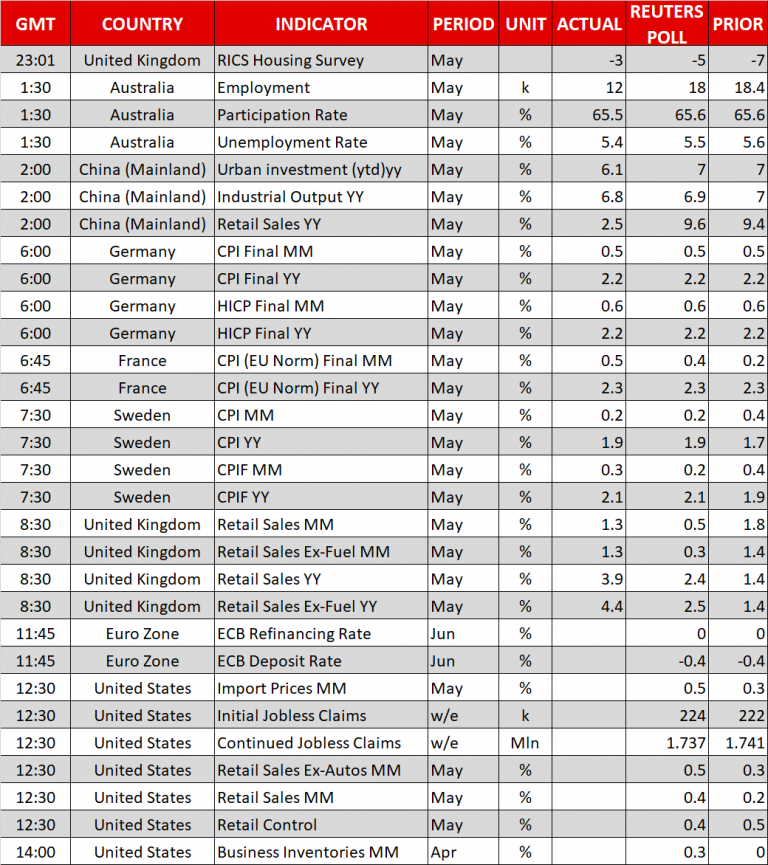

Here are the latest developments in global markets:

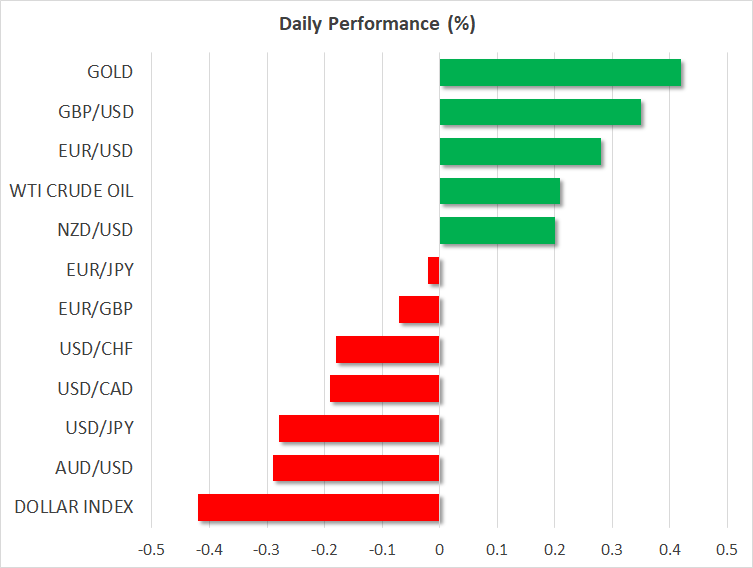

FOREX: The focus turns to the European Central Bank (ECB) interest rate decision and press conference a bit later on Thursday, with euro/dollar picking up by 0.31% before the meeting. The US dollar dived back from 3-week highs against the Japanese yen on Wednesday, erasing previous gains made after the Fed signaled two more rate hikes this year, bringing the total number of rises to four from the three previously thought. The FOMC raised the Fed funds rate by 25 bps to a range of 1.75%-2.00% as was widely expected. The pair, however, lost ground immediately after the FOMC announcement, with the sell-off continuing today to 109.96 (-0.33%) on the back of a stronger euro and pound as well as rising trade risks. Also, the US dollar index dipped by 0.44% to 93.30. Pound/dollar jumped considerably by 0.40% to a 5-day high of 1.3445 after UK retail sales climbed for a second consecutive month, on a monthly basis. The retail sales industry increased by 1.3% m/m in May versus 1.6% m/m in the preceding month, beating expectations, while year-on-year the index advanced by 3.9% from 1.4% before. Turning to the antipodean currencies, aussie/dollar slipped after job creation in Australia and industrial production in China fell short of expectations during the Asian session. The Australian unemployment rate, though, ticked surprisingly lower. The pair fell by 0.25% to 0.7556, while kiwi/dollar rose by 0.16% to 0.7034. Dollar/loonie slid by 0.19% to 1.2955.

STOCKS: Stocks retreated in global markets on Thursday. European equities were in a sea of red at 1030 GMT with the pan-European STOXX 600 and the blue-chip Euro STOXX 50 being down by 0.49% and 0.32% respectively. The German DAX 30 fell by 0.30%, the British FTSE 100 decreased by 0.57% to the lowest in more than two weeks, while the French CAC 40 dived by 0.24%. The Italian FTSE MIB declined by 0.40%. In the US, futures tracking stock indices were on the back foot as well, pointing to a negative open.

COMMODITIES: Oil prices were mixed today as investors waited for the OPEC policy meeting next week. West Texas Intermediate (WTI) crude gained 0.18% to $66.76 per barrel, while London-based Brent declined by 0.20% to $76.59 per barrel. In precious metals, gold was up by 0.45%, trading close to $1,305 per ounce level, printing the largest increase in more than a week. Sources so far support that OPEC members will increase oil output, a proposal made by Saudi Arabia and Russia. However, the meeting could take an interesting turn since Iran, Iraq, and Venezuela oppose the idea.

Day ahead: European Central Bank and Bank of Japan next to decide on interest rates

A policy meeting by the European Central Bank will take the center stage later on Thursday before a stream of data come out of the US, while trade and geopolitical headlines will remain in focus.

At 1145 GMT, ECB policymakers will conclude their two-day gathering, but no rate hikes are expected to be announced, with investors turning attention to the forward guidance in the rate statement and the press conference scheduled to start at 1230 GMT. Particularly investors will be eager to hear whether the ECB is ready to end its bond-buying program in December or whether it thinks is necessary to expand QE beyond the anticipated deadline. If the ECB chairman, Mario Draghi, flags the termination of the program by year-end then the euro could drift higher to fresh highs, though probably by not much as the news is almost priced into the markets. Otherwise, a more cautious tone, expressing the need to increase the duration of the QE, could pressure the common currency.

No change in interest rates is also widely expected in Japan early on Friday at a tentative time, where the Bank of Japan is anticipated to stand pat on its monetary strategy. In this case traders will take a look at the rate statement and the BoJ’s chief, Haruhiko Kuroda’s press conference to identify whether policymakers have changed their views on the country’s economic status after inflation, which is not even halfway of the BoJ’s target, continued its downtrend in May and GDP growth remained in negative territory in Q1 (second estimates). Specifically, it would be interesting to see what Kuroda has to say about the path of inflation after he decided to remove from the quarterly projections report the sentence referring to the timeline inflation could reach the BoJ’s target of 2.0%. Note that the central bank will not renew its economic forecasts at Friday’s meeting.

Meanwhile in the US, a number of economic releases are expected to keep investors busy at 1230 GMT. The Census Bureau is expected to show that US retail sales have marginally improved in May, posting a growth of 0.4% month-on-month compared to a rise of 0.2% in April. The expansion, however, is projected to be larger in the absence of the volatile automobiles, seen at 0.5% m/m versus 0.3% in the preceding month. Initial jobless claims for the week ending June 8 are forecasted to inch up as well, while May’s import prices are projected to support stronger inflationary pressures on a monthly basis.

In Beijing, the trade battle with the US is still open as Chinese officials wait for Washington to announce on Friday its final list of Chinese products subject to a 25% import tariff on $50 billion of goods.

The North Korean story will be under the spotlight as well. After the symbolic summit between the US President Donald Trump and the North Korean leader, Kim Jong Un spread hopes of peace between the two countries and the complete denuclearization of the North Korean peninsula, negotiating teams from both sides will continue talks to achieve these goals. Yesterday, the US Secretary of State, Mike Pompeo who met its South Korean and Japanese counterparts in Seoul said that the US will not abandon its sanctions against North Korea until it sees a complete denuclearization of the isolated region.