Here are the latest developments in global markets:

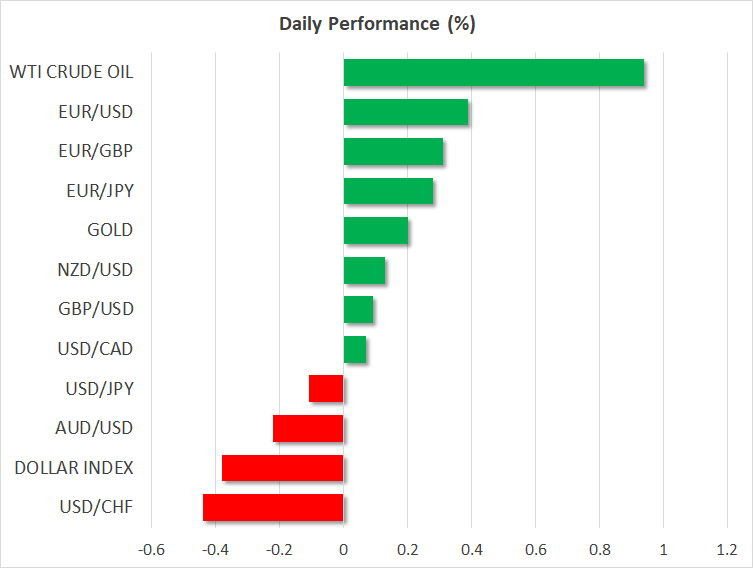

FOREX: The euro kept shining during the early European afternoon as yesterday’s comments by ECB officials raised speculation that the central bank was preparing to exit its quantitative program by the end of this year, with the announcement probably coming as soon as next week. Euro/dollar managed to peak at a fresh three-week high of 1.1837 before it fell to 1.1815 (+0.39%), being the best performer among its major peers. Against the yen, the euro posted moderate gains, edging up to 129.91 .(+0.15%), while versus the swiss franc it was down today at 1.1592 (-0.16%). Meanwhile in Italy, April’s retail sales recorded the sharpest decline since February, with the statistical office noting that economic growth could lose steam in coming months. Pound/dollar was the second-best performer of the day, winning 0.32%. Upbeat Halifax House prices helped the pair to reach a new two-week peak at 1.3471, though it soon returned to 1.3448. Euro/pound changed hands higher at 0.8788 (+0.13%). The dollar was on the back foot today at 109.92 (-0.22%), while the dollar index also stood lower at 93.32 (-0.36%) as investors turned more confident on the euro and pound amid tense trade relations between the US and the rest of the world. Dollar/loonie was steady at 1.2947. Aussie/dollar remained near today’s lows, fluctuating at 0.7655 (-0.20%) after trade stats out of Australia disappointed early today, showing a narrower trade surplus. Kiwi/dollar rose to 0.7047 (+0.23%). Dollar/Turkish lira moved up to 4.58 (+0.54%) ahead of a rate decision by the Turkish central bank. Recall that the Turkish President’s interest to monitor monetary policy after the June 24 presidential elections drove the pair to record highs recently.

STOCKS: After a respectful rally in Wall Street, European equities opened higher, with financials joining the biggest gains after ECB officials signaled that the central bank’s bond-buying program could come to an end by December this year. At 1100 GMT, the pan-European STOXX 600 was up by 0.15%, while the blue-chip Euro STOXX 50 was rising by 0.11%. The German DAX 30 gained 0.15%, the French CAC 40 climbed by 0.27% and the Italian FTSE MIB jumped by 0.31%. UK’s FTSE 100 inched up by 0.02% after a delayed open in the London Stock Exchange market due to technical issues, while the Spanish IBEX 35 was the best performer, surging by 0.79% towards two-week highs. In the US, futures tracking major stock indices were marginally higher, pointing to a slightly positive open.

COMMODITIES: Crude oil prices were rising on Thursday, supported by supply troubles in Venezuela. Particularly, the OPEC member is said now to be one month behind from serving customers from its export terminals as Trump’s sanctions imposed on the state-owned oil company PDVSA were said to disrupt the flow of activities. Increasing production in the US and worries that OPEC could raise its output at its two-day policy meeting on June 22-23 capped gains in the market. WTI crude and Brent were last seen at $65.35/barrel (+0.96%) and $76.34/barrel (+1.30%) respectively. In precious metals, gold was trading moderately higher around $1,298.70/ounce (+0.19%) on the back of a weaker dollar.’

Day Ahead: US jobless claims and Japan’s final GDP growth figures on today’s calendar

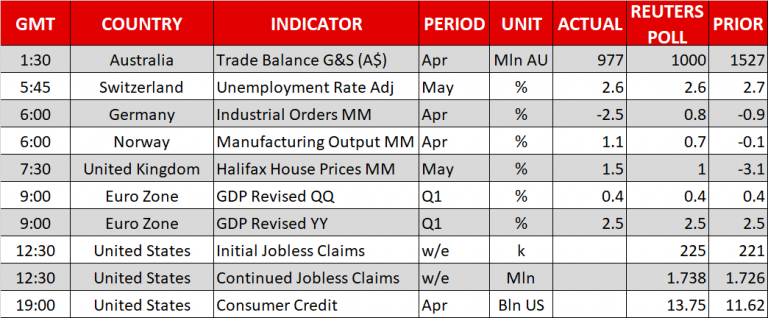

Looking at the calendar, out of the US, weekly jobless claims – initial and continued – due at 1230 GMT will be gathering attention. The Department of Labor forecasts 223,000 individuals to have applied for unemployment benefits in the week ending June 1, little changed from the preceding week’s 221,000. The world’s largest economy will also see the release of October consumer credit data at 1900 GMT.

Still, investors are turning their focus to the Group of Seven meeting later this week that may give clues on global trade tensions, as well as policy meetings from the European Central Bank and Federal Reserve next week. Today, sources stated that Germany and France joined voices to warn the US President of an inconclusive G7 meeting if progress in tariffs and the Iranian nuclear deal fails to be made.

Overnight, at 2350 GMT, the focus will also turn to Japan with the release of final GDP growth data. GDP growth is expected to fall by 0.4% on an annualized basis, less than the 0.6% decline estimated initially. On a quarterly basis, GDP growth is predicted to decline by 0.1% compared to a fall of 0.2% in the previous quarter.

The Bank of England’s Deputy Governor of Markets and Banking, Dave Ramsden is scheduled to speak in public today at 1600 GMT, while earlier at 1515 GMT, the Bank of Canada Governor Stephen Poloz and Senior Deputy Governor Carolyn Wilkins will be holding a press conference to discuss the contents of the Financial System Review

Meanwhile, the U.S. President Donald Trump will meet with Japanese Prime Minister Shinzo Abe at the White House ahead of next week’s US-North Korea summit in Singapore.

In Turkey, the central bank will decide on interest rates at 1100 GMT, while in the UK, British Ministers will meet in an effort to find common ground on the Irish border, an issue that continues to be a thorn in Brexit negotiations