The Swiss National Bank (SNB) is widely expected to keep its ultra-loose policy unchanged when it announces its rate decision on Thursday at 0730 GMT. Investors will look for hints on whether a 2019 rate increase is a realistic scenario. While Swiss economic data are painting a rosier picture, it’s probably too early for such a signal, particularly with the franc already strengthening. In this respect, there is a clear downside risk for the currency, as policymakers may express discomfort with its recent appreciation.

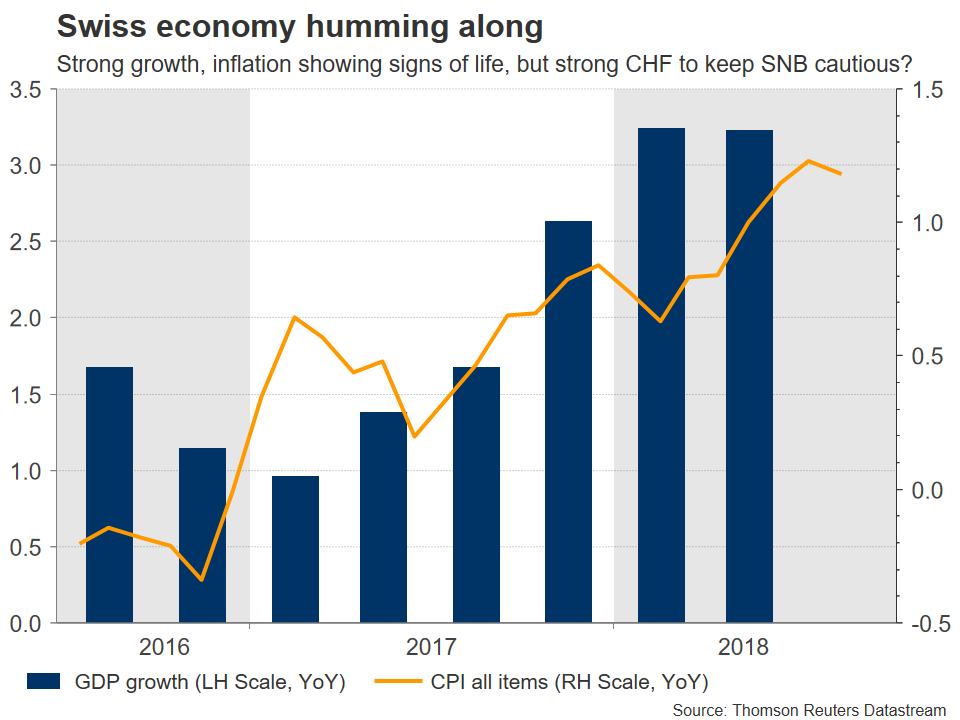

Switzerland’s economy has been recovering at a steady and healthy pace in recent quarters. Economic growth picked up speed in Q2, clocking in at an annual rate of 3.4%, an eight-year high. The unemployment rate continues to hover near a ten-year low and crucially, even inflation is showing signs of life again. The nation’s CPI rate currently rests at 1.2% in yearly terms, rising slowly yet consistently. To be fair though, most of this progress comes from higher energy prices, as core inflation – that excludes volatile items like food and energy – is much lower, at 0.5%.

Seen in isolation, these figures point to an overall strengthening outlook, and hardly justify the SNB holding interest rates at the lowest level worldwide. Yet, there is one factor that doesn’t fit in with this rosy picture; the exchange rate. As a reminder, the SNB pays very close attention to how strong the Swiss franc is. In general, an appreciating currency tends to hold down inflation by lowering the prices of imports, and since the franc typically benefits in times of global turmoil given its safe-haven status, the SNB has regularly intervened in the FX market to weaken the currency.

Seeing things through this scope, the franc’s substantial advance since May will likely be a worrisome development for policymakers. The safe-haven currency saw a surge of inflows amid intensifying concerns around international trade, Italy’s political situation, and emerging market fragility. Its surge threatens to derail, or at least delay, the SNB’s inflation-lifting efforts. Hence, a solid argument can be made that policymakers may opt to push back against this appreciation and “jawbone” the franc lower, perhaps by expressing increased concerns around its current levels and threatening to intervene if it continues to gain.

Beyond the franc, the other major area of focus will be any hints the SNB is gearing up to follow in the ECB’s footsteps, by indicating that a rate increase could come as early as 2019 amid an improving economy. That said, it still appears too early for such a signal, as suggesting as much could trigger a sharp rally in the Swiss franc that – as mentioned above – could hamper the upward trend in inflation. The SNB is unlikely to want to take such a risk with core inflation so low still, implying the path of least resistance may be sticking to the same language on policy, for now at least.

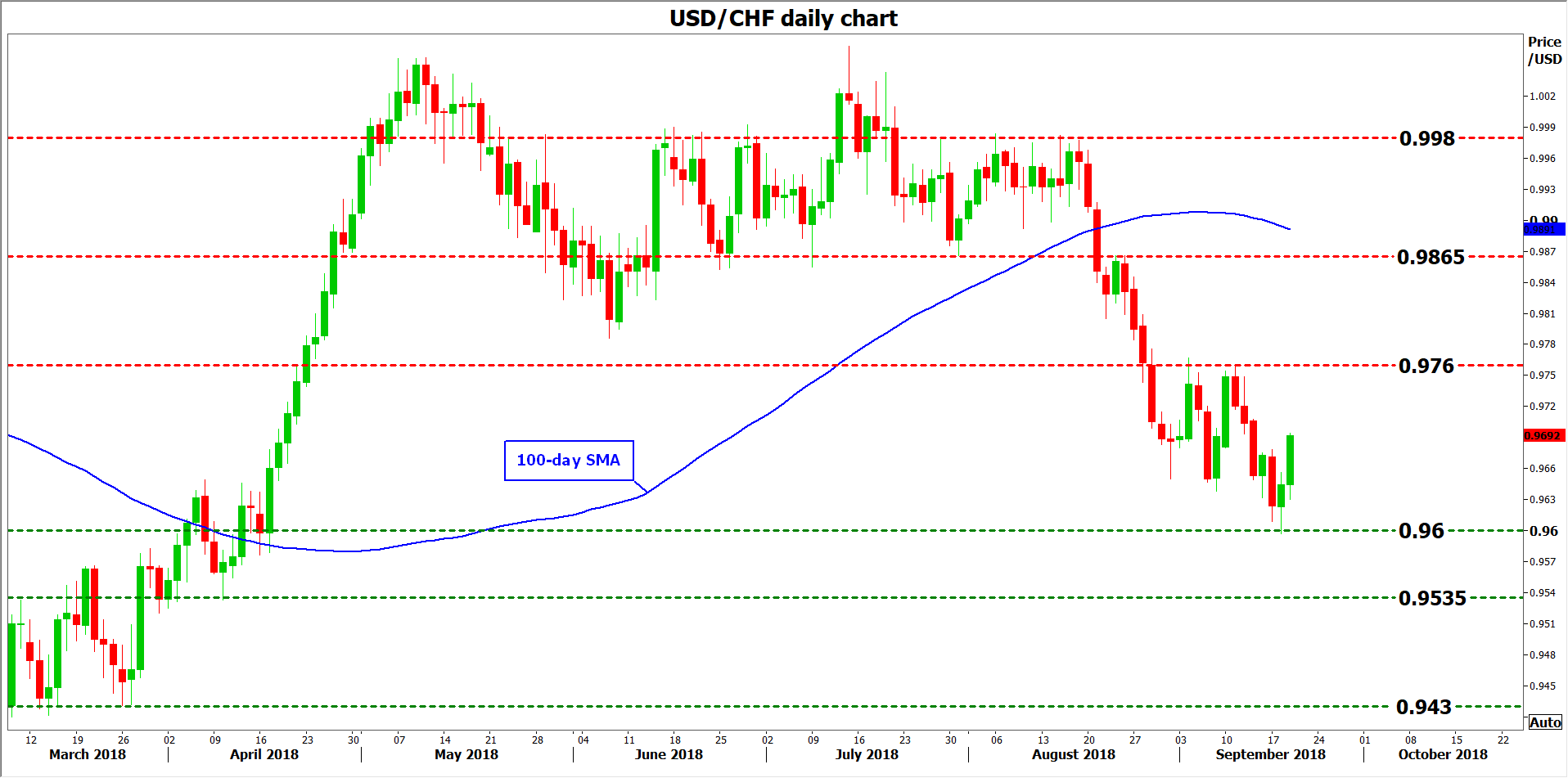

In case the Bank indeed shows no signs it is considering normalization, or if officials strike a more worried tone around the franc’s appreciation, the currency could tumble. Looking at dollar/franc, resistance to advances may come near 0.9760, the high of September 11, before the 0.9865 hurdle comes into view – this being the peak of August 23. Even higher, the August 17 top of 0.9980 would increasingly come into view.

On the contrary, any hints from the SNB that a rate hike is possible in 2019 could trigger another round of gains in the franc. In such case, dollar/franc could edge lower for a test of 0.9600, the low of September 18. A downside break could shift the attention to the April 10 trough of 0.9535, ahead of the March 26 low, at 0.9430.

Looking past the SNB, the franc will also remain sensitive to any developments in trade tensions, emerging markets, and the situation in Italy. Should these risks grow further, that would likely drive more flows into the haven currency, and vice-versa.

{kind=link}