Dollar trades broadly lower as results of US mid-term election kick in. At the time of writing, Democrats already claimed victory of 163 seats in the House while Republicans got 159 seats. And the Democrats have already achieved a net gain of more than 23 seats up to regain majority of House. Republicans will keep control of the Senate as widely expected. The question now is how much a majority would the Democrats get. And it seems the larger the majority, the more bearish the greenback is.

Staying in the currency markets, New Zealand Dollar is the strongest one for today as boosted by stellar employment data. Euro and Australian Dollar are the second and third strongest. It seems like disregarding the impact of data, Euro and Aussie are the biggest beneficiary of US elections. Canadian Dollar is the second weakest as also dragged down by free fall in oil prices. Yen follows as the third weakest.

In other markets, DOW closed 0.68% higher at 25635.01 overnight. S&P 500 rose 0.63% while NASDAQ added 0.64%. Treasury yields were mixed with 10 year yield up 0.013 to 3.214. 30 year yield was down -0.006 at 3.426. Asian markets are cheering US results with Nikkei trading up 0.45%, Hong Kong HSI up 1.17%, China Shanghai SSE up 0.26%, Singapore Strait Times up 0.53%.

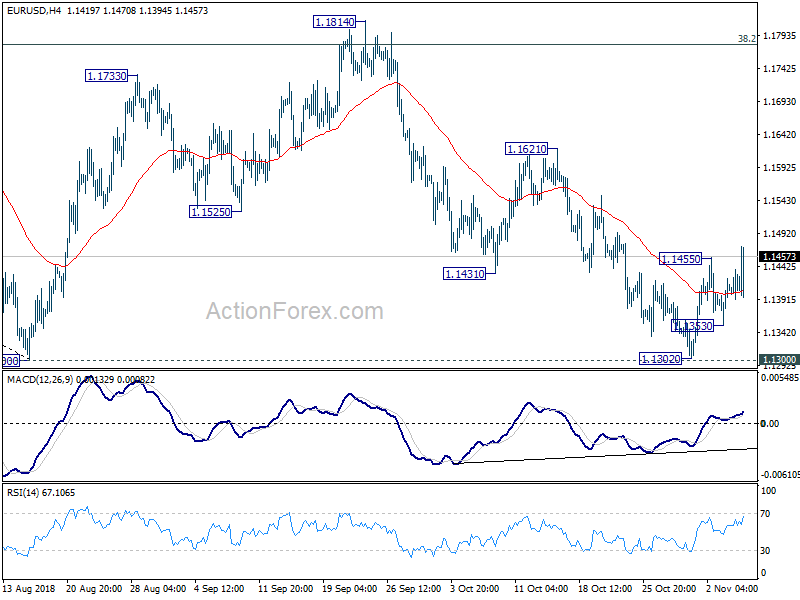

Technically, EUR/USD’s rebound from 1.1302 resumes by breaking 1.1455 temporary top and should be heading towards 1.1621 resistance. That hints that USD/CHF will likely dip through 0.9968 too as correction from 1.0094 extends. GBP/USD’s rebound is on track for 1.3297 resistance despite more Brexit jokes. EUR/GBP also finally broke 0.8722 support, despite weak momentum, and should be heading to next support at 0.8620.

NZD surges after surprisingly strong New Zealand job data

New Zealand Dollar surges broadly after surprisingly strong employment data. Unemployment rate dropped -0.5% to 3.9% in Q3 versus expectation of 4.4%. That’s the lowest level in a decade since June 2008. Employment rate rose 0.5% to 68.3%, highest since the series began 30 years ago. Participation rate also rose 0.2% during the quarter to 71.1%. Employment grew 1.1% qoq versus expectation of 0.5% qoq.

The set of strong data came in just a day ahead of RBNZ rate decision. RBNZ is widely expected to keep OCR unchanged at 1.75%, without a doubt. The tone of the accompanying statement is the key. RBNZ Governor Adrian Orr has sounded rather dovish in his recent comments, even being open for a cut as next move. The upbeat data will likely be reflected in the communications and thus, at least, remove some bets on RBNZ cut.

UK PM May denied childish document on plan to announce Brexit deal on Nov 19

BBC reported, based on a “leaked” document titled “Brexit Communications Grid Summary” that UK Brexit Minister Dominic Raab is set to announce the full withdrawal agreement on November 19 and put to parliament. And, according to the document, the Parliament would vote on the bill on November 27.

But Prime Minister Theresa May’s spokesman quickly came out and denied it. The spokesman said “The misspelling and childish language in this document should be enough to make clear it doesn’t represent the government’s thinking. You would expect the government to have plans for all situations – to be clear, this isn’t one of them.”

EU Barnier said no operational Irish backstop, no brexit accord

EU chief Brexit negotiator Michel Barnier reiterated yesterday that “we are still not at the 100 percent” on the Brexit agreement. And, “What is missing is a solution for the issue of Ireland.” He added that “Without an operational backstop there will not be an accord and there will not be a transition period. That is certain.” Besides Barnier also echoed Ireland’s stance that the backstop “cannot have an end-date” and “it must be applicable unless and until another solution is found.”

Elsewhere

Japan labor cash earnings rose 1.% yoy in September, below expectation of 1.2% yoy. German will release industrial production in European session. Eurozone will release retail sales. Swiss will release foreign currency reserves. Later in the day, Canada will release Ivey PMI.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1398; (P) 1.1419; (R1) 1.1446; More….

EUR/USD’s break of 1.1455 suggests that rebound from 1.1302 has resumed. Intraday bias is turned to the upside for 1.1621 resistance. Rise from 1.1302 is seen as the third leg of the consolidation pattern form 1.1300. Hence, upside is expected to be limited by 1.1814 to bring down trend resumption eventually. On the downside, break of 1.1353 minor support will suggests that rise from 1.1302 has completed. In that case, retest of 1.1300 key support should be seen next.

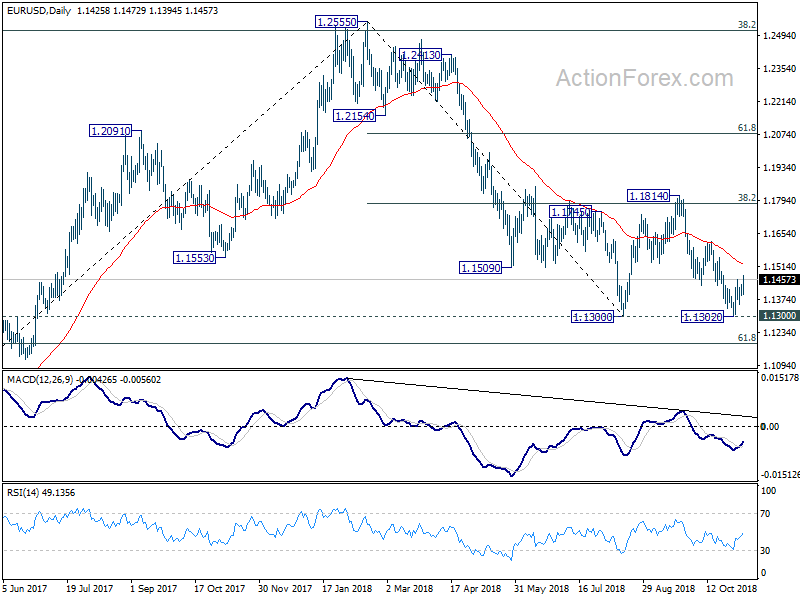

In the bigger picture, price actions from 1.1300 is seen as a corrective pattern. Decisive break of 1.1300 will resume the down trend from 1.2555 to 61.8% retracement of 1.0339 (2017 low) to 1.2555 at 1.1186 next. Sustained break there will pave the way to retest 1.0339. In case the consolidation from 1.1300 extends, upside should be limited by 1.1814 and 38.2% retracement of 1.2555 to 1.1300 at 1.1779. to bring down trend resumption eventually.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Overall Household Spending Y/Y Sep | -1.60% | 1.60% | 2.80% | |

| 00:01 | GBP | BRC Retail Sales Monitor Y/Y Oct | 0.10% | 0.60% | -0.20% | |

| 03:30 | AUD | RBA Rate Decision | 1.50% | 1.50% | 1.50% | |

| 07:00 | EUR | German Factory Orders M/M Sep | 0.30% | -0.40% | 2.00% | 2.50% |

| 08:45 | EUR | Italy Services PMI Oct | 49.2 | 52.1 | 53.3 | |

| 08:50 | EUR | France Services PMI Oct F | 55.3 | 55.6 | 55.6 | |

| 08:55 | EUR | Germany Services PMI Oct F | 54.7 | 53.6 | 53.6 | |

| 09:00 | EUR | Eurozone Services PMI Oct F | 53.7 | 53.3 | 53.3 | |

| 10:00 | EUR | Eurozone PPI M/M Sep | 0.50% | 0.30% | 0.30% | 0.40% |

| 10:00 | EUR | Eurozone PPI Y/Y Sep | 4.50% | 4.20% | 4.20% | 4.30% |

| 13:30 | CAD | Building Permits M/M Sep | 0.40% | 0.30% | 0.40% |

Interventions?")

{kind=link}