Market sentiment continue to flip-flop on flowing headlines regarding US debt ceiling negotiations. But then, it should be remembered that it’s not done until it’s done. So uncertainties and volatility still lie ahead. Yen is the consistent one extending its near term decline. Commodity currencies are rebounding with Sterling. But the more important development is in Dollar’s rally extension against Euro and Swiss France.

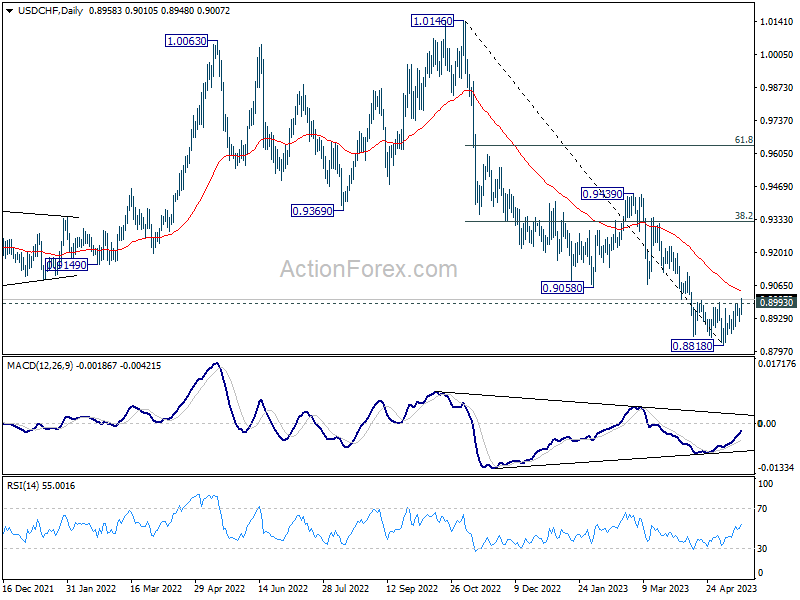

Technically, USD/CHF’s break of 0.8993 resistance today now argues that rebound from 0.8818 might at least correcting whole fall from 1.0146. This is supported by bullish convergence condition in D MACD. Next focus is the resistance zone between 55 D EMA (now at 0.9044) and 0.9058 support turned resistance. Sustained break there will affirm this case and bring further rally to 38.2% retracement of 1.0146 to 0.8818 at 0.9325. Meanwhile, to aid the rally, EUR/CHF better takes out 0.9780 minor resistance too.

In Europe, at the time of writing, FTSE is down -0.05%. DAX is up 0.49%. CAC is up 0.15%. Germany 10-year yield is down -0.0424. Earlier in Asia, Nikkei rose 0.84%. Hong Kong HSI dropped -2.09%. China Shanghai SSE dropped -0.21%. Singapore Strait Times dropped -1.25%. Japan 10-year JGB yield dropped -0.0264 to 0.369.

BoE Bailey: Will adjust rate further if inflation pressures persist

BoE Governor Andrew Bailey pledged in a speech, “I can assure you that the MPC will adjust Bank Rate as necessary to return inflation to target sustainably in the medium term, in line with its remit.”

“If there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required,” he added.

In the baseline modal projection of May Report, which is conditional on a market-implied path for interest to peak at 4.75% in Q4, inflation will fall materially below the 2% target in the medium term.”

However, he noted, “risks to inflation are skewed significantly to the upside”, primarily reflecting the possibility of more persistence in domestic wage and price setting. Also, the “unwinding of second-round effects may take longer than it did for them to emerge”.

This “asymmetry” was not made as part of the baseline modal projection. Instead, “we think of this as a material upside risk to the inflation outlook over the medium term.”

Eurozone CPI finalized at 7% yoy in Apr, CPI core at 5.6% yoy

Eurozone CPI was finalized at 7.0% yoy in April, up from March’s 6.9% yoy. The highest contribution to came from food, alcohol & tobacco (+2.75%), followed by services (+2.21%), non-energy industrial goods (+1.62%) and energy (+0.38%). CPI core (excluding energy, food, alcohol & tobacco) was finalized at 5.6% yoy, down from prior month’s 5.7% yoy.

EU CPI was finalized at 8.1% yoy. The lowest annual rates were registered in Luxembourg (2.7%), Belgium (3.3%) and Spain (3.8%). The highest annual rates were recorded in Hungary (24.5%), Latvia (15.0%) and Czechia (14.3%). Compared with March, annual inflation fell in twenty-two Member States and rose in five.

Japan’s economy bounced back in Q1, up 1.6% annualized, 0.4% qoq

Japan’s economy delivered a robust performance in Q1, expanding at annualized rate of 1.6%, which significantly surpassed expectation of 0.7%. This marks the first expansion in three quarters, thanks to a potent combination of strong private consumption and a rebound in inbound tourism.

In terms of real GDP, adjusted for inflation, there was an increase of 0.4% qoq, beating the forecast growth of 0.1% qoq. The positive data signals a welcome resurgence in Japan’s economy, signaling a potential turn-around after short period of technical recession.

Looking into the details, private consumption for the quarter rose by 0.6%, driven by robust demand for cars and durable goods. Concurrently, consumers boosted spending on services such as dining out, culminating in the fourth consecutive quarterly gain. Meanwhile, capital spending rose by 0.9%, aided by increased car-related investments and marking the first increase in two quarters.

However, not all sectors exhibited positive trends. Exports took a hit, declining by -4.2% due to a slump in shipments of cars and machinery used for chip production. Imports also fell by 2-.3%. Public investment remained largely flat.

Australia wage growth accelerated to 0.8% in Q1, highest in over a decade

Australia wage price index posted 0.8% qoq increase in Q1 2023, slightly short of expected 0.9% rise. Despite this, annual wage growth accelerated to 3.7%, marking the highest level since Q3 2012. This uptick is attributable to a combination of factors, including low unemployment, tight labour market, and high inflation.

Private sector emerged as the primary engine of growth, with wages climbing 0.8% over Q1 and experiencing an annual rise of 3.8%. According to Leigh Merrington, ABS’s acting head of prices statistics, several private sector industries witnessed an annual wage growth exceeding 4%, with the remaining industries all recording an annual growth above 3%.

In the public sector, the highest quarterly (0.9%) and annual (3.0%) wage growth in a decade was reported. Increase in public sector wages is attributed to outcomes from enterprise agreement bargaining, regular scheduled rises, and higher wage caps.

Merrington further highlighted wage outcomes for Q1 2023, stating, “There was a continued lift in the share of jobs receiving wage rises of between 4 and 6 per cent, which is the highest share since 2009. The share of jobs with a wage rise of 2 per cent or less has fallen from over 50 per cent in mid-2021 to less than 20 per cent.”

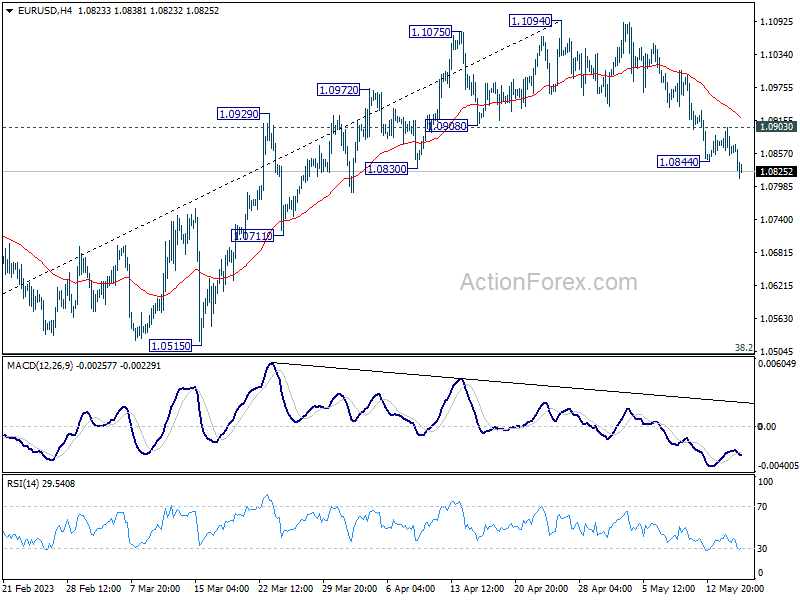

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0844; (P) 1.0874; (R1) 1.0894; More…

EUR/USD’s fall from 1.1094 short term top resumed after brief consolidations. Intraday bias is back on the downside. Current fall is seen as correcting whole up trend from 0.9534. Deeper decline would be seen to 1.0515 cluster support, 38.2% retracement of 0.9534 to 1.1094 at 1.0498. On the upside, above 1.0903 minor resistance will turn intraday bias neutral first.

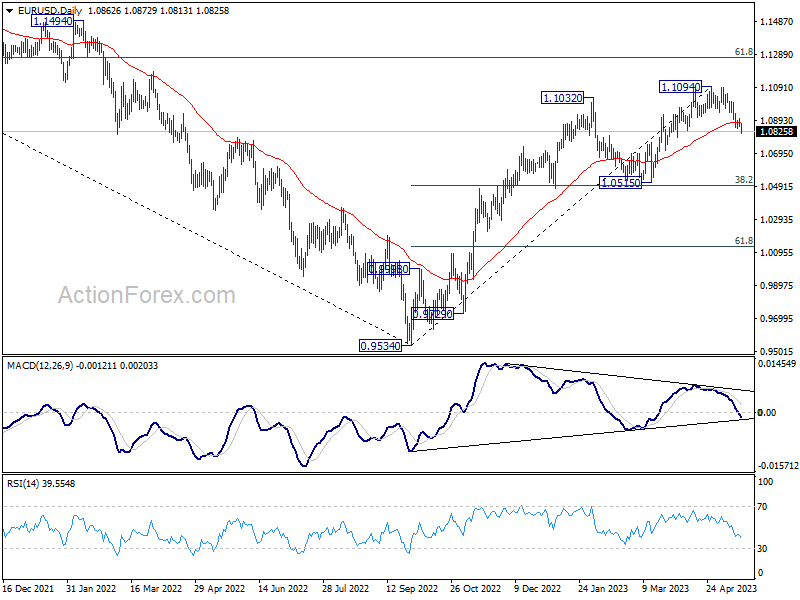

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | GDP Annualized Q1 P | 0.40% | 0.20% | 0.10% | |

| 23:50 | JPY | GDP Deflator Y/Y Q1 P | 2.00% | 2.00% | 1.20% | |

| 01:30 | AUD | Wage Price Index Q/Q Q1 | 0.80% | 0.90% | 0.80% | |

| 04:30 | JPY | Industrial Production M/M Mar F | 1.10% | 0.80% | 0.80% | |

| 08:00 | EUR | Italy Trade Balance (EUR) Mar | 7.54B | 2.50B | 2.11B | |

| 09:00 | EUR | Eurozone CPI Y/Y Apr F | 7.00% | 7.00% | 7.00% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Apr F | 5.60% | 5.60% | 5.60% | |

| 12:30 | USD | Housing Starts Apr | 1.42M | 1.40M | 1.42M | 1.43M |

| 12:30 | USD | Building Permits Apr | 1.42M | 1.44M | 1.43M | 1.37M |

| 14:30 | USD | Crude Oil Inventories | -1.5M | 3.0M |

Interventions?")

{kind=link}