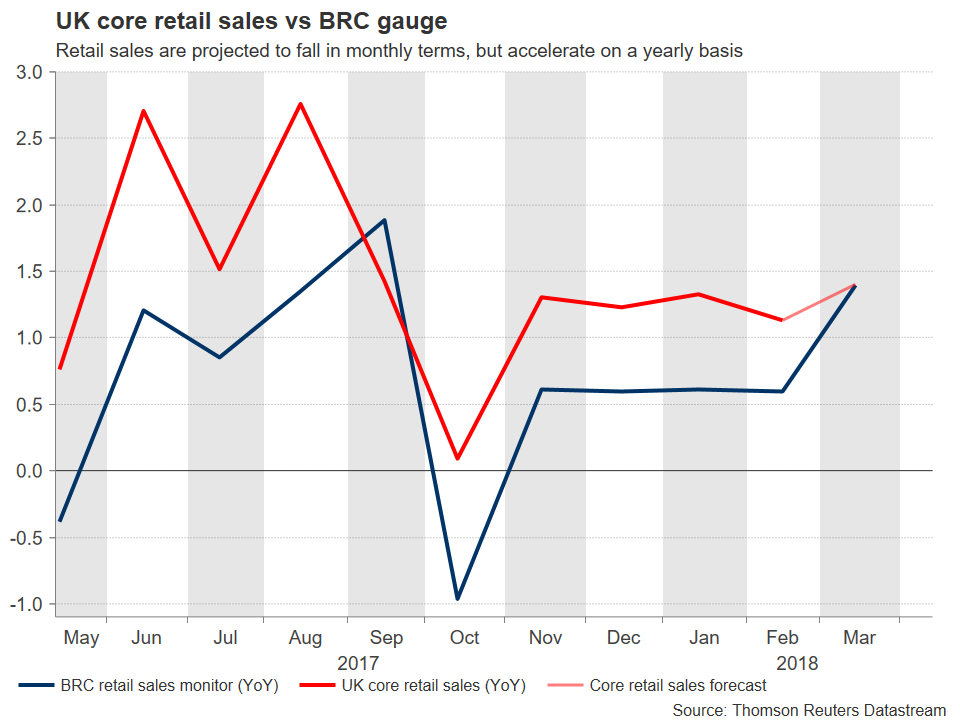

It’s going to be a busy week for sterling traders. The UK will release its employment figures for February on Tuesday at 0830 GMT, while inflation and retail sales data for March will follow at the same time on Wednesday and Thursday respectively. Wages are projected to have picked up speed, while inflation is anticipated to have risen at the same pace as previously, pushing real wage growth back into positive territory. Such prints would likely be encouraging news for the Bank of England (BoE), and could cement expectations for a rate hike in May.

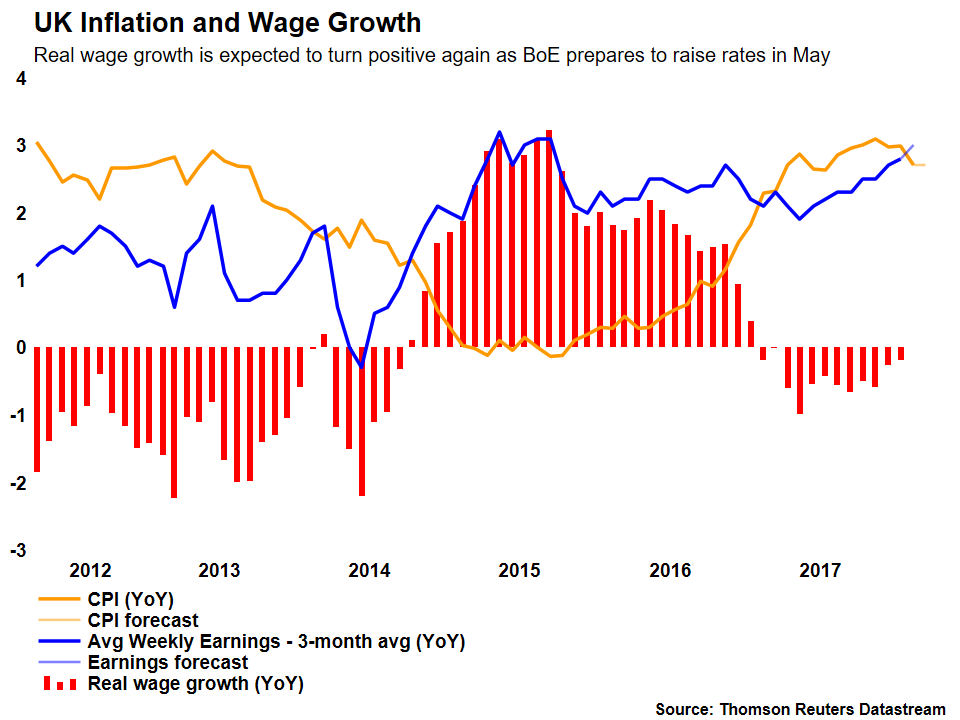

Following the Brexit vote, UK inflation accelerated sharply but wage growth remained largely flat, leading to a ‘squeeze’ in the real incomes of consumers. With inflation running ahead of wages, people essentially become poorer on average, as living expenses increase faster than their incomes. This has been one of the main factors that have deterred the BoE from raising interest rates too much. The Bank considers the surge in inflation to be a transitory effect that will fade over time, caused by the depreciation of sterling back in 2016. As such, it is reluctant to raise rates in order to fight high inflation, as higher rates could weigh further on consumers’ disposable incomes, thereby hurting consumption and slowing the economy.

This week, investors will get an update on whether the ‘income squeeze’ continues to haunt UK consumers, or whether the situation is turning around. According to forecasts, wages are expected to outpace inflation, pushing real income growth back into positive territory. Specifically, the unemployment rate is projected to have remained unchanged in February, while average weekly earnings both including and excluding bonuses are expected to have accelerated, reaching 3.0% and 2.8% respectively in yearly terms. Meanwhile, CPI inflation is anticipated to have remained unchanged at 2.7% year-on-year in March, while the core print that excludes the effects of volatile items is forecast to have ticked up to 2.5%, from 2.4% in February.

Gauges of the labor market and inflationary pressures support these forecasts. With regards to wages, the Markit UK Report on Jobs for February showed that starting salaries continued to rise sharply, holding close to a 31-month high amid shortages for candidates. As for inflation, the Markit services PMI for March noted that prices charged by service firms continued to increase at a robust pace, with Markit’s Chief Business Economist Chris Williamson concluding that “consumer price inflation could remain stubbornly high in coming months”.

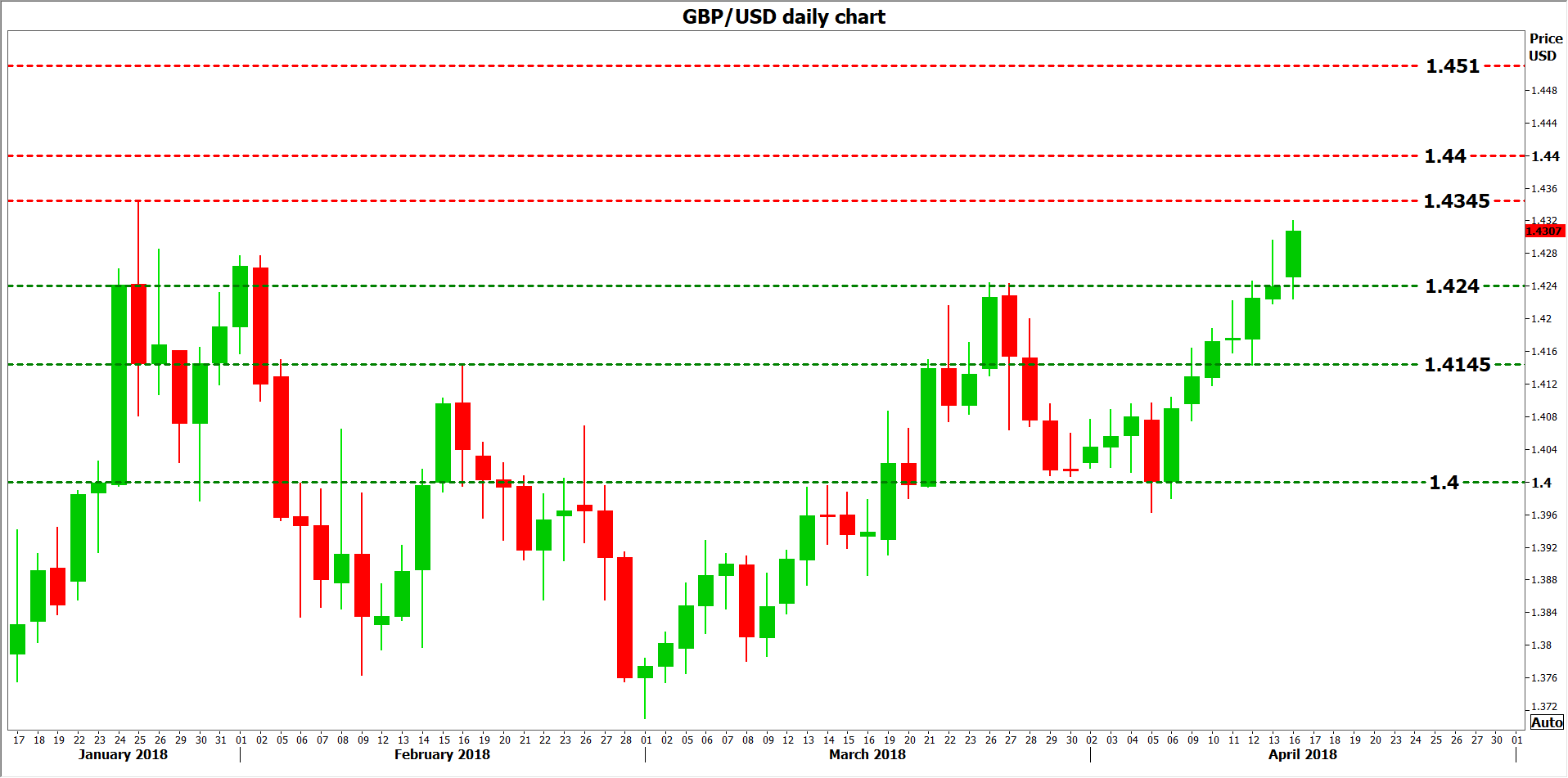

On the flip side, if real wage growth remains negative – for example with wages failing to accelerate or inflation surprising to the upside – then sterling could come under pressure as markets begin to doubt whether a May hike will indeed materialize and traders take some profit on their prior long-pound bets. Immediate support in pound/dollar could come around 1.4240, the peaks of March 27, with a downside violation of that barrier bringing into view the 1.4145 area, which was congested in the recent past and also encapsulates a peak from February. If sellers manage to overcome that zone, then buy orders may be found near the psychological handle of 1.4000.

{kind=link}