US stock futures bounce while treasury yields weaken following release of January’s PCE inflation data, which showed slowdown in both headline and core inflation rates as anticipated. This development provided some relief to investors, who were concerned that disinflation progress might have come to a halt. Fed should remain more likely start interest rate cuts in the first half of the year, rather than waiting until later. The development also led to mild weakening of Dollar.

As for the day Yen is maintaining its position as the strongest currency, fueled by hawkish comments from a BoJ official. Yet, there is no clear follow through momentum for now. Traders are probably awaiting more definitive guidance from BoJ Governor Kazuo Ueda on the anticipated rate hike before making significant bets.

Elsewhere, Australian Dollar and the Canadian Dollar are trailing Yen as the second and third strongest currencies, respectively. On the other end of the spectrum, Sterling and Swiss Franc are underperforming, with New Zealand Dollar not far behind. Euro and the Dollar are mixed in the middle.

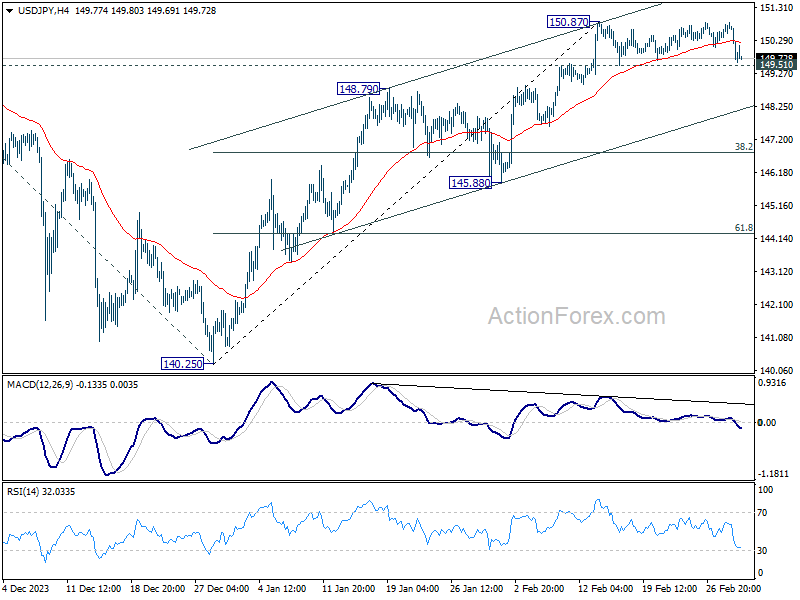

Technically, 149.51 support in USD/JPY remains a major focus for the rest of the session. Firm break there would open up deeper decline to channel support (now at 148.14), even as a corrective move. However, strong bounce from the current level would likely resume the rise from 140.25 through 150.87 instead.

In Europe, at the time of writing, FTSE is up 0.55%. DAX is up 0.57%. CAC is down -0.02%. UK 10-year yield is up 0.155 at 4.272. Germany 10-year yield is down -0.001 at 2.456. Earlier in Asia, Nikkei fell -0.11%. Hong Kong HSI fell -0.15%. China Shanghai SSE rose 1.94%. Singapore Strait Times rose 0.09%. Japan 10-year JGB yield rose 0.0160 to 0.714.

US PCE prices slows to 2.4% yoy in Jan, core PCE down to 2.8% yoy

US personal income rose USD 233.7B or 1.0% mom in January, well above expectation of 0.5% mom. Personal spending rose USD 43.9B or 0.2% mom, matched expectations.

Headline PCE price index rose 0.3% mom, matched expectations. Core PCE price index (excluding food and energy) rose 0.4% mom, matched expectations. Services prices rose 0.6% mom while goods prices decreased -0.2% mom. Food prices rose 0.5% mom and energy prices fell -1.4% mom.

From the same month a year ago, headline PCE price index slowed from 2.6% yoy to 2.4% yoy. Core PCE price index slowed from 2.9% yoy to 2.8% yoy. Both matched expectations. Services prices were up 3.9% yoy while goods prices fell -0.5% yoy. Food prices rose 1.4% yoy and energy prices fell -4.9% yoy.

US initial jobless claims rises to 215k, above expectation 210k

US initial jobless claims rose 13k to 215k in the week ending February 24, above expectation of 210k. Four-week moving average of initial claims fell -3k to 212.5.

Continuing claims rose 45k to 1905k in the week ending February 17. Four-week moving average of continuing claims rose 3k to 2880, highest since December 11 2021.

Canada’s GDP flat in Dec, up 0.2% qoq in Q4

Canada’s GDP rose 0.2% qoq in Q4, recovering from Q3’s -0.1% decline. Statistics Canada noted that higher exports (up 1.4%) and reduced imports (down -0.4%) fuelled GDP growth, but this was moderated by a decline in business investment.

In December, GDP was flat for the month, below expectation of 0.2% mom. Goods-producing industries contracted -0.2% mom. Services-producing industries were largely unchanged. Advance information indicates that real GDP rose 0.4% mom in January.

Swiss GDP grows 0.3% qoq in Q4, abv exp 0.1% qoq

Switzerland’s GDP grew by 0.3% qoq in Q4, slightly surpassing expectation of 0.1% qoq growth.

Despite this modest uptick, the nation faced slight decline in domestic final demand, which fell by -0.3%. This downturn was primarily driven by a significant, broad-based decrease in investments in equipment, plummeting by -2.5%. Construction investment also fell by by -0.3%, which in turn, led to -0.2% decrease in the construction industry.

Meanwhile, private consumption saw a marginal increase of 0.3%, buoyed by spending in housing, health, mobility, and foreign travel sectors. However, spending on food and other retail goods witnessed a decline. The retail and trade sectors also reported contraction, with retail dropping by -0.3% and trade by -1.0% . Additionally, imports of goods and services showed weak performance, registering 0.7% increase after adjusting for sporting events.

Swiss KOF falls to 101.6 in Feb, rather positive economic signals intact

Swiss KOF Economic Barometer fell from 102.5 to 101.6 in February, below expectation of 102.0. Despite this marginal cooling, KOF maintains an optimistic stance regarding the Swiss economy, asserting that “the rather positive economic signals in Switzerland remain intact.”

This assertion is particularly relevant to manufacturing and construction sectors, which have seen an improvement in their outlooks. Contrastingly, projections for financial and insurance services, hospitality, other services, and foreign demand have experienced a downturn. Meanwhile, forecast for private consumption within Switzerland remains stable.

BoJ’s Takata urges policy shift, time to exit ultra-accommodative stance

In a significant speech today, BoJ board member Hajime Takata emphasized the need for a “nimble and flexible response” to the nation’s monetary policy strategy, and called for the moves away from the current “extremely accommodative monetary policy”.

He outlined several measures for consideration, including exiting yield curve control, moving away from negative interest rates, and revising the BoJ’s commitment to expanding its monetary base until inflation consistently exceeds the 2% target.

Takata’s remarks come at a time when Japan appears to be on the cusp of meeting its long-sought-after inflation target of 2%. He noted, “While there are some economic uncertainties, I feel that we’re finally seeing prospects for achieving our 2% inflation target.”

Furthermore, Takata highlighted the positive momentum in spring wage negotiations, with many companies proposing wage hikes surpassing those of 2023. This trend towards higher wages, coupled with the corporate sector’s growing resilience to yield increases upon the exit of current monetary policies, underscores a strengthening economic foundation.

Japan faces steepest industrial decline in nearly four years, -7.5% mom drop in Jan

Japan’s industrial production faced a significant downturn in January, recording a -7.5% mom decline in production, marking the sharpest drop since May 2020. This downturn was slightly more severe than the anticipated -7.3% mom, with a widespread decrease across 14 of the 15 surveyed industries. Motor vehicles sector experienced the most substantial fall, plummeting by -17.8% mom, driven by declines in regular passenger cars and electrical drive systems.

Manufacturers remain somewhat optimistic, anticipating a rebound with of 4.8% in output for February and a further 2.0% rise in March, as surveyed by the Ministry of Economy, Trade and Industry. However, these forecasted gains are deemed insufficient by METI officials to fully counterbalance the steep January decline.

In contrast to the industrial sector’s struggles, Japan’s retail sales presented a brighter picture, rising 2.3% yoy in January, surpassing the expected 2.0% increase.

RBNZ’s Orr confident on bringing down inflation, highlights global risks

RBNZ to said in a conversation with Radio New Zealand that the central bank RBNZ’s very confident on returning inflation to target band of 1%-3% by the second half of 2024, with a goal to hit near 2% midpoint in 2025.

Highlighting the broader context, Orr pointed out that key risks to this positive outlook are mostly global. Domestic economy aligns with RBNZ’s expectations. Orr noted the current “subdued spending” and “declined” inflation levels as outcomes of the existing monetary policy settings and trade conditions.

Later in the day, Orr told a parliamentary committee the importance of “retaining a restrictive stance with the official cash rate,” as a pivotal factor for ensuring the forecasted return to target inflation levels.

NZ ANZ business confidence falls to 34.7, patchy economy

New Zealand ANZ Business Confidence fell from 36.6 to 34.7 in February. Own activity outlook rose from 25.6 to 29.5. Inflation expectations fell from 4.28% to 4.03%. Pricing intentions eased from 50% to 48%, continuing their sideways trend of recent months. Cost expectations fell from 75.6 to 73.5. Wages expectation fell from 81.4 to 78.9.

ANZ’s describes the economy as “patchy,” with visible “green shoots” in some sectors, yet acknowledges the “ongoing challenges” facing other segments. The survey does not imply the “economy is rolling over” or that “inflation has been beaten”.

Australia’s retail sales rises 1.1% mom in Jan, stagnates in trend terms

Australia’s retail sales rose 1.1% mom in January, below expectation of 1.7% mom. This increase marks a recovery from December’s significant -2.1% mom decline, where consumer spending retracted following the Black Friday sales rush in November.

According to Ben Dorber, ABS head of retail statistics, retail turnover has effectively returned to the levels observed in September 2023. Additionally, “retail turnover was unchanged in trend terms in January,” indicating that, despite the month’s positive performance, the broader trend reflects a period of stagnation in retail sales when considering the volatility of the past few months.

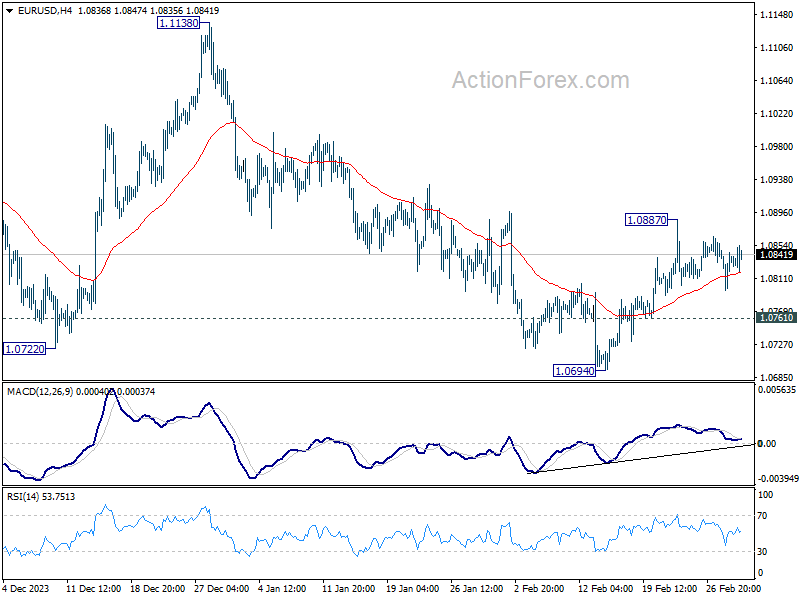

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0807; (P) 1.0829; (R1) 1.0860; More…

EUR/USD recovers mildly in early US session but stays in range below 1.0887. Intraday bias stays neutral at this point. On the upside, break of 1.0887 and sustained trading above 55 D EMA (now at 1.0832) will affirm the case that fall from 1.1138 has completed. Stronger rally would then be seen back to 1.1138. However, break of 1.0761 will turn bias back to the downside for retesting 1.0694 support.

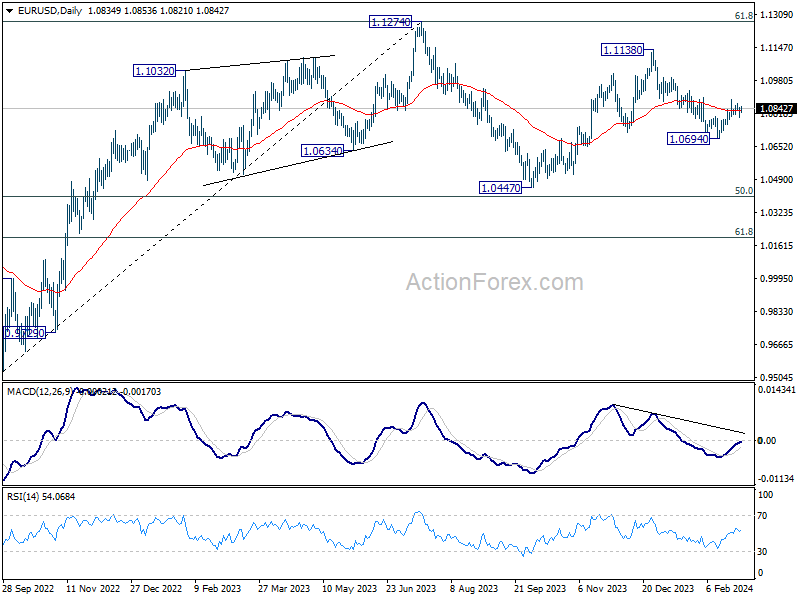

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Industrial Production M/M Jan P | -7.50% | -7.30% | 1.40% | |

| 23:50 | JPY | Retail Trade Y/Y Jan | 2.30% | 2.00% | 2.30% | |

| 00:00 | NZD | ANZ Business Confidence Feb | 34.7 | 36.6 | ||

| 00:30 | AUD | Retail Sales M/M Jan | 1.10% | 1.70% | -2.70% | -2.10% |

| 00:30 | AUD | Private Sector Credit M/M Jan | 0.40% | 0.40% | 0.40% | |

| 00:30 | AUD | Private Capital Expenditure Q4 | 0.80% | 0.40% | 0.60% | 0.30% |

| 05:00 | JPY | Housing Starts Y/Y Jan | -7.50% | -7.50% | -4.00% | |

| 07:00 | EUR | Germany Retail Sales M/M Jan | -0.40% | 0.50% | -1.60% | |

| 07:45 | EUR | France GDP Q/Q Q4 | 0.10% | 0.00% | 0.00% | |

| 08:00 | CHF | KOF Economic Barometer Feb | 101.6 | 102 | 101.5 | 102.5 |

| 08:00 | CHF | GDP Q/Q Q4 | 0.30% | 0.20% | 0.30% | |

| 08:55 | EUR | Germany Unemployment Change Feb | 11K | 10K | -2K | |

| 08:55 | EUR | Germany Unemployment Rate Feb | 5.90% | 5.80% | 5.80% | |

| 09:30 | GBP | M4 Money Supply M/M Jan | -0.10% | 0.30% | 0.50% | |

| 13:00 | EUR | Germany CPI M/M Feb P | 0.40% | 0.50% | 0.20% | |

| 13:00 | EUR | Germany CPI Y/Y Feb P | 2.50% | 2.60% | 2.90% | |

| 13:30 | CAD | GDP M/M Dec | 0.00% | 0.20% | 0.20% | |

| 13:30 | USD | Personal Income M/M Jan | 1.00% | 0.50% | 0.30% | |

| 13:30 | USD | Personal Spending Jan | 0.20% | 0.20% | 0.70% | |

| 13:30 | USD | PCE Price Index M/M Jan | 0.30% | 0.30% | 0.20% | |

| 13:30 | USD | PCE Price Index Y/Y Jan | 2.40% | 2.40% | 2.60% | |

| 13:30 | USD | Core PCE Price Index M/M Jan | 0.40% | 0.40% | 0.20% | |

| 13:30 | USD | Core PCE Price Index Y/Y Jan | 2.80% | 2.80% | 2.90% | |

| 13:30 | USD | Initial Jobless Claims (Feb 23) | 215K | 210K | 201K | 202K |

| 14:45 | USD | Chicago PMI Feb | 47.9 | 46 | ||

| 15:00 | USD | Pending Home Sales M/M Jan | 1.00% | 8.30% | ||

| 15:30 | USD | Natural Gas Storage | -86B | -60B |

{kind=link}