- Markets now treat a December rate hike to 0.75% as the base case.

- Inflation remains above target, with limited improvement in core measures.

- Rising rate expectations are strengthening the yen, supported by a narrowing US – Japan rate spread.

- Higher yields may constrain the BoJ’s pace of tightening next year.

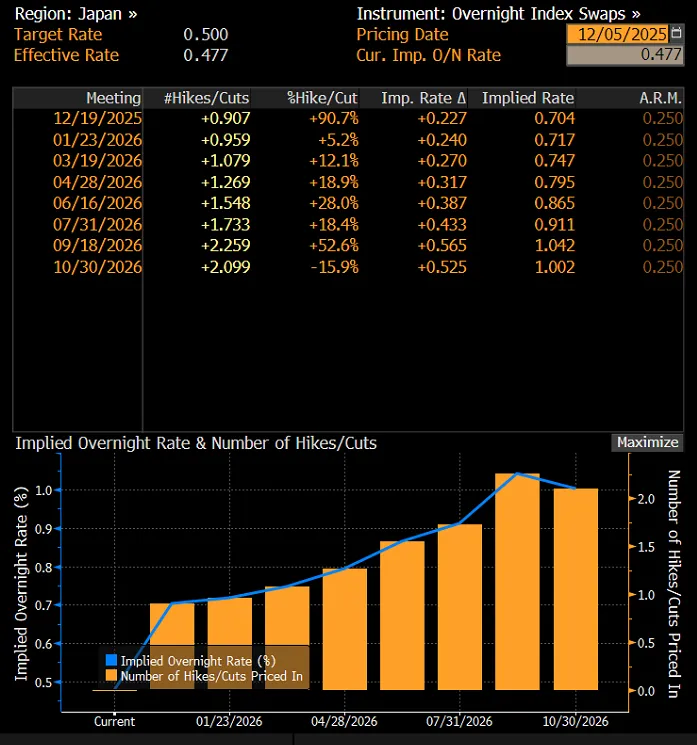

Growing likelihood of a December rate increase

Expectations for another interest rate hike in Japan are clearly strengthening. Although initial hints appeared as early as September, they have intensified markedly in recent days. According to the latest reports, Bank of Japan policymakers are prepared to raise the policy rate to 0.75% at the December meeting – provided no significant disruptions emerge. Markets are now almost fully pricing in such a move, making it the baseline scenario.

Valuation of futures contracts for the future path of interest rates in Japan, source: Bloomberg

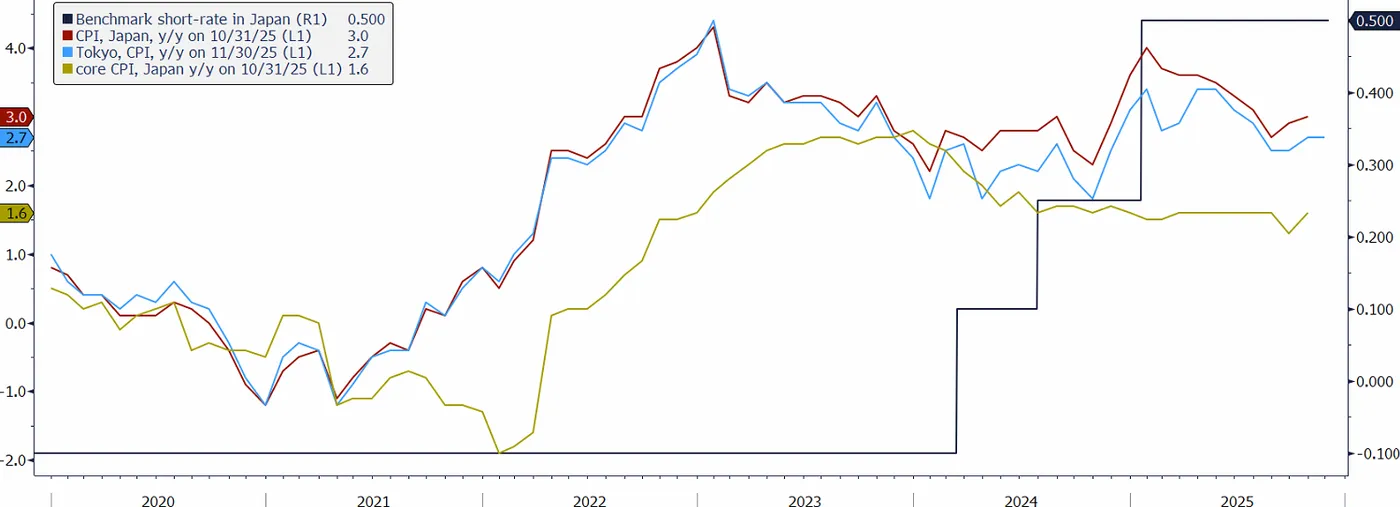

Inflation pressures persist despite partial stabilisation

After a period of uncertainty linked to trade tensions, conditions have stabilised somewhat, while inflation remains above the central bank’s target and continues to strain households. Although much of the price growth stems from volatile food costs – an area monetary policy should not overreact to – the core inflation index in Japan excludes only fresh food and energy. Within this measure, improvement has been limited despite some stabilisation in individual categories.

Inflation measures in Japan and the level of the main interest rate, source: Bloomberg

The risk of credibility loss for the Bank of Japan

A prolonged period of above-target inflation threatens to undermine the central bank’s credibility. For decades, Japan grappled with very low inflation, and markets grew accustomed to price growth below target. Today’s environment is different. Ignoring persistently elevated inflation – even if partly driven by unstable factors – is becoming increasingly difficult to justify.

Yen strengthens as rate expectations rise

Rising expectations for further rate hikes are supporting the yen, which has begun to appreciate against the dollar after weeks of weakness. The USD/JPY pair is trending lower, and the prospect of additional moves suggests further strengthening of the Japanese currency. The Bank of Japan will likely raise rates again in the spring – to around 1% – while the Federal Reserve is expected to continue its easing cycle. As a result, the interest-rate differential between the US and Japan should narrow to roughly 150 basis points by the end of next year, creating further room for yen appreciation.

Higher rates push bond yields up

Higher interest rates come with side effects, especially the rise in Japanese government bond yields. Recent increases have been substantial. While this is unlikely to stop the BoJ from delivering a December hike, it may slow the pace of future actions – the central bank is keen to avoid triggering a sharp sell-off in the debt market, especially as the government’s fiscal package is also exerting upward pressure on yields.

Technical picture of USD/JPY

In the second half of November, the USD/JPY currency pair reached levels corresponding to the peak recorded at the beginning of this year. The exchange rate has ‘returned’ to the upward trend channel, which it broke above last month. Signals coming from the BoJ, together with the technical setup, indicate that the strengthening of the JPY may continue, pushing the pair’s quotations toward even 150.00.

USD/JPY currency pair chart, daily data, source: Tradingview

{kind=link}