Dollar recovers mildly today but momentum stays weak. Philadelphia Fed president Patrick Harker said that he’s open to a March hike, but markets thought otherwise. Harker noted that he’s "supportive of three rate hikes" this year depending on how the economy and policies evolve. And, more importantly, "March should be considered as a potential for another 25 basis point increase". While he said the Fed is not behind the curve now, he wants to "make sure we don’t get behind the curve". Meanwhile, fed fund futures are pricing in just 8.9% chance of a March hike, down from prior day’s 13.3% and nearly 30% last month. Dollar index continues to hover tight range around 100 handle. Technically, as it’s close to key support level between 99.0/99.5. There is prospect of a short term rebound.

Euro Weakens as Draghi Tamed Tapering Speculations

Weakness in Euro is slightly helping the greenback to regain footing. ECB president Mario Draghi faced the European Parliament’s committee on economic affairs late yesterday. He noted that the central bank would not react to temporary spike in inflation. He emphasized that "our monetary policy strategy prescribes that we should not react to individual data points and short-lived increases in inflation". And, underlying inflation pressures "remain very subdued" reflecting "largely weak domestic cost pressures.

There were speculations that ECB could start tapering as headline inflation, recorded at 1.8% in January, would exceed 2% target soon. And Draghi’s comments tamed such speculations.

Meanwhile, Draghi also responded straightly to accusations by US president Donald Trump’s trade advisor to Germany regarding Euro. Draghi bluntly said that "first and foremost: we are not currency manipulators." And, "second, our monetary policies reflect the diverse state of the (economic) cycle of the euro zone and the United States."

Aussie Higher as RBA Maintained Neutral Stance

Aussie is generally firmer today after RBA stands pat and maintained a neutral stance. As widely anticipated, RBA left its cash rate unchanged at 1.50% at its first meeting in 2017. Policymakers acknowledged improvement in the global economic outlook. They also retained the view that the domestic economy would growth above-trend. The overall monetary stance is neutral, signaling the central bank is in no hurry to adjust the policy. The market is closely awaiting Governor Philip Lowe’s speech on Thursday and RBA’s Statement on Monetary Policy (SoMP) on Friday. The SoMP would reveal policymakers’ updated economic forecasts. We expect downgrades of both growth and inflation outlooks. More in RBA Sees Contraction In 3Q16 As Temporary, Maintains Neutral Stance

On the data front, UK BRC retail sales dropped -0.6% yoy in January. New Zealand RBNZ 2 year inflation expectation rose 1.9% in Q1. Japan leading index rose to 105.2 in December. German industrial production, Swiss foreign currency reserves will be released in European session. US will release trade balance. Canada will release trade balance, building permits and Ivey PMI.

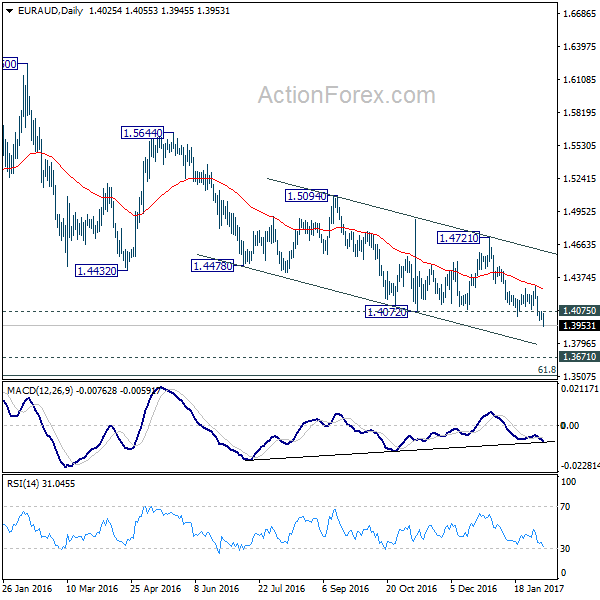

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.3996; (P) 1.4035; (R1) 1.4070; More…

EUR/AUD’s decline accelerates today and reaches as low as 1.3945 so far. Intraday bias remains on the downside for the moment. Current fall from 1.4721 is seen as part of the larger decline from 1.6587. Next target is key support level at 1.3671. As the fall from 1.6587 is seen as a corrective move, we’d expect downside to be contained by 1.3671 to bring reversal. On the upside, above 1.4075 minor resistance will turn intraday bias neutral first. Break of 1.4289 resistance will indicate short term bottoming and turn bias back to the upside for 1.4721 resistance.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a consolidative pattern. While further fall cannot be ruled out, we’d expect strong support above 1.3671 to contain downside and bring rebound. Up trend from 1.1602 should not be finished and will resume later. Break of 1.4721 resistance will indicate completion of such correction and outlook bullish for retesting 1.6587 high.

Economic Indicators Update

| MT | Ccy | Events | Actual | Consensus | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:01 | GBP | BRC Retail Sales Monitor Y/Y Jan | -0.60% | 0.90% | 1.00% | |

| 2:00 | NZD | RBNZ 2-Year Inflation Expectation Q1 | 1.90% | 1.70% | ||

| 3:30 | AUD | RBA Rate Decision | 1.50% | 1.50% | 1.50% | |

| 5:00 | JPY | Leading Index Dec P | 105.2 | 105.5 | 102.8 | |

| 6:45 | CHF | SECO Consumer Confidence Jan | -11 | -13 | ||

| 7:00 | EUR | German Industrial Production M/M Dec | 0.30% | 0.40% | ||

| 8:00 | CHF | Foreign Currency Reserves Jan | 646B | 645B | ||

| 13:30 | USD | Trade Balance Dec | -45.0B | -45.2B | ||

| 13:30 | CAD | International Merchandise Trade (CAD) Dec | 0.3B | 0.5B | ||

| 13:30 | CAD | Building Permits M/M Dec | -2.50% | -0.10% | ||

| 15:00 | CAD | Ivey PMI Jan | 58.3 | 60.8 |

Subscribe to our daily and mid-day newsletter to get this report delivered to your mail box

{kind=link}