Wednesday’s economic calendar might bring somewhat positive news to the European Central Bank, with figures on Eurozone’s inflation and unemployment rate bringing policy normalization closer in sight.

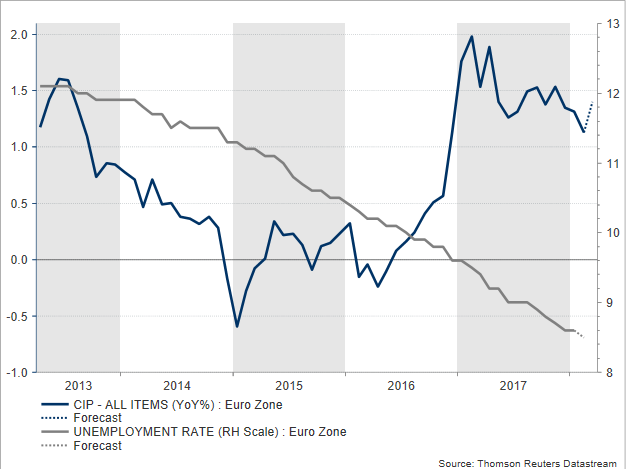

Preliminary consumer prices for the month of March will attract the most attention on Wednesday at 0900 GMT as these will show whether price pressures have strengthened enough to lift inflation one step towards the ECB’s target of 2.0%. The headline CPI is expected to support this narrative up to an extent, with analysts forecasting that the measure has rebounded from 1.1% to 1.4% on yearly terms after easing for two consecutive months. The core CPI which excludes food and energy is anticipated to rise as well but at a slower pace, inching up by 0.1 percentage points to 1.3% y/y.

Separately, the unemployment rate published at the same time will probably bring some smiles too if the measure retreats further to a fresh nine-year low of 8.5% in February as forecasts suggest. While the gauge has not reached pre-crisis levels yet as is the case in the US, hinting that the there is still some slack in the labor market, its downward pattern over the past five years signals that the available labor capacity becomes narrower, a critical factor needed to push wages and therefore inflation up faster.

Regarding interest rates, it is clear that policymakers are not willing to deliver any hike until “well past the horizon of net asset purchases” according to Draghi who wants to see first a sustained adjustment in the inflation path. Yet, Jens Weidmann, the Bundesbank’s president and Germany’s likely candidate to replace Mario Draghi as ECB chair when his term expires in late 2019, lent credence to market expectations for an interest rate increase towards mid-2019. However, not all ECB policymakers share the same view. For example, ECB Governing Council member Erkki Liikanen last week cautioned against premature tightening, given that inflation still remains well below the Bank’s target of below but close to 2% on annualized basis.

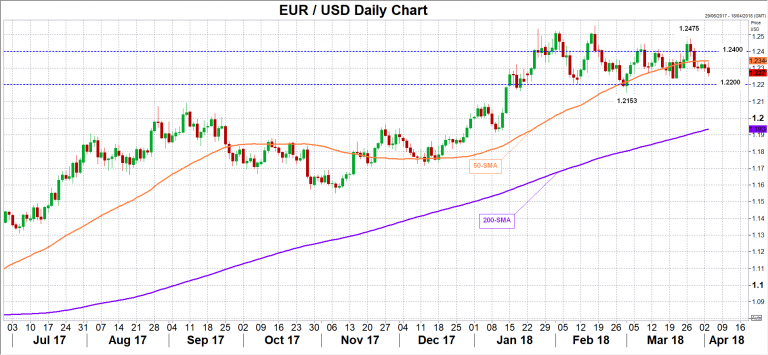

Turning to forex markets, euro/dollar has been on the back foot the past few days, slipping to a two-week low of 1.2260 today and any sign pointing to stronger inflationary pressures would be definitely valuable to the pair. Therefore, if CPI and unemployment numbers impress, the pair could run towards the 50-day simple moving average which currently stands at 1.2343. In case of stronger readings, prices could break the 1.2400 handle, with scope to reach the 1 ½ -month high of 1.2475 tracked on March 27.

Alternatively, disappointing readings – especially on the CPI front – could add further losses to the market, driving euro/dollar down to the 1.2200 key-level which offered some support from the mid of January onwards. A substantial close below 1.2153, however, could trigger further downfalls.

On Thursday, Eurozone’s retail sales and producer prices for the month of February could bring fresh volatility to the market. The former is said to have eased to 2.1% y/y, while the latter is expected to remain steady at 1.5% y/y.

{kind=link}