Australian and New Zealand Dollar are slightly firmer in Asian session today despite Chinese GDP miss. The stronger than expected industrial production growth ease some concerns over worse slowdown in Q4. Meanwhile, Sterling continues to consolidation in tight range, digesting this week’s strong gains. The Pound’s fate will heavily depend on the crucial Brexit vote on Saturday.

As for the week, Sterling remains the strongest one, shot up by UK Prime Minister Boris Johnson’s new Brexit deal with EU. The development took other European majors higher too, with Swiss Franc second strongest and Euro third. On the other hand, Yen is currently the weakest for the week, followed by Dollar, as risk aversions eased.

In Asia, Nikkei closed up 0.18%. Hong Kong HSI is down -0.58%. China Shanghai SSE is down -1.14%. Singapore Strait Times is down -0.45%. Japan 10-year JGB yield is up 0.0089 at -0.145. Overnight, DOW rose 0.09%. S&P 500 rose 0.28%. NASDAQ rose 0.40%. 10-year yield rose 0.009 to 1.757.

China GDP growth slowed to 6% in Q3, worst since 1992

China’s GDP growth slowed further to 6.0% yoy in Q3, down from 6.2% yoy in Q2 and missed expectation of 6.1% yoy. That’s also the worst pace since Q1 of 1992, the earliest quarterly data on record. National Bureau of Statistics spokesman Mao Shengyong said China was ” faced with mounting risks and challenges both at home and abroad”. But he attempted to tone down the situation and said ” the national economy maintained overall stability … and improved living standard.” He also added there was ample room for adjustments on monetary policy,

The weak data raised concern that the slowdown this year could be worse than originally expected, as trade war with US weigh. While there appears to be some progresses on trade negotiations, the imposed tariffs are remaining. Uncertainties continued to weigh on business sentiments too. Growth could slow further below 6% handle in Q4.

Nevertheless, on the positive side, industrial production grew 5.8% yoy in September, comfortably beat expectations of 5.0% yoy. That’s also a notably improvement from 4.4% yoy in August. Retail sales growth accelerated to 7.8% yoy, up from 7.5% yoy and matched expectations. Fixed asset investment, however, slowed to 5.4% ytd yoy, down from 5.5% and matched expectations.

Japan CPI core slowed to 0.3%, lowest since Apr 2017

Japan CPI core (all items ex-fresh food), slowed to 0.3% yoy in September, down from 0.5% yoy, matched expectation of 0.3% yoy. That’s also the lowest level in more than two years since April 2017, and drifted further away from BoJ’s 2% target. All items CPI slowed to 0.2% yoy, down from 0.3% yoy and matched expectations. CPI core-core (all items ex-fresh food and energy) slowed to 0.5% yoy, down form 0.6% yoy, matched expectation but remained sluggish.

Japan Finance minister Taro Aso said yesterday that the government was ready to ramp up stimulus to guard against risks from slowing global growth and US-China trade tensions. He said after a meeting of G20 finance leaders, “Given uncertainty over the global economy, exports are falling and weighing on manufacturers’ output. But the weakness has yet to spread to non-manufacturers or domestic demand.

Ado added, “if we need to compile some form of an economic stimulus package, we are ready to take various types of fiscal measures flexibly”. He also emphasized that “When you look back at the problems Japan faced, including deflation, they can’t be fixed by monetary policy alone. You need a coordinated monetary and fiscal response.”

Separately, the good news is that the government estimated the US-Japan trade deal will boost Japan’s economy by 0.8%. There will be around JPY 4T contribution to GDP based on its fiscal 2018 figures. Also, the deal will create around 280k jobs.

Fed Williams: Economy in pretty good place with very resilient consumers

New York Fed President John Williams said yesterday that the economy is in a “pretty good place” and consumption has been “very resilient”. While consumer spending is a lagging indicator, data on asset prices, employment growth and wage growth support positive outlook.

Fed policymakers factored in some uncertainties during the decisions for rate cuts back in July and September. The factors include global slowdown, low inflation and trade tensions. However, Williams added, “I don’t want to have this narrative that we still have the same conditions out there so does it mean we need to take further and further action.” And, “what we need to do is weigh or consider how those factors are influencing the outlook.”

Looking ahead

Eurozone current account will be the only feature in a rather light day. Fed Vice Chair Richard Clarida will speak today, so will BoE Governor Mark Carney.

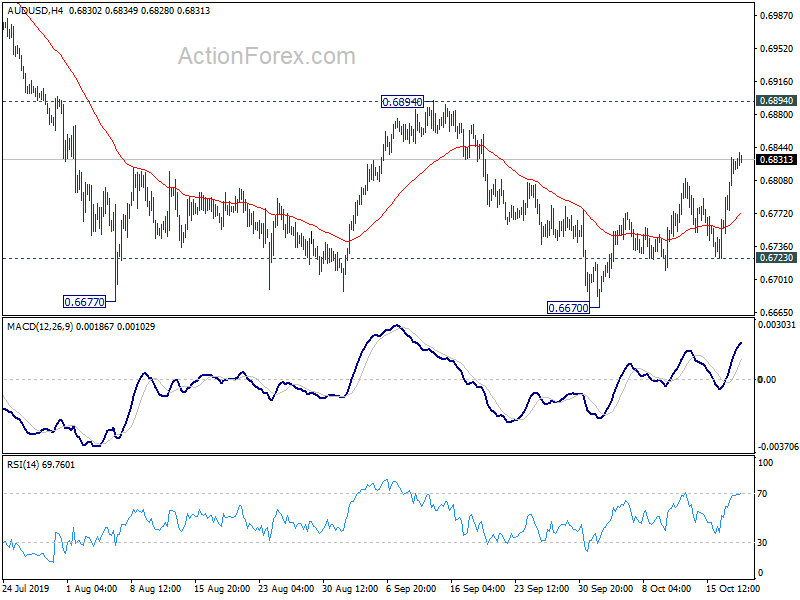

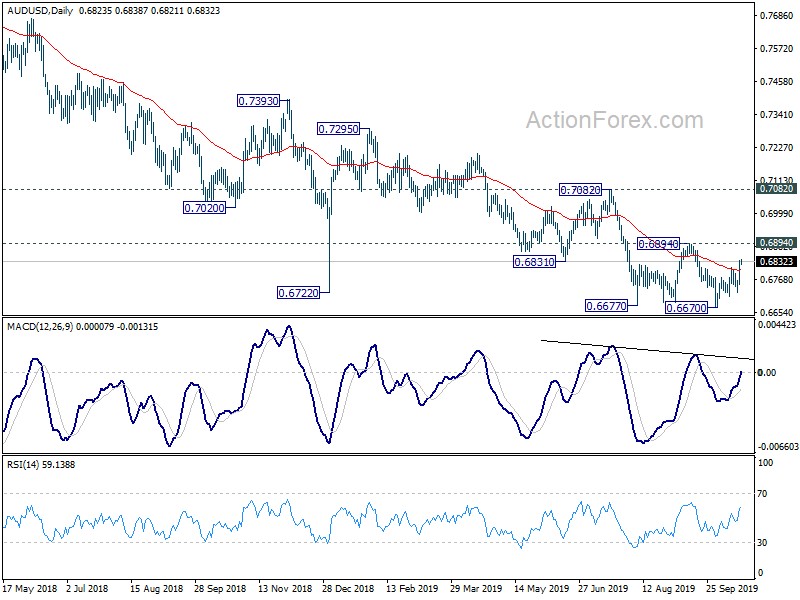

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.6775; (P) 0.6804; (R1) 0.6855; More…

Intraday bias in AUD/USD remains mildly on the upside as rebound from 0.6677 is extending. But outlook is unchanged that such rebound is seen as a corrective move. Hence, upside should be limited by 0.6894 resistance to bring down trend resumption. On the downside, break of 0.6723 minor support will turn bias back to the downside for retesting 0.6670 low.

In the bigger picture, decline from 0.8135 (2018 high) is seen as resuming the long term down trend from 1.1079 (2011 high). Next target is 0.6008 (2008 low). On the upside, break of 0.7082 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will remain bearish even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y Sep | 0.30% | 0.30% | 0.50% | |

| 2:00 | CNY | GDP Y/Y Q3 | 6.00% | 6.10% | 6.20% | |

| 2:00 | CNY | Retail Sales Y/Y Sep | 7.80% | 7.80% | 7.50% | |

| 2:00 | CNY | Industrial Production Y/Y Sep | 5.80% | 5.00% | 4.40% | |

| 2:00 | CNY | Fixed Asset Investment YTD Y/Y Sep | 5.40% | 5.40% | 5.50% | |

| 8:00 | EUR | Current Account (EUR) Aug | 21.3B | 20.5B |

{kind=link}