The Flash Harmonized Consumer Price Index (HCPI) and initial GDP growth estimates will be on the watchlist early on Wednesday. Following a dovish policy meeting by the European Central Bank last week, the data could assure markets that further monetary easing is the right choice for the months coming ahead. What markets don’t know yet though is the size and the duration of the upcoming stimulus package, with investors and hence the euro eagerly waiting this week’s data to give some direction.

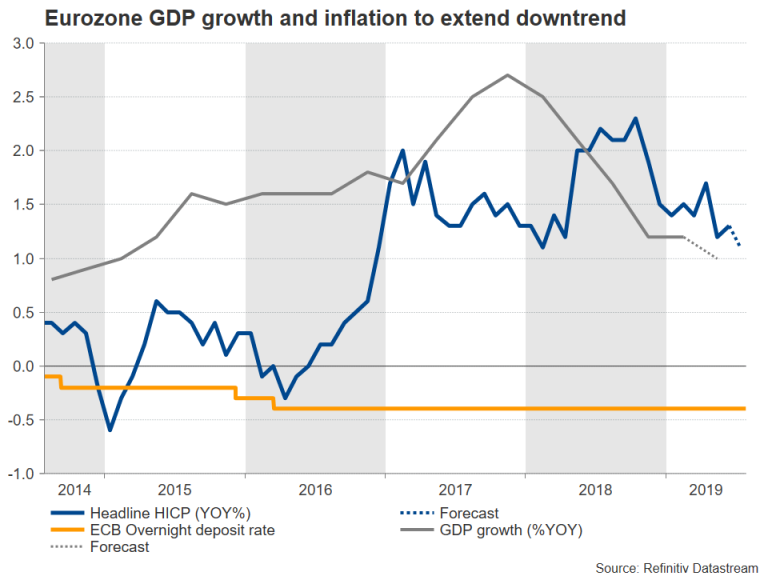

GDP growth and inflation slowdown to continue

Recent business PMI surveys out of the EU and the powerhouse Germany arrived weaker and so the EU flash inflation and GDP growth readings are forecast to do the same on Wednesday at 0900 GMT.

Both the headline and the core HCPI measures are expected to slip to 1.1% year-on-year (y/y) from 1.3% in June according to Refinitiv estimates despite a robust labor market. Separately, the preliminary GDP report for the second quarter is likely to be even discouraging, with forecasts suggesting a softer growth of 0.2% q/q compared to 0.4% in the previous quarter, which could result in an annual expansion of 1.0% versus 1.2% previously.

New stimulus package might not be easy decision

Compared to its previous policy meetings, the ECB added the word “lower” to its forward guidance on interest rates last week, admitting that a cut in the deposit rate is very likely in the coming months. Policymakers also messaged that this might not be the only option to stimulate the eurozone economy but other measures “such as the design of a tiered system for reserve remuneration” which would reduce the charge for some banks to store their reserves in the central bank, as well as, a second round of quantitative easing might accompany the reduction in borrowing costs.

Following Draghi’s press conference speech, markets turned almost certain that a 0.10bps rate cut could be delivered as soon as in September when the central bank updates its economic projections and starts a new series of quarterly targeted longer-term refinancing operations (TLTRO-III).

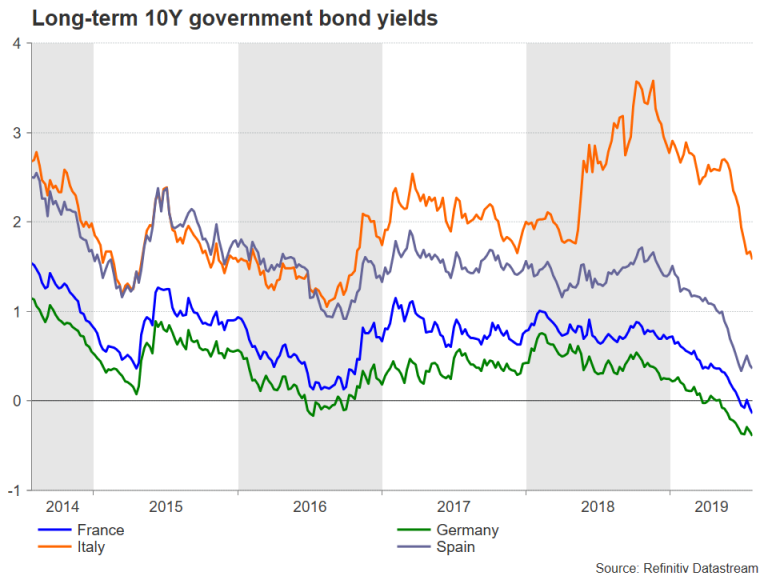

Yet, analysts are still in the dark concerning “the size and the composition” of a potential new asset purchase program. For example, the ECB could find it hard to purchase government bonds from Germany where the government is running an excessive budget surplus. Note that a government issues new bonds when total spending exceeds the revenue it collects through taxation. Worth of mention is also the fact that the ECB has set out its bond purchases in proportion to the amount each country has paid into the central bank, meaning that larger economies get the most. Besides, questions are also arising about how willing the ECB is to buy bonds from Germany and France where the 10-year yields are currently negative.

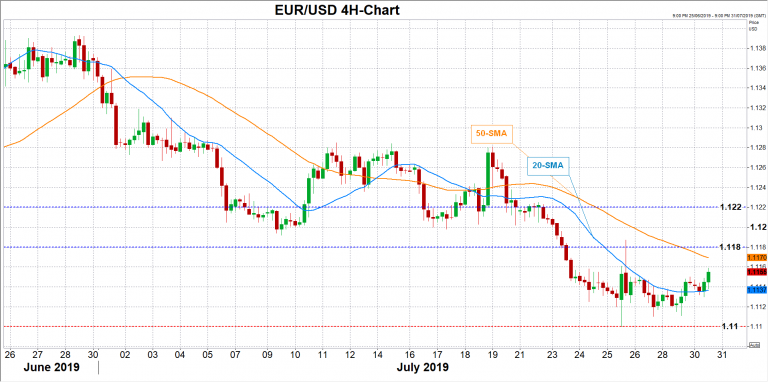

Technical analysis

All in all, Draghi could inject a bigger amount of liquidity through its monetary policy and for a longer period if economic terms in the eurozone deteriorate along with Brexit and trade developments. On Wednesday, flash GDP growth and inflation figures could provide insight on the bloc’s performance, and hence evidence on how big the stimulus wave could be, adding more volatility to the euro. A worse-than-expected outcome may likely push EURUSD under the 1.1100 strong support area and towards the 1.1000 psychological mark.

Alternatively, in the event of a positive surprise, EURUSD could look for resistance within the 1.1180-1.1220 area.

Keep in mind that the Federal Open Market Committee is highly anticipated to slash its funds rate on Thursday and any change in the language could shake the euro as well.

{kind=link}