The Swiss National Bank is leaving the SNB policy rate unchanged at 1.75%. Banks’ sight deposits held at the SNB are remunerated at the SNB policy rate up to a certain threshold, and at 1.25% above this threshold. The SNB is also willing to be active in the foreign exchange market as necessary.

Inflationary pressure has decreased slightly over the past quarter. However, uncertainty remains high. The SNB will therefore continue to monitor the development of inflation closely, and will adjust its monetary policy if necessary to ensure inflation remains within the range consistent with price stability over the medium term.

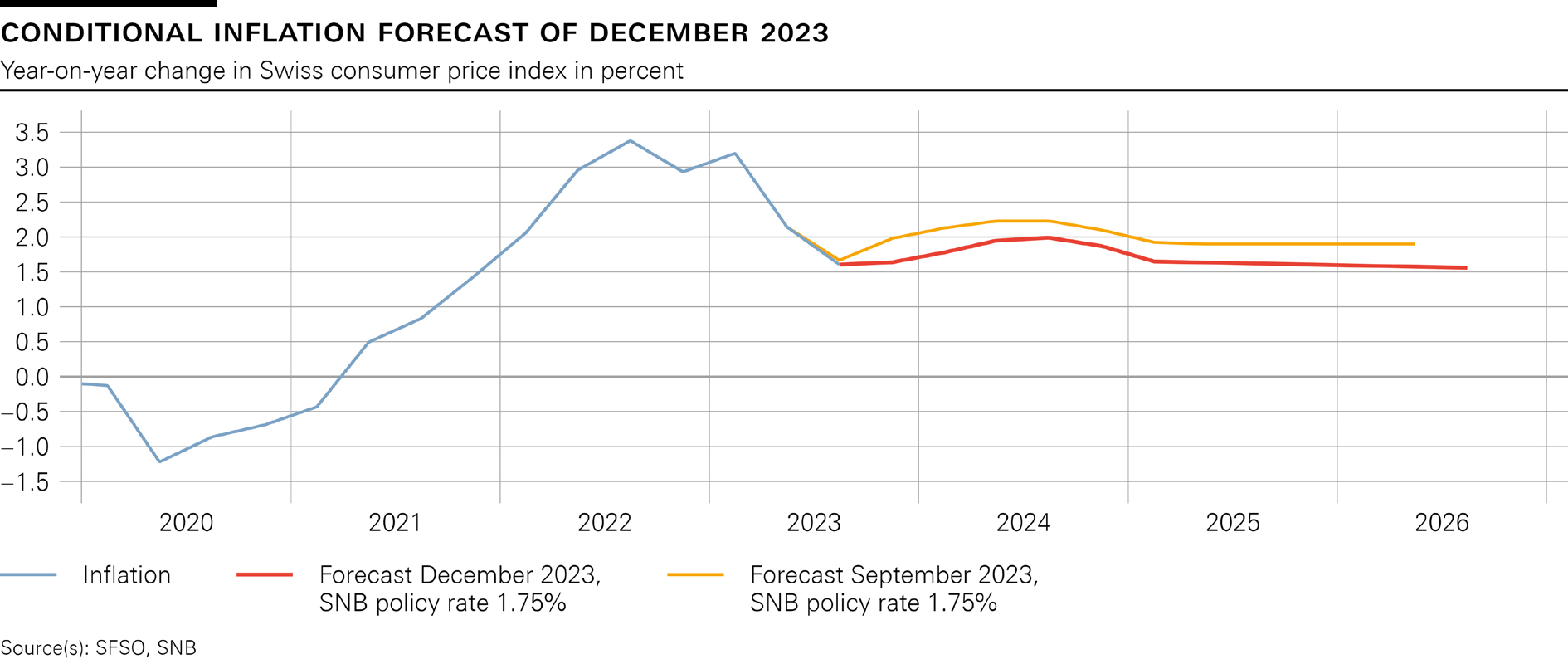

Inflation stood at 1.4% in November, and was thus somewhat lower than in the previous months. The slight decrease was above all attributable to lower inflation on goods and tourism services. However, inflation is likely to increase again somewhat in the coming months due to higher electricity prices and rents, as well as the rise in VAT.

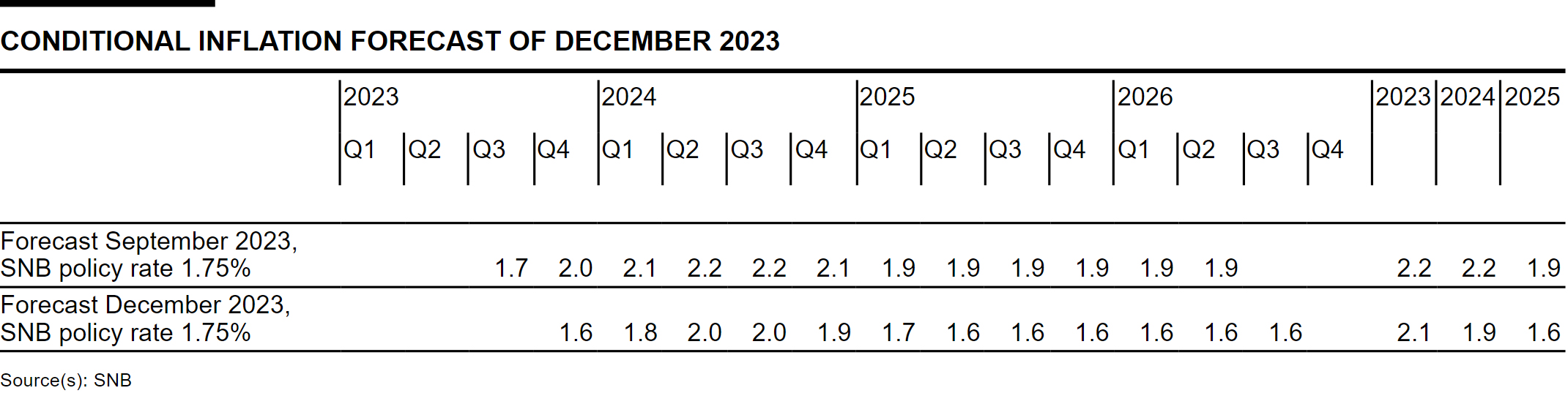

The new conditional inflation forecast is below that of September. In the short term, this is due to the recent lower-than-expected inflation. In the medium term, reduced inflationary pressure from abroad and somewhat weaker second-round effects are resulting in a downward revision. Over the entire forecast horizon, the inflation forecast is within the range of price stability (cf. chart). The forecast puts average annual inflation at 2.1% for 2023, 1.9% for 2024 and 1.6% for 2025 (cf. table). The forecast is based on the assumption that the SNB policy rate is 1.75% over the entire forecast horizon.

Global economic growth was stronger than expected in the third quarter of this year. Inflation has declined significantly in most countries in recent months. Against this backdrop, many central banks have refrained from further monetary policy tightening. With inflation still above the respective targets, monetary policy is likely to remain restrictive in many countries for the time being.

The growth outlook for the global economy in the coming quarters remains subdued. Inflationary pressure is likely to continue to ease.

This scenario for the global economy is still subject to large risks. Inflation could remain elevated for longer in some countries, necessitating a further tightening of monetary policy there. Equally, the energy situation in Europe could deteriorate over the course of the winter, and geopolitical tensions could increase. It therefore cannot be ruled out that global growth momentum will weaken more significantly than assumed.

Swiss GDP growth was moderate in the third quarter of this year. The services sector expanded again, while value added in manufacturing stagnated. Unemployment rose somewhat, and the utilisation of overall production capacity was only slightly above average.

Growth is likely to be weak in the coming quarters. Subdued demand from abroad and the tighter financing conditions are having a dampening effect. Overall, Switzerland’s GDP is likely to grow by around 1% this year. For 2024, the SNB currently expects growth of between 0.5% and 1%. In this environment, unemployment is likely to continue to rise gradually, and the utilisation of production capacity should decline somewhat further.

The forecast for Switzerland, as for the global economy, is subject to high uncertainty. The main risk is a more pronounced economic slowdown abroad.

Momentum on the mortgage and real estate markets has weakened noticeably in recent quarters. However, the vulnerabilities in these markets remain.

More detailed information on the monetary policy decision can be found in the introductory remarks of the Governing Board.

{kind=link}