After further increases in stock markets yesterday, the market is pausing and consolidating ahead of European trading. Asian equity markets are in the green, trading up around 1% but Chinese markets are lagging due to trade tensions with the US. Dovish comments from BOE Governor Carney and soft US CPI data yesterday led to a risk-on mood in markets. Lower inflation is a key driver at the moment, with markets fearing any move higher in rates. USDJPY has slipped lower from its second test of the 110.000 level, as US 10-Year yields hang just under the 3% mark, at 2.97%. Spot US Oil is off its high from yesterday of $71.80, trading around $71.26.

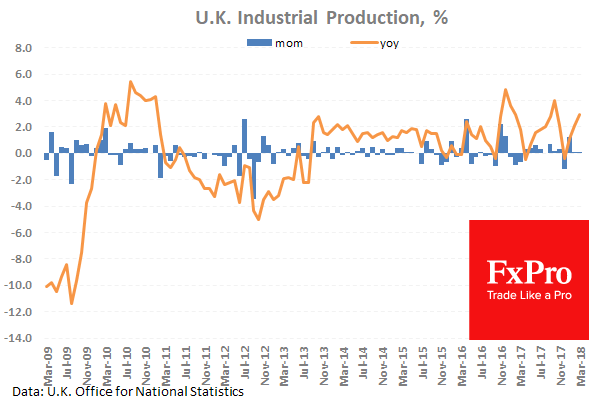

UK Industrial Production (YoY) (Mar) was 2.9% versus an expected 3.1%, against a previous 2.2%, which was revised down to 2.1%. Industrial Production (MoM) (Mar) was 0.1% versus an expected 0.2%, against 0.1% previously. This reading came in higher than last month but again failed to meet expectations. Manufacturing Production (YoY) (Mar) was 2.9% versus an expected 2.9%, against 2.5% previously. Manufacturing Production (MoM) (Mar) was -0.1% versus an expected -0.2%, against -0.2% previously. GBPUSD moved higher from 1.35268 to 1.36170 after this data release.

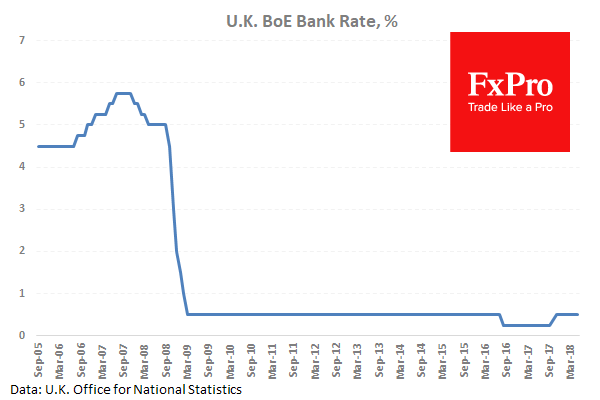

The Bank of England’s Interest Rate Decision resulted in rates remaining unchanged at 0.5%. The BOE Minutes, BOE Quarterly Inflation Report and the Monetary Policy Statement were also released at the same time. The BOE Asset Purchase Facility remained unchanged at £435B. BOE Governor Mark Carney led the Press Conference where he continually repeated that he was confident in the economy but any hikes would be “limited and gradual”. The BOE is in “wait and see mode”, with a focus on Q2 data. GBPUSD fell from 1.35951 to a low of 1.34900 during this event.

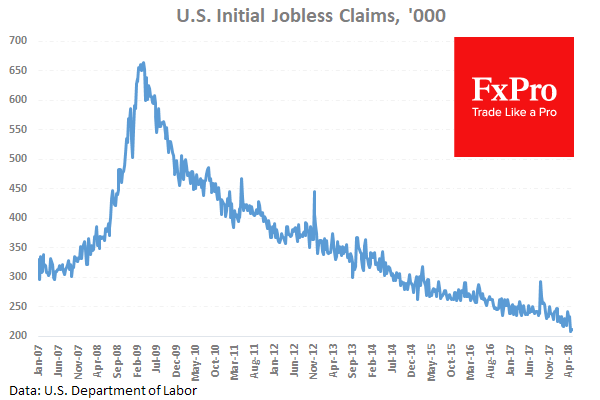

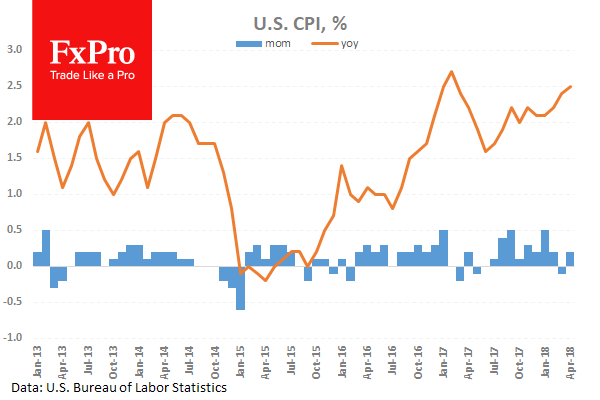

US Continuing Jobless Claims (Apr 27) were 1.790M versus an expected 1.778M, against 1.756M previously, which was revised up to 1.760M. Initial Jobless Claims (May 4) was 211K versus an expected 218K, against 211K previously. This data is showing a continuing increase in the number of people who are jobless. US Consumer Price Index (YoY) (Apr) data was released, coming in as expected at 2.5% against 2.4% previously. Consumer Price Index Ex-Food & Energy (YoY) (Apr) data was released, missing the expected reading of 2.2% and matching the previous 2.1% reading. Consumer Price Index Ex-Food & Energy (MoM) (Apr) came in at 0.1% versus an expected reading of 0.2%, against 0.2% previously. Consumer Price Index (MoM) (Apr) data was released coming in at 0.2% versus an expected reading of 0.3%, against -0.1% previously. Consumer Price Index Core s.a. (Apr) data came in at 256.450 versus an expected reading of 256.899, against 256.200 previously. These data points will provide an updated measure of the effect of inflation on consumers. Inflation is one of the main drivers of market sentiment in the US currently. The expectation was for an increase in consumer prices, with most data matching or falling marginally short of those expectations. USDJPY fell from 109.593 to 109.316 after this data release.

EURUSD is down -0.04% overnight, trading around 1.19104.

USDJPY is up 0.10% in early session trading at around 109.495.

GBPUSD is unchanged this morning, trading around 1.35167.

USDCAD is unchanged overnight, currently trading around 1.27668.

Gold is down -0.17% in early morning trading at around $1,318.91.

WTI is down -0.22% this morning, trading around $71.26.

{kind=link}