Swiss Franc climbed against major currencies following the release of stronger-than-expected inflation data, which is expected to bolster the case for SNB to raise interest rates by 50bps during their upcoming meeting this month. Euro also gained ground, supported by hawkish comments from ECB officials, while Dollar trailed behind.

Conversely, Australian Dollar is trading as the worst performer,weighed down by China’s 5% growth target for the year, which is the lowest rate in decades. Despite expectations of a 25bps interest rate hike by the RBA in the upcoming Asian session, Aussie is facing pressure from the cautious outlook on China’s economy. Meanwhile, the New Zealand Dollar and Sterling are also trading lower.

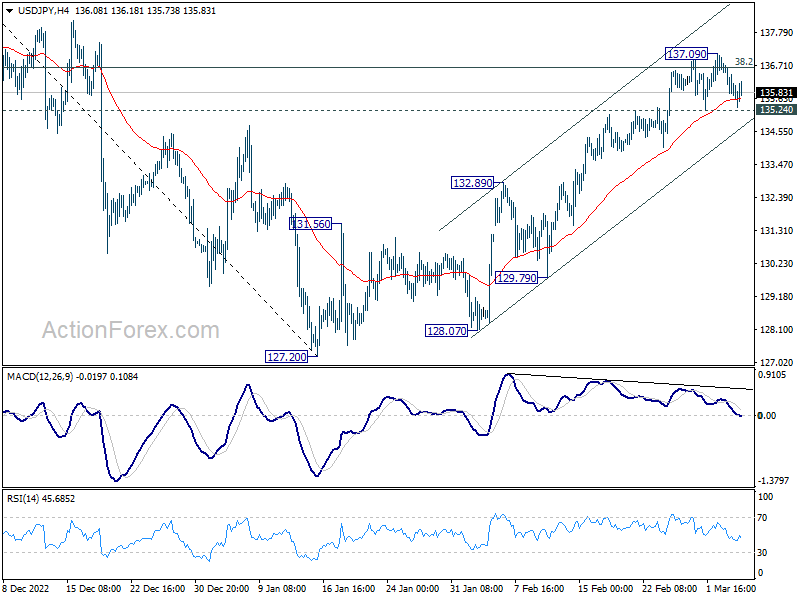

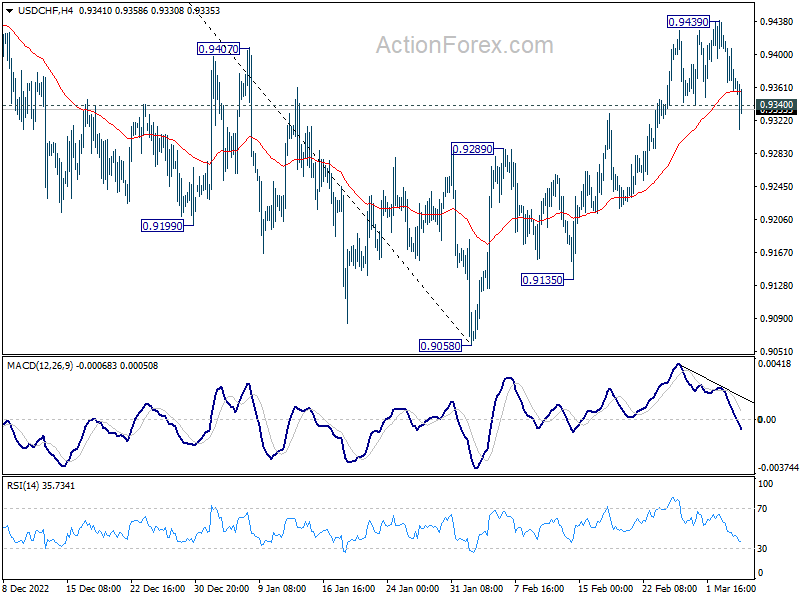

Technically, USD/CHF has broken 0.9340 support to confirm short term topping at 0.9439. Focus will turn to 135.24 support in USD/JPY. Break of the level should indicate short term topping at 137.09. If that happens, the chance for a near term reversal in Dollar will growth. Further break of 1.0690 resistance in EUR/USD could trigger deeper selloff in the greenback.

In Europe, at the time of writing, FTSE is down -0.54%. DAX is up 0.44%. CAC is up 0.33%. Germany 10-year yield is down -0.0649 at 2.655. Earlier in Asia, Japan 10-year JGB yield dropped -0.0020 to 0.504. Nikkei rose 1.11%. Hong Kong HSI rose 0.17%. China Shanghai SSE dropped -0.19%. Singapore Strait Times rose 0.23%.

ECB Lane: Appropriate to raise interest rates further beyond March

ECB Chief Economist Philip Lane indicated that it’s “appropriate” to raise interest rates further beyond March meeting. But the “exact calibration” will depend on the upcoming macroeconomic projections and incoming data on inflation and the monetary transmission mechanism.

Lane said in a speech, “the current information on underlying inflation pressures suggests that it will be appropriate to raise rates further beyond our March meeting”.

“By bringing the key policy rates to a sufficiently restrictive level and fostering a period of below-trend growth through the dampening of demand, we will counter-act above-target medium-term inflation pressures and also ensure that the prolonged phase of above-target inflation does not become embedded through a de-anchoring of inflation expectations,” he explained.

ECB Holzmann calls for four more 50bps hikes

ECB Governing council member Robert Holzmann said he would like to have 50bps rates hikes in all of the March, May, June and July meetings.

“I expect it to take a very long time for inflation to come down,” the Austrian central bank Governor told Handelsblatt. “My hope is that within the next 12 months we will have reached the peak of interest rates.”

“If we want to get inflation back to two percent in the foreseeable future, we have to be restrictive,” Holzmann said, arguing that only a 4% deposit rate will start restricting growth.

Eurozone Sentix dropped to -11.3, stagnation could turn into renewed recession worries

Eurozone Sentix Investor Confidence index dropped from -8 to -11.1, much worst than expectation of an improvement to -5.6.

Current Situation index rose from -10.0 to -9.3, hitting the highest level since June 2022. But that means the economy is “currently in a stagnation phase at best”.

Expectations index dropped notably from -6.0 to -13.0. “Over the next six months, investors expect the Eurozone economy to deteriorate.”

Sentix added, “this stagnation phase could soon turn into renewed recession worries if the negative economic expectations materialise.”

Eurozone retail sales volume rose 0.3% mom in Feb

Eurozone retail sales volume rose 0.3% mom in February, well below expectation of 1.0% mom. Volume of retail trade increased by 1.8% for food, drinks and tobacco and by 0.8% for non-food products, while it decreased by -1.5% for automotive fuels.

EU retail sales volume rose 0.3% mom. Among Member States for which data are available, the highest monthly increases in the total retail trade volume were registered in the Netherlands (+4.9%), Luxembourg (+4.6%) and Slovenia (+4.1%). The largest decreases were observed in Austria (-9.8%), Slovakia (-1.4%) and Hungary (-0.6%).

UK PMI construction rose to 54.6, returned to growth with increasing optimism

UK PMI Construction rose sharply from 48.4 to 54.6 in February, well above expectation of 48.5. It’s also the first expansion reading in three months, and highest since May 2022. S&P Global also noted greater commercial work helped to offset drop in housing activity. Input cost inflation was the lowest since November 2020.

The construction sector returned to growth as commercial work and civil engineering output increased, offsetting a continued weakness in the housing market. Firms attributed the growth to improving global economic conditions and increased client confidence in the commercial segment. Construction companies are increasingly optimistic about the year ahead and expect business to expand, helped by softer inflationary pressures and fewer supplier delays.

Swiss CPI accelerated to 3.4% yoy in Feb, core rose to 2.4% yoy

Swiss CPI rose 0.7% mom in February, above expectation of 0.4% mom. Core CPI (excluding fresh and seasonal products, energy and fuel), rose 0.8% mom. Prices of domestic products rose 0.6% mom. Imported products rose 1.1% mom.

Compared with the same month a year ago, CPI accelerated to 3.4% yoy, up from January’s 3.3% yoy, well above expectation of slowing to 2.9% yoy. Core CPI accelerated to 2.4% yoy, up from 2.2% yoy. Domestic prices accelerated to 2.9% yoy, up from 2.6% yoy. Imported prices slowed to 4.9% yoy, down from 5.2% yoy.

The data should reinforce the case for SNB to maintain its tightening pace and raise interest rates by 50bps to 1.50% on March 23. While some analysts expect a slowdown to 25bps in June, SNB may continue to tighten at the current speed if inflation remains high.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9336; (P) 0.9384; (R1) 0.9408; More…

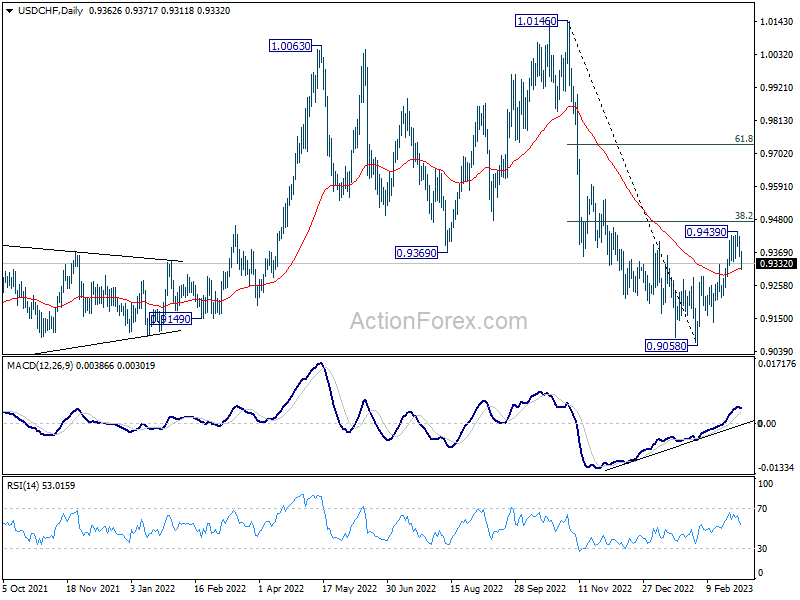

USD/CHF’s break of 0.9340 support indicate short term topping at 0.9439, on bearish divergence condition in 4 hour MACD. More importantly, the corrective rebound from 0.9058 could have completed ahead of 38.2% retracement of 1.0146 to 0.9058 at 0.9474. Intraday bias is back on the downside for 0.9289 resistance turned support first. Decisive break there will bring retest of 0.9058 low. For now, risk will stay on the downside as long as 0.9439 resistance holds, in case of recovery.

In the bigger picture, decline from 1.0146 is seen as part of a long term sideway pattern. As long as 38.2% retracement of 1.0146 to 0.9058 at 0.9474 holds, another fall is in favor through 0.9058. However, sustained trading above 0.9474 will indicate that the medium term trend has reversed, and open up further rally to 61.8% retracement at 0.9730 and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:00 | AUD | TD Securities Inflation M/M Feb | 0.40% | 0.90% | ||

| 07:30 | CHF | CPI M/M Feb | 0.70% | 0.40% | 0.60% | |

| 07:30 | CHF | CPI Y/Y Feb | 3.40% | 2.90% | 3.30% | |

| 09:30 | EUR | Eurozone Sentix Investor Confidence Mar | -11.1 | -5.6 | -8 | |

| 09:30 | GBP | Construction PMI Feb | 54.6 | 48.5 | 48.4 | |

| 10:00 | EUR | Eurozone Retail Sales M/M Feb | 0.30% | 1.00% | -2.70% | -1.70% |

| 15:00 | USD | Factory Orders M/M Jan | -1.50% | 1.80% | ||

| 15:00 | CAD | Ivey PMI Feb | 55.9 | 60.1 |

{kind=link}