{kind=link}

Sunrise Market Commentary

- Rates: White smoke of political scene and strong (?) payrolls

Strong Japanese/Chinese eco data and positive developments on the political scene (government shutdown temporary averted; Brexit agreement) boost risk sentiment and weigh on core bonds. Today’s payrolls report is expected to be strong and could inflict additional losses ahead of next week’s Fed meeting. - Currencies: Will payrolls be strong enough to sustain further USD gains?

The dollar extended its recent gradual rebound yesterday, supported by a positive risk sentiment and ongoing solid interest rate support. Today’s payrolls will decide whether the US currency can extend further gains going into next week’s Fed meeting. Sterling rallied overnight as a Brexit deal was announced for this morning.

The Sunrise Headlines

- US stock markets gained slightly ground yesterday, ending around 0.3% higher. Risk sentiment improved further in Asia overnight with China and Japan gaining up to 1%.

- Congress passed a two-week extension of federal funding that averts a government shutdown this week but defers decisions on spending levels for defense and domestic programs, with December 22 the new deadline.

- UK PM May and EU’s Juncker held a press conference this morning announcing a break-through in the first round of the Brexit negotiations. EU’S Juncker said the EC recommends that sufficient progress has been made on the divorce and indicated that Brexit talks can enter the second phase.

- China’s exports (12.3% Y/Y) and imports (17.7% Y/Y) unexpectedly accelerated last month, though growth could continue cooling amid a government crackdown on financial risks and polluting factories.

- Japan’s economy grew much faster as originally estimated in Q3 (2.5% Q/Qa vs 1.5% Q/Qa) thanks to big gains in capital expenditure (1.1% Q/Q), revised data showed, with expansion seen to continue thanks to buoyant exports.

- Global bank regulators broke a year-long deadlock and closed the book on Basel III. The deal includes new curbs on how banks estimate the risk of mortgages, loans and other assets on their books.

- Today’s eco calendar heats up in the US with the payrolls report. Unemployment rate and average hourly earnings will also be closely watched. UK industrial production and trade balance are on the agenda as well

Currencies: Will Payrolls Be Strong Enough To Sustain Further USD Gains?

Payrolls strong enough to sustain USD gains?

There was no high profile news to guide trading in the major FX cross rates yesterday. The risk-off correction slowed, but at first there was no sustained rebound. Sentiment improved later in the session. US equities finished the session with decent gains. US House and Senate approved a two-week stopgap funding deal after the US close, providing funding for the US government till Dec 22. Gains of the dollar were modest, but the announcement supported an overall constructive market sentiment. EUR/USD closed the session at 1.1773. USD/JPY finished at 113.09.

Asian equities are extending yesterday’s comeback overnight with Japan taking the lead. The economic news flow was mostly positive. Japan Q3 GDP was revised sharply higher from 1.5% Q/Qa to 2.5% Q/Qa, propelled by strong business investment and by a rise in inventories. Japanese real wages rose (0.2% Y/Y) in October. Chinese November imports and exports also beat the consensus by quite a big margin, supporting regional sentiment. The overall positive sentiment via higher core yields supports the dollar rather than regional currencies. USD/JPY extends gains north of 113 (currently 113.40). EUR/USD (1.1765) is holding near recent lows.

US November payrolls provide the last important economic input going into next week’s Fed meeting. The US economy is expect to have added a net 195 000 jobs. The jobless rate is expected unchanged at 4.1%. However, the market focus will be on wages/earnings data. Average hourly earnings are expected to rise 0.3% M/M and 2.7% Y/Y, after disappointing readings in the previous months (0.0% M/M and 2.4% Y/Y in October). If payrolls, and wages in particular, are in line with the consensus (or better), it might already be enough to sustain a gradual further rise of the dollar. Markets could question the Fed rate hike path in 2018 in case of a big miss. We have no reason to expect the data to undershoot the consensus. Maybe there is a slight risk for a rise in the unemployment rate after last months unexpected decline, but that won’t bother markets. This morning, politics dominate the headlines. The news flow (US spending bill and Brexit deal) might support support core yields and the dollar. However, the payrolls probably hold the key for the next directional move. We see a good chance for the payrolls’ outcome to sustain this week’s gradual USD comeback

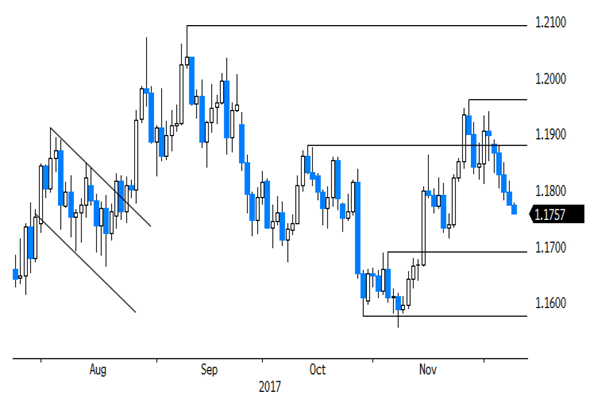

From a technical point of view: EUR/USD set a post-ECB low mid-November, but the dollar’s momentum wasn’t strong enough. EUR/USD settled in a directionless sideways consolidation pattern in the 1.18/19 area. A return below 1.1713 would signal an improvement in the ST USD momentum, going into next week’s Fed meeting. Will today’s payrolls be able to force the break? Next support comes in at 1.1554 (November low). USD/JPY’s momentum deteriorated early November, dropping below the 111.65 neckline. No aggressive follow-through selling occurred though. Last week the pair succeeded a nice rebound, calling off the downside alert. The pair returned again in the 110.84/114.73 consolidation range. We amended our ST bias from negative to neutral. We maintain the view that a sustained break north of 115 won’t be easy.

EUR/USD: USD keeps positive momentum going into the US Payrolls

EUR/GBP

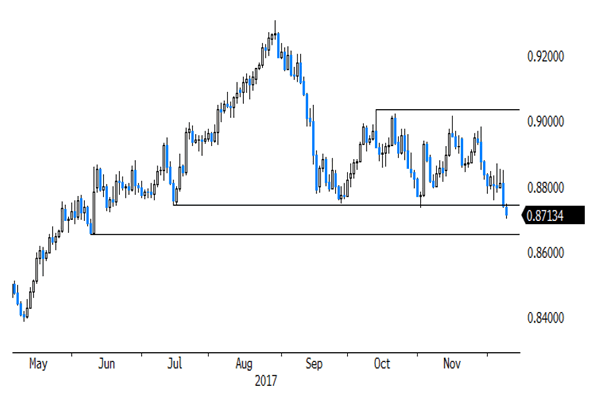

EUR/GBP tests 0.8733 support on Brexit deal

There was little hard news on Brexit yesterday. Sterling was captured in erratic order-driven trading for most of the day. In the evening, rumours/comments from sources close to the UK/Irish government and the European commission suggested that an agreement on the Irish border was within reach and that a deal could be finished as soon as Friday morning. Sterling rallied and EUR/GBP closed the session at 0.8737, testing a first key support area. Cable finished the day at 1.3474.

This morning, all eyes were on Brussels as PM May and EU commission chairman Juncker met at 7 AM. In a press conference, EU’s Juncker said that the European commission considered that enough progress had been made on a divorce deal. It recommends the EU leaders to move to the next stage of the negotiations, to be confirmed at next week EU summit. At the time of writing we have no details of the content of the agreement yet. Sterling rallied in the runup to the announcement of the deal, but the rally slowed during the press conference. EUR/GBP currently hovers in the 0.87 area. For now we remain cautious on further sterling gains from here as long as we have no insight on the details of the deal, e.g. with respect to the Irish border. From a technical point of view, EUR/GBP tries to break first support at 0.8733. In case of a sustained break, next intermediate support comes in in the mid 0.86 area

EUR/GBP testing downside support on Brexit deal