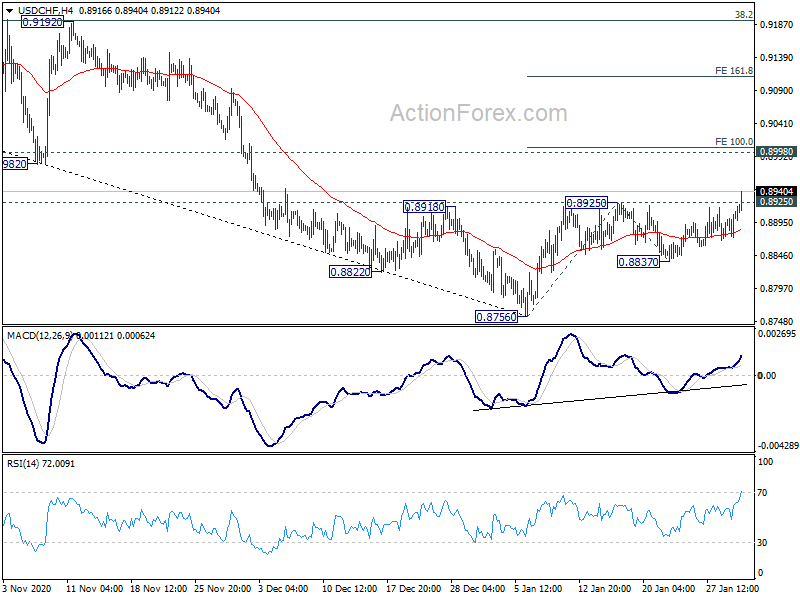

China Caixin PMI Manufacturing dropped to 51.5 in January, down from 53.0, missed expectation of 52.7. That’s also the lowest reading in seven months. Markit said that production and new orders both expanded at notably slower rates at the start of the year. There was fresh decline in new export business. Input costs and output prices both rose sharply.

Wang Zhe, Senior Economist at Caixin Insight Group said: “Overall, the manufacturing sector continued to recover in January, but the momentum of both supply and demand weakened, dragged by subdued overseas demand. The gauge for future output expectations was the lowest since May last year though it remained in positive territory, showing manufacturing entrepreneurs were still worried about the sustainability of the economic recovery. In addition, the weakening job market and the sharp increase in inflationary pressure should not be ignored.”

Full release here.

Released over the weekend, the official PMI manufacturing dropped to 51.3 in January, down from 51.9, below expectation of 51.5. PMP non-manufacturing dropped sharply to 52.4, down from 55.7, missed expectation of 55.1.

Fed Bostic: This recession was unlikely anything we had before

Atlanta Fed President Raphael Bostic said “this recession was unlike anything we ever had before, so the recovery is going to be that way as well”. As for the way out there in 2023, 2024, ” there’s a lot that’s going to happen that could go one way or another.”

“A lot of the recent developments have been positive,” he added. “We should be open to the possibility that things might happen more strongly than they would otherwise.”

Still, Bostic was not worrying about price pressures. “It’s not really the level of inflation but much more the trajectory as we move forward that I’m going to be focusing on to get answers of whether the economy might be moving into places that make me uncomfortable,” he said.