Sentiment is mixed overall as Russia invasion of Ukraine is continuing. Asia is split into two world, with Nikkei and Singapore markets steady. But Hong Kong and China stock markets are in steep selloff again, after US warned China of helping Russia of easing the impact of sanction. The upbeat Chinese data are generally ignored. Oil price and Gold are both extending near term pull back.

In the currency markets, Yen’s decline continue, as driven by extended rally in global benchmark yields. But selloff in Aussie and Kiwi is even more severe, as dragged down by China. Euro is recovering together with Sterling. Dollar is mixed for now, awaiting the guidance from FOMC later in the week.

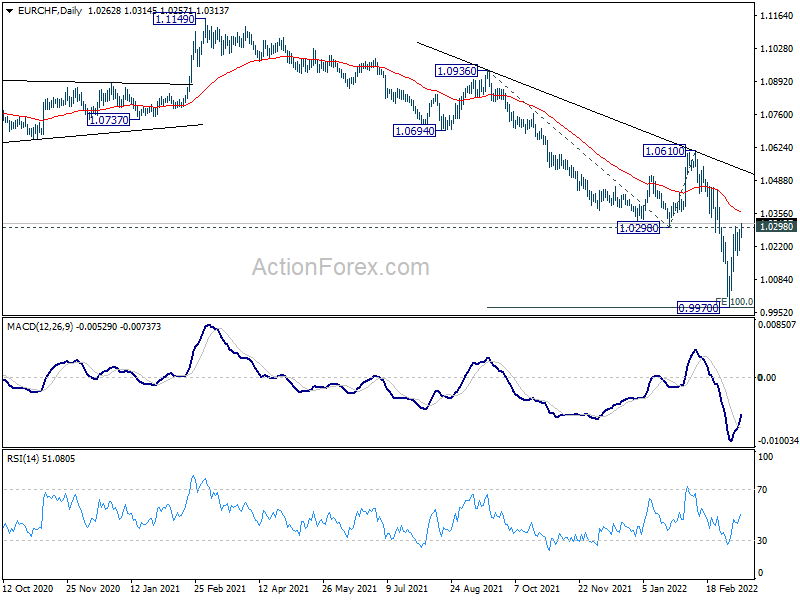

Technically, EUR/CHF is extending the rebound from 0.9970. The break of 1.0298 support turned resistance now suggest that a medium term bottom is probably in place after defending parity. That’s an important sign of stabilization in Euro. Attention will be in particularly to 1.1120 resistance in EUR/USD. Break will further confirm the war triggered selloff is fully over.

In Asia, at the time of writing, Nikkei is up 0.32%. Hong Kong HSI is down -2.99%. China Shanghai SSE is down -2.18%. Singapore Strait Times is up 0.64%. Japan 10-year JGB yield is up 0.0145 at 0.210. Overnight DOW rose 0.00%. S&P 500 dropped -0.74%. NASDAQ dropped -2.04%. 10-year yield rose strongly by 0.136 to 2.140.

China industrial production and retail sales growth unexpectedly strong

For the two months of January and February, China industrial production grew 7.5% yoy, well above expectation of 3.9% yoy. That’s the fastest pace since June 2021. Retail sales rose 6.7% yoy, also well above expectation of 3.0% yoy, also the fastest since June 2021. Fixed asset investment rose 12.2% yoy, above expectation of 5.0% yoy, highest since July 2021.

Separately, PBoC unexpectedly kept the rate of CNY 200B worth of one-year medium term lending facility (MLF) loans to some financial institutions unchanged at 2.85%. The operation resulted in a net injection of CNY 100B funds to the market. The central bank said it is for “maintaining banking system liquidity reasonably ample”.

RBA minutes reiterate patient stance on interest rate

In the minutes of March 1 meeting, RBA reiterated that it will not hike cash rate “until actual inflation is sustainably within the 2 to 3 per cent target band. Now, it was “too early to conclude that” inflation is “sustainably within the target band”.

There were “uncertainties about how persistent the pick-up in inflation”. Wage growth “remained modest”, and “it was likely to be some time before aggregate wages growth would be at a rate consistent with inflation being sustainably at target.”

Thus, RBA is “prepared to be patient” on lifting interest rate.

New Zealand BNZ services index rose to 48.6, pain is accumulating

New Zealand BNZ Performance of Services Index rose slightly from 46.0 to 48.6 in February. Activity/sales rose from 44.6 to 50.7. Employment dropped from 47.0 to 45.0. New orders/business rose from 41.2 to 53.6. Stocks/inventories rose from 48.0 to 50.0. Supplier deliveries dropped from 43.4 to 34.4.

BNZ Senior Economist Doug Steel said that “February marks the PSI’s seventh consecutive month below the breakeven 50 mark. Pain is accumulating. While there were some overs and unders in the components, all remain below their respective long-term averages.”

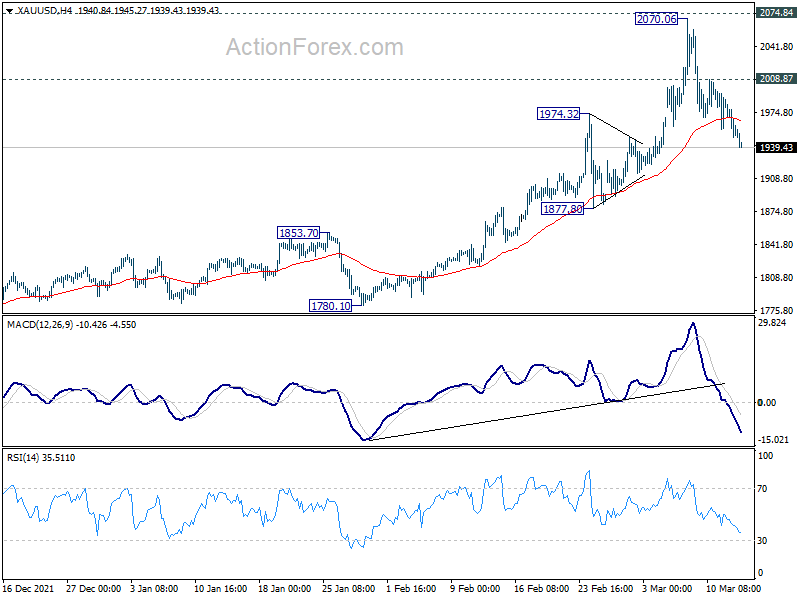

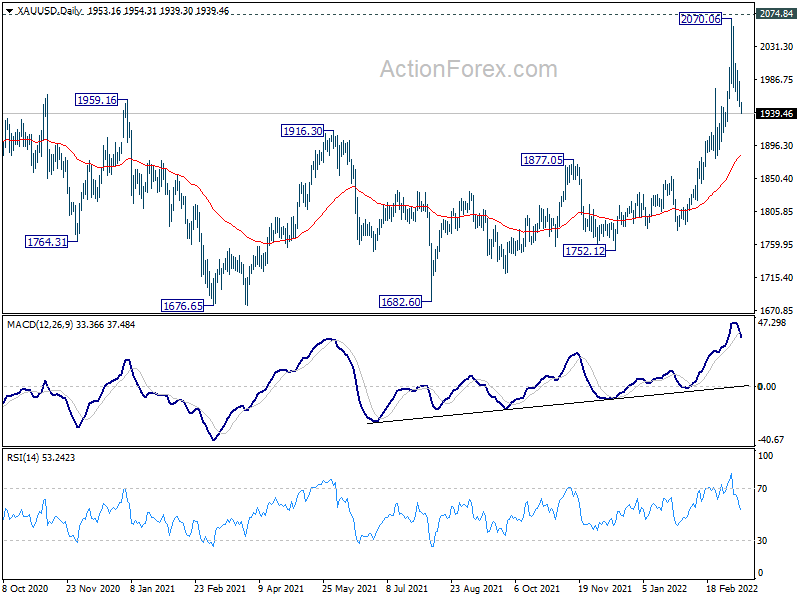

Gold extends pull back, heading back to 55 day EMA

Gold’s pull back from 2070.06 picks up momentum today. The break of 1960.83 minor support should confirm short term topping, after initial rejection by 2074.84 high. Deeper decline is now expected as long as 2008.87 minor resistance holds, towards 55 day EMA (now at 1882.52).

The pull back from 2070.06 could either be a correction to rise from 1682.60 only. Or it could be the third led of the corrective pattern from 2074.84 high. Strong rebound from 55 day EMA will favor the former case, and bring upside breakout through 2074.84 sooner. However, sustained break of 55 day EMA will favor the latter case, and bring deeper fall back to 1676.65 support.

Looking ahead

UK employment, Swiss PPI, Eurozone industrial production and Germany ZEW economic sentiment will be released in European session. Later in the day, Canada will release housing starts and manufacturing sales. US will release Empire state manufacturing index and PPI.

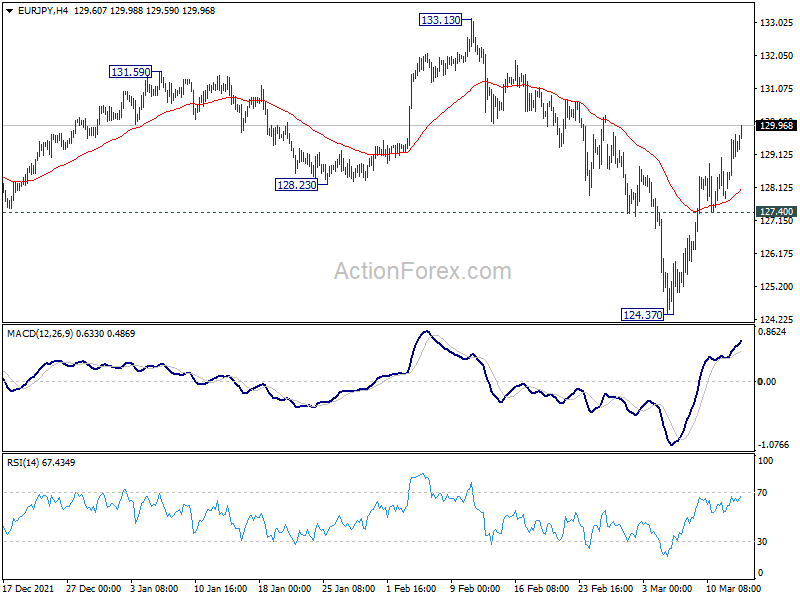

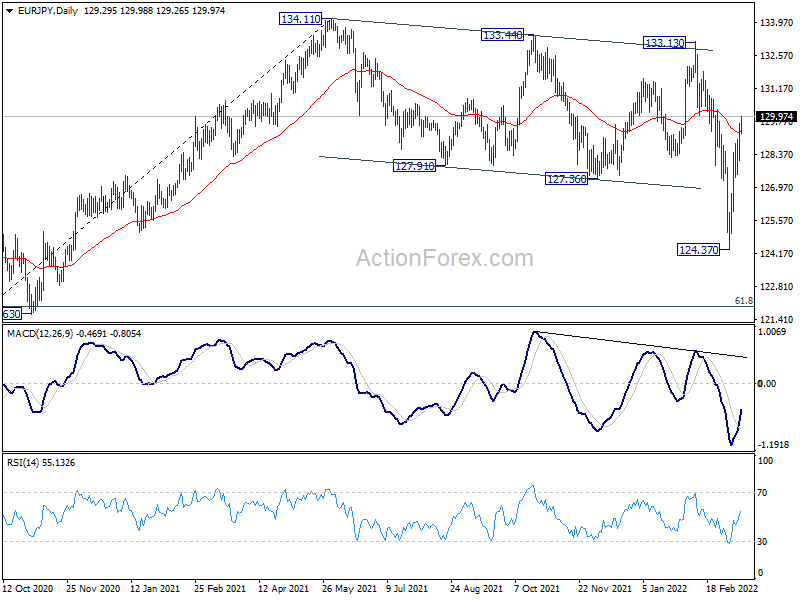

EUR/JPY Daily Outlook

Daily Pivots: (S1) 128.33; (P) 129.02; (R1) 130.00; More….

Intraday bias in EUR/JPY remains mildly on the upside at this point. With break of 55 day EMA, the corrective pattern from 134.11 might have completed at 124.37 already. Further rise should be seen to 133.13/134.11 resistance zone. This will now be the mildly favored case as long as 127.40 minor support holds. Nevertheless, break of 127.40 will bring retest of 124.37 instead.

In the bigger picture, medium term outlook remains neutral for now. Price actions from 134.11 are so far still seen as a corrective pattern. That is, rise from 114.42 (2020 low) is in favor to resume at a later stage. But before that, the corrective pattern from 134.11 could still extend further, sideway or downward. In the latter case, break of of 124.37 will target 61.8% retracement of 114.42 to 134.11 at 121.94.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | RBA Meeting Minutes | ||||

| 00:30 | AUD | House Price Index Q/Q Q4 | 4.70% | 3.90% | 5.00% | |

| 02:00 | CNY | Retail Sales Y/Y Feb | 6.70% | 3.00% | 1.70% | |

| 02:00 | CNY | Fixed Asset Investment (YTD) Y/Y Feb | 12.20% | 5.00% | 4.90% | |

| 02:00 | CNY | Industrial Production Y/Y Feb | 7.50% | 3.90% | 4.30% | |

| 07:00 | GBP | Claimant Count Change Feb | -31.9K | |||

| 07:00 | GBP | ILO Unemployment Rate (3M) Jan | 4.00% | 4.10% | ||

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Jan | 4.60% | 4.30% | ||

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Jan | 3.70% | 3.70% | ||

| 07:30 | CHF | Producer and Import Prices M/M Feb | 0.40% | 0.60% | ||

| 07:30 | CHF | Producer and Import Prices Y/Y Feb | 5.10% | 5.40% | ||

| 10:00 | EUR | Eurozone Industrial Production M/M Jan | 0.40% | 1.20% | ||

| 10:00 | EUR | Germany ZEW Economic Sentiment Mar | 10.3 | 54.3 | ||

| 10:00 | EUR | Germany ZEW Current Situation Mar | -22.5 | -8.1 | ||

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Mar | 49.3 | 48.6 | ||

| 12:15 | CAD | Housing Starts Y/Y Feb | 235K | 231K | ||

| 12:30 | CAD | Manufacturing Sales M/M Jan | 0.30% | 0.70% | ||

| 12:30 | USD | Empire State Manufacturing Index Mar | 7.3 | 3.1 | ||

| 12:30 | USD | PPI M/M Feb | 1.00% | 1.00% | ||

| 12:30 | USD | PPI Y/Y Feb | 10.00% | 9.70% | ||

| 12:30 | USD | PPI Core M/M Feb | 0.60% | 0.80% | ||

| 12:30 | USD | PPI Core Y/Y Feb | 8.10% | 8.30% |

{kind=link}