- Precious metals rebounded, but remain expensive relative to early 2026 levels

- Gold’s rally was not driven by falling rates or rising inflation expectations

- Geopolitical risk and policy uncertainty boosted safe haven demand

- Downside appears limited, but upside momentum is likely to slow

Partial rebound, but valuations remain elevated

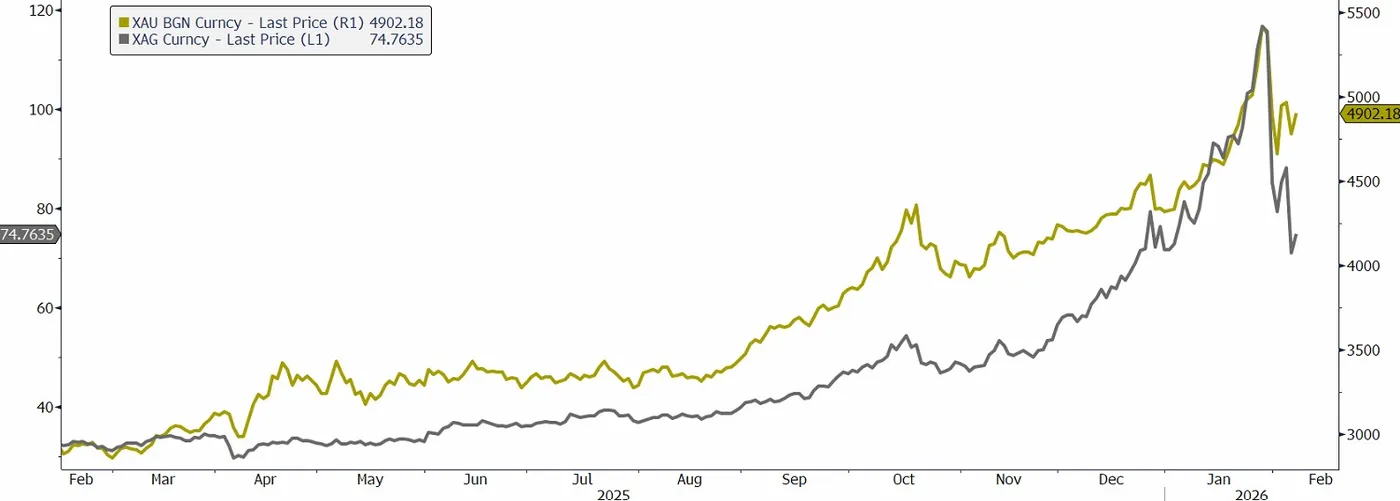

The precious metals market has seen a partial rebound after a sharp correction, but this has not fundamentally changed the picture of still elevated valuations. Gold remains more than 12 percent above its levels at the start of 2026, while silver is around 4 percent higher. In silver, the recent selloff pushed prices to new early February lows before only a modest rebound followed. The scale of the earlier rally keeps the question of how durable the correction really is firmly on the table.

Spot price chart for gold and silver, source: Bloomberg

A rally detached from classic macro drivers

What makes the current situation unusual is that the strong rise in gold prices was not supported by traditional macroeconomic factors. Real interest rates have not fallen materially, and long term inflation expectations in the United States remain stable, slightly below 2.5 percent. Markets are pricing in only two further rate cuts to around 3 percent by year end. At the same time, fundamental valuation models suggest that even after the recent pullback, gold is still priced roughly 2000 dollars per ounce above levels justified by macro fundamentals over the past three years, increasing vulnerability to further corrections.

Safe haven demand driven by global uncertainty

The main driver behind this overvaluation has been gold’s growing role as a safe haven. The war between Russia and Ukraine, tensions in the Middle East, and a more confrontational stance by China towards Taiwan have significantly raised global uncertainty. The freezing of Russian foreign exchange reserves has also heightened concerns among central banks about the safety of reserve assets. These factors were reinforced by the unpredictability of US economic policy under Donald Trump, including pressure on the Federal Reserve, aggressive trade policies, and rising fiscal risks, which undermined confidence in traditional safe assets.

Limited downside, but slower gains ahead

Recent price action shows that even a partial easing of uncertainty can halt rallies and trigger profit taking. Still, a sharp collapse in gold prices appears unlikely, as recent months have shown that declines are quickly used as buying opportunities, including by central banks. In the medium term, the most likely scenario is price stabilisation in gold and silver, followed by a moderate recovery, with higher volatility and clearly slower gains than at the start of the year.

{kind=link}