Live Comments

Fed Holds Rates, Three Dissents Reinforce September Hike Expectations

Federal Reserve left the federal funds target range unchanged at 3.50-3.75%, as widely expected, but the 9-3 vote delivered a more hawkish signal than markets had anticipated. Cleveland Fed President Beth Hammack and Dallas Fed President Lorie Logan both dissented in favor of an immediate 25 basis point hike, as expected. More notably, Minneapolis Fed President Neel Kashkari joined them, suggesting support for tighter policy is broadening within the Committee and reinforcing expectations that another rate increase could come as soon as September.

The statement itself offered few surprises. Policymakers continued to characterize economic activity as expanding at a solid pace despite elevated uncertainty linked partly to the Middle East conflict. The labor market was described as remaining resilient, with job gains keeping pace with workforce growth and unemployment little changed.

On inflation, the Committee reiterated that price pressures remain elevated relative to its 2% objective, while explicitly acknowledging that supply shocks, particularly in energy, have contributed to persistent inflation. The statement again emphasized the Fed's commitment to restoring price stability.

The voting breakdown is likely to attract more market attention than the statement. Markets had largely expected Hammack and Logan to dissent, but Kashkari's decision to support an immediate hike marks a notable shift from one of the Committee's members. Although Chair Kevin Warsh refrained from joining the hawkish camp, the 9-3 outcome nevertheless strengthens the case that support for another rate increase is expanding.

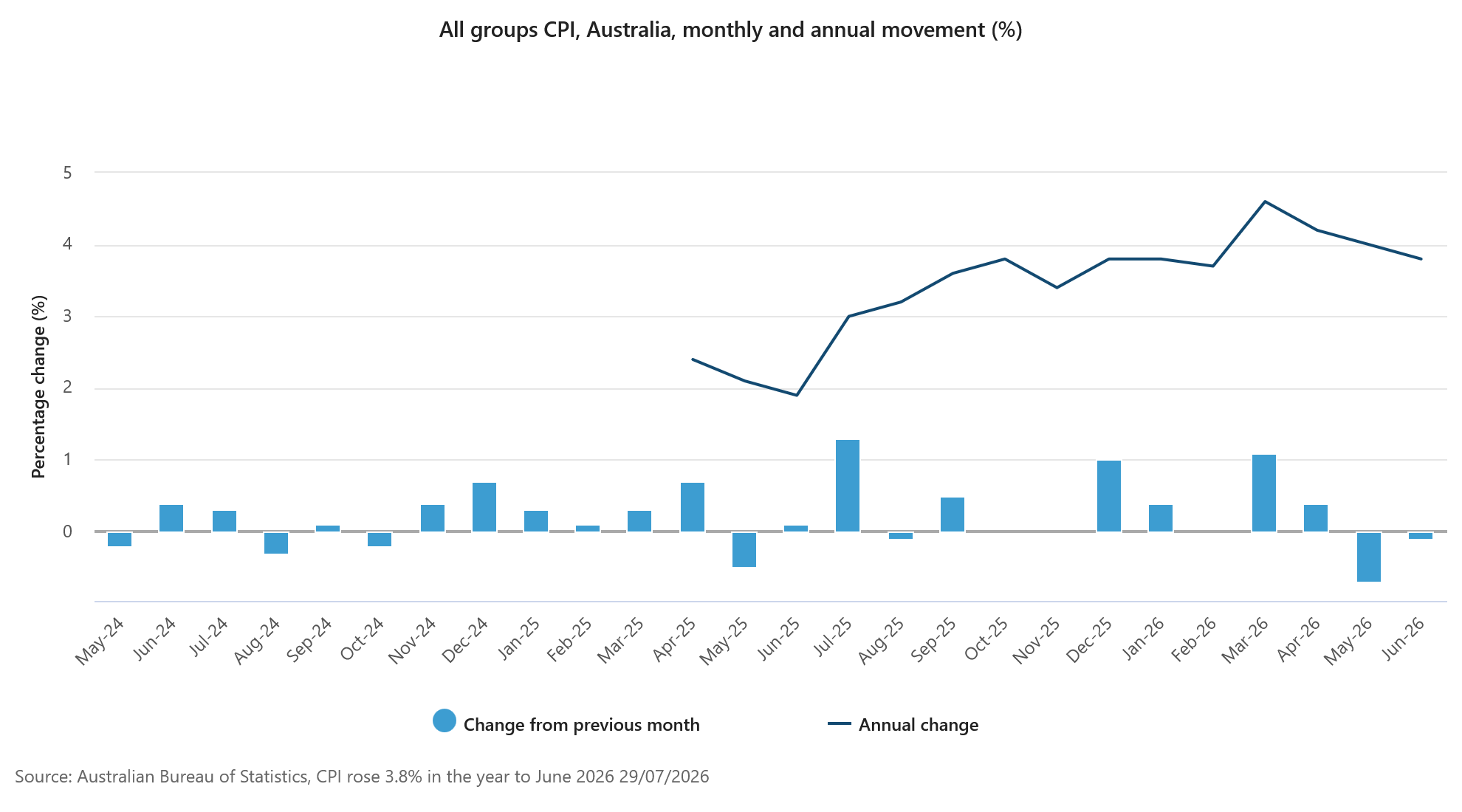

Australia Inflation Slows to 3.8% as Core CPI Misses Forecasts 3.6%

Australia's inflation report offered further evidence that price pressures are gradually easing, strengthening the case for the Reserve Bank of Australia to remain on hold in August. Both the quarterly and monthly measures came in softer than expected, while underlying inflation remained below the RBA's own forecasts. The outcome supports Governor Michele Bullock's recent assessment that inflation is evolving broadly as anticipated and suggests there is little pressing need to resume tightening immediately after three rate hikes already delivered this year.

The quarterly figures, which carry the greatest weight for RBA policy, were particularly encouraging. Headline CPI unexpectedly fell -0.1% qoq in the second quarter, compared with expectations for a 0.7% increase, after rising 1.4% in the first quarter. Annual headline inflation slowed from 4.1% to 3.8%. More importantly, quarterly trimmed mean inflation—the RBA's preferred gauge of underlying price pressures—rose 0.8% qoq, below the 0.9% consensus and matching the pace recorded in the first quarter. On an annual basis, trimmed mean inflation edged up from 3.5% to 3.6%, but remained below both the 3.7% market consensus and the RBA's own 3.8% forecast published in May.

The monthly CPI indicator told a similar story. Headline CPI slowed from 4.0% yoy in May to 3.8% yoy in June, while monthly trimmed mean inflation held steady at 3.6% yoy, undershooting expectations for a rise to 3.7%. On a monthly basis, both the trimmed mean and weighted median increased just 0.3%, while prices excluding volatile items and holiday travel were unchanged. Tradable and goods prices each declined -0.8% mom during the month, extending the disinflation trend in imported goods. Services inflation remained firmer at 4.0% yoy, while non-tradables rose 4.9% yoy, indicating that domestically generated inflation continues to moderate only gradually.

Taken together, the report reinforces the view that the RBA's tightening bias remains intact but the urgency to act has diminished. Inflation remains above target, meaning policymakers are unlikely to declare victory. However, with both headline and underlying inflation coming in below expectations—and trimmed mean inflation also below the RBA's own forecasts—the data give the Board little reason to abandon June's pause and rush into another rate increase in August.

Economic Data

Quarterly CPI (Q2 2026)

| Indicator | Actual | Expected | Previous |

|---|---|---|---|

| CPI q/q | -0.1% | 0.7% | 1.4% |

| CPI y/y | 3.8% | 4.1% | 4.1% |

| Trimmed Mean CPI q/q | 0.8% | 0.9% | 0.8% |

| Trimmed Mean CPI y/y | 3.6% | 3.7% | 3.5% |

Monthly CPI (June 2026)

| Indicator | Actual | Expected | Previous |

|---|---|---|---|

| CPI m/m | -0.1% | 0.2% | -0.7% |

| CPI y/y | 3.8% | 4.0% | 4.0% |

| Trimmed Mean CPI m/m | 0.3% | 0.4% | 0.4% |

| Trimmed Mean CPI y/y | 3.6% | 3.7% | 3.6% |

Key Takeaways

- Australia's inflation report was softer than expected across both the quarterly and monthly measures. Headline and trimmed mean inflation all undershot market forecasts.

- Quarterly trimmed mean inflation—the RBA's preferred measure—rose 0.8% q/q and 3.6% y/y, below both market expectations and the RBA's own May forecast of 3.8%.

- The monthly CPI indicator reinforced the quarterly message, with headline CPI slowing to 3.8% y/y and monthly trimmed mean inflation holding at 3.6% instead of rising as expected.

- The details point to broader disinflation rather than just lower fuel prices. Prices excluding volatile items and holiday travel were flat in June, while tradable and goods prices both fell 0.8%.

- Housing remained the largest source of inflation, rising 6.8% y/y, driven by electricity (+22.4%) following the expiry of government rebates and new dwelling costs (+5.8%) as builders passed through higher labour and material costs.

- Services and non-tradables remain sticky, with annual inflation of 4.0% and 4.9% respectively, indicating domestic inflation pressures have eased only gradually.

- For the RBA, the report weakens the case for an August rate hike. The Bank's tightening bias remains intact, but inflation is evolving slightly better than expected, giving policymakers more room to assess the cumulative impact of previous tightening.

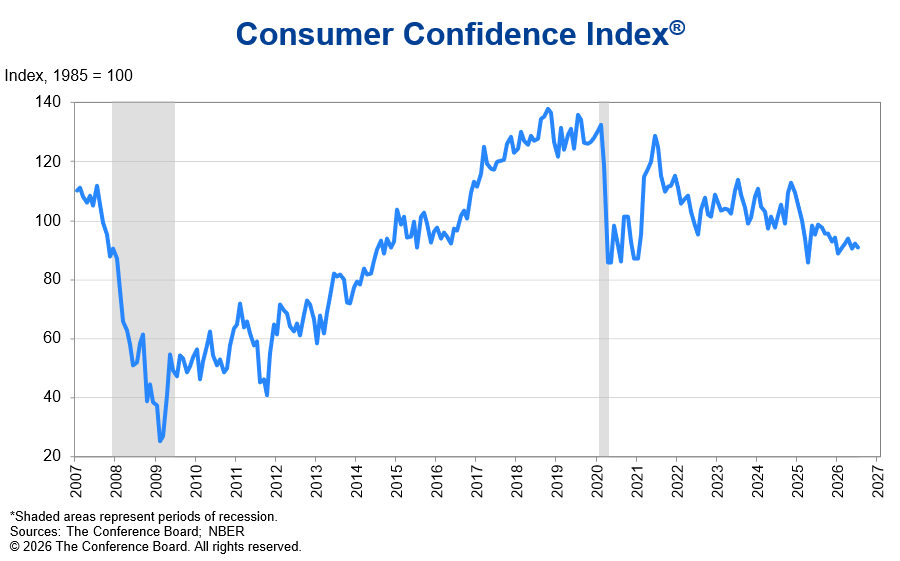

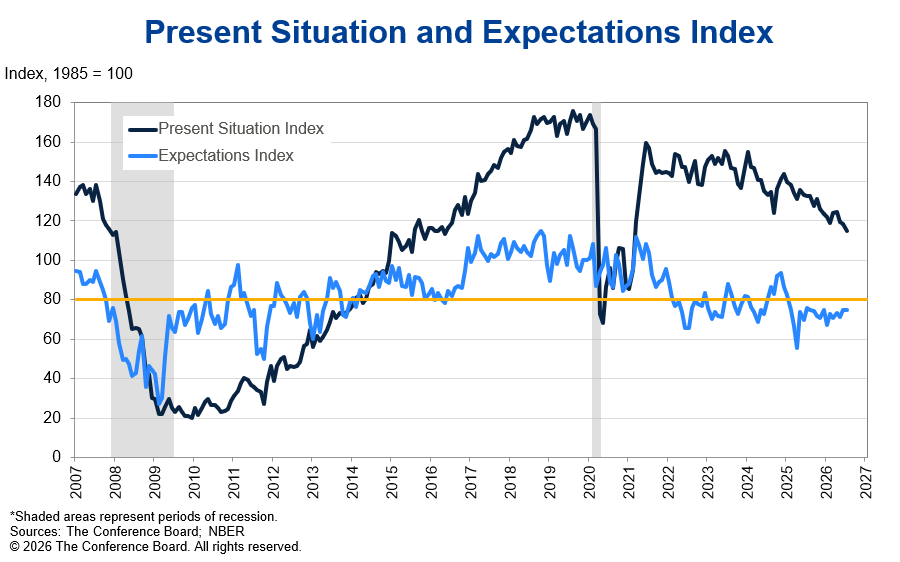

US Consumer Confidence Falls to 90.8 in July, Expectations Remain Below Recession Threshold

US consumer confidence weakened further in July as households grew less upbeat about current business conditions and the labor market, although easing inflation expectations offered a modest offset. The Conference Board's Consumer Confidence Index slipped -1.4 points to 90.8 from an upwardly revised 92.2 in June. The Present Situation Index fell -3.6 points to 114.9, marking its third consecutive monthly decline, while the Expectations Index held steady at 74.7—well below the 80 level that has historically been associated with recession risks.

The latest survey suggests consumers remain unconvinced that economic conditions will improve meaningfully in the months ahead. According to Dana M. Peterson, Chief Economist at The Conference Board, confidence has continued its gradual downtrend since late 2021 as assessments of current business conditions and, to a lesser extent, the labor market deteriorated further. While expectations for future employment became slightly less pessimistic, consumers continued to anticipate little improvement in overall business conditions over the next six months. Household income expectations also moderated, although they remained positive overall.

There were, however, some encouraging signs beneath the headline figures. Both average and median 12-month inflation expectations eased in July, suggesting consumers are becoming somewhat less concerned about future price pressures. Even after recent market volatility, households continued to expect stock prices to rise over the coming year. Meanwhile, 61.3% of respondents still anticipated higher interest rates over the next 12 months, unchanged from June, indicating consumers remain prepared for monetary policy to stay restrictive even as confidence gradually softens.

Economic Data

| Indicator | Actual | Previous |

|---|---|---|

| Consumer Confidence Index | 90.8 | 92.2 |

| Present Situation Index | 114.9 | 118.5 |

| Expectations Index | 74.7 | 74.7 |

| Average 12-mth Inflation Expectations | Lower | Higher |

| Median 12-mth Inflation Expectations | Lower | Higher |

Key Takeaways

- Consumer confidence fell for a second straight month, extending the gradual downtrend that has been in place since late 2021.

- The decline was driven by weaker assessments of current business conditions and the labor market, with the Present Situation Index falling for a third consecutive month.

- The Expectations Index remained at 74.7, below the 80 threshold that has historically been associated with recession risks, suggesting consumers remain cautious about the economic outlook.

- Consumers expect little improvement in business conditions over the next six months, although labor market expectations became slightly less pessimistic.

- Inflation expectations eased further, indicating households are becoming less concerned about future price pressures.

- Despite recent equity market volatility, consumers continued to expect stock prices to rise over the next year.

- A majority (61.3%) still expect interest rates to move higher over the coming 12 months, highlighting expectations that monetary policy will remain restrictive.

Full US Conference Board consumer confidence release here.