{kind=link}

Sunrise Market Commentary

- Rates: US political developments weigh on US Treasuries

The US Note future loses ground this morning after the successful US Senate tax vote and the erroneous Flynn report. We expect the Bund to move back in its sideways range after the European opening. The eco calendar is empty today, but heats up later this week in the US with payrolls on Friday. - Currencies: USD gains only modestly after approval of Senate tax bill

US political headlines sent the dollar in a roller-coaster ride on Friday. This morning, markets react mostly positive to the approval of the US tax bill in the Senate. The approval could help to put a ST floor for the dollar. However, ongoing political noise might prevent a sustained USD rebound ahead of next week’s Fed meeting.

The Sunrise Headlines

- US stock markets closed 0.2% to 0.4% lower on Friday, nervously awaiting the outcome of the US Senate vote on tax reforms. Asian markets show a very mixed picture overnight, with daily changes ranging between -0.5% and +0.5%.

- US Senate Republicans narrowly approved the most sweeping rewrite of the US tax code in three decades, slashing the corporate tax rate and providing temporary tax-rate cuts for most Americans.

- Congressional GOP leaders hope to pass a two-week spending bill before the federal government runs out of money by Saturday, but resistance among conservative Republicans and some Democrats could derail their plans with little time to spare.

- Major central banks must ensure their efforts to gradually lift interest rates prove effective enough to cool some already "frothy" financial markets, the Bank for International Settlements (BIS) said in its latest report.

- Britain and the EU are on the brink of sealing a Brexit divorce deal on Monday, as Theresa May travels to Brussels with potential solutions in sight for the two biggest political obstacles to opening trade talks.

- A coalition of movements pushing for greater autonomy for Corsica looks likely to dominate a newly constituted assembly on the French Mediterranean island of Corsica, returns from the first round of voting show.

- Today’s eco calendar is uneventful with EMU PPI data, the UK construction PMI and US factory orders

Currencies: USD Gains Only Modestly After Approval Of Senate Tax Bill

Dollar cautiously higher on Tax bill approval

The dollar initially held up well on Friday even as sentiment in Europe was outright risk-off. The dollar rebounded further early in US dealings, but fell off a cliff on headlines that Michael Flynn admitted to have lied to the FBI on contacts with Russia, potentially resulting in further trouble for the US president. The decline was short-lived as the debate on the Tax bill in the US Senate made progress. USD/JPY closed the session at 112.17 (from 112.54). EUR/USD finished the session at 1.1896 (from 1.1904 on Thursday).

Asian equity markets trade mixed this morning after the approval of the Tax bill in the US Senate. Investors remain cautious as the House of Representatives and the Senate still have to the make a reconciliation on their two proposals. US yields are modestly higher and so is the dollar. USD/JPY profits most and trades in the high 112 area. Japanese equities underperform despite the rise of USD/JPY. EUR/USD trades in the 1.1865 area, within the range that reigned for most of last week. Ongoing noise on the Russia investigation against aides of President Trump might prevent a bigger positive reaction to the Senate Tax bill.

The eco calendar is thin today. EMU PPI is no market mover. US factory orders will be published, but the cyclical component of the report (durable orders) is already available. Any FX reaction should only be of intraday significance, at best. The reaction of global markets to the US tax bill will be an important driver for USD-trading. At the same time, there will remain plenty of political noise from the US (fall-out from the investigation on contacts of Trump’s aides/campaign team with Russia; solution for the debt ceiling). The US calendar is interesting later this week with the non-manufacturing ISM, ADP labour market report and payrolls. We expect the US eco data to confirm the positive drive in the economy.

The dollar showed a mixed picture last week, rebounding against the yen but holding relatively soft against the euro. Even after the approval of the Tax bill, this pattern apparently continues. Markets are still looking forward for the Fed’s rate hike intentions in 2018. This week’s US eco data might be USDsupportive, but we don’t expect a really big directional move ahead of next week’s Fed policy decision/statement

EUR/USD might continue last week consolidation pattern. Unless in case of high profile negative news from the US (or negative risk sentiment) we see no reason for EUR/USD to rise beyond the 1.1961/1.20 area. USD/JPY’s momentum looks a bit more constructive, but the rebound might slow if it isn’t supported by developments on other markets.

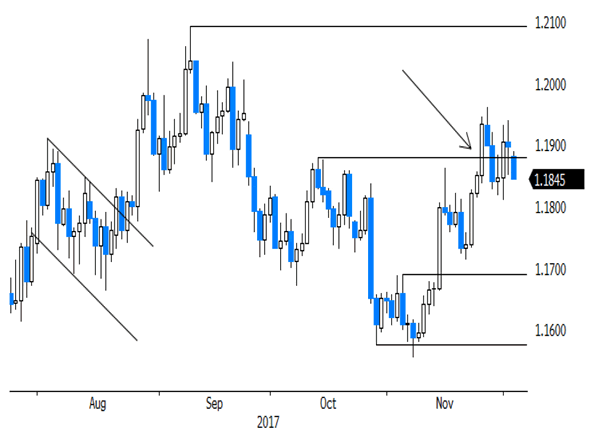

From a technical point of view: EUR/USD set a post-ECB low mid-November, but dollar momentum wasn’t strong enough. EUR/USD regained the 1.1880 MT correction top, opening the way for a full retracement to the 1.2092 top. A return below 1.1713 would signal that the rebound in EUR/USD is aborted. For now, there is no clear technical signal. The USD/JPY momentum deteriorated early November. USD/JPY dropped below the 111.65 neckline, but there was no aggressive follow-through selling. Last week, the pair even succeeded a nice rebound, calling off the downside alert. The pair again hovers in the 110.84/114.73 consolidation range. We amend our ST bias on the pair from negative to neutral.

EUR/USD: rally aborted, but no clear correction signal

EUR/GBP

Brussels meeting to set tone for Sterling trading

Sterling trading showed no clear trend Friday. The issue of the Irish border proves to be a hard nut to crack to make progress in the Brexit negotiations. Sterling lost slightly ground against the euro and the dollar. EUR/GBP hovered mostly in the lower half of the 0.88 big figure and finished the day at 0.8929. Cable traded with a negative bias even as dollar volatility was also visible in this cross rate. The pair closed the session at 1.3477. The UK November manufacturing PMI printed at a very strong 58.2 (from 56.6, 56.5 was expected), but the report had no lasting impact on sterling trading.

The UK construction PMI will be published today. However, the focus of sterling traders will be on Brussels as UK PM May meets with EU’s Juncker. The EU initially set this meeting as the deadline to meet the UK propositions on the separation. However, for now it looks that a final agreement is still too far off. Signals on the progress this weekend were mixed. If there remain substantial obstacles today, sterling might cede some ground short-term.

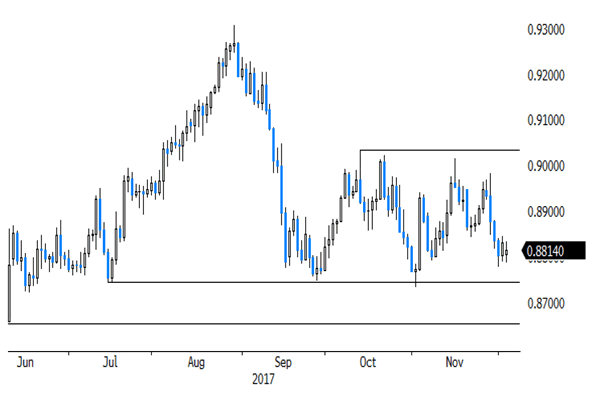

MT view/technical picture: A BoE driven sterling rebound ran into resistance early this month. Sterling declined again as markets anticipated that the rate cycle would be very gradual and limited. EUR/GBP trades in a 0.8733/0.9033 consolidation range. Brexit headlines cause day-to-day gyrations. We changed our ST bias on EUR/GBP from positive to neutral mid-November. The 0.9015/33 area might be tough to break short-term. In case of more positive news on Brexit, return action to the 0.8733 (or below) level is possible ST.

EUR/GBP: decline slows as investors want positive news on Brexit