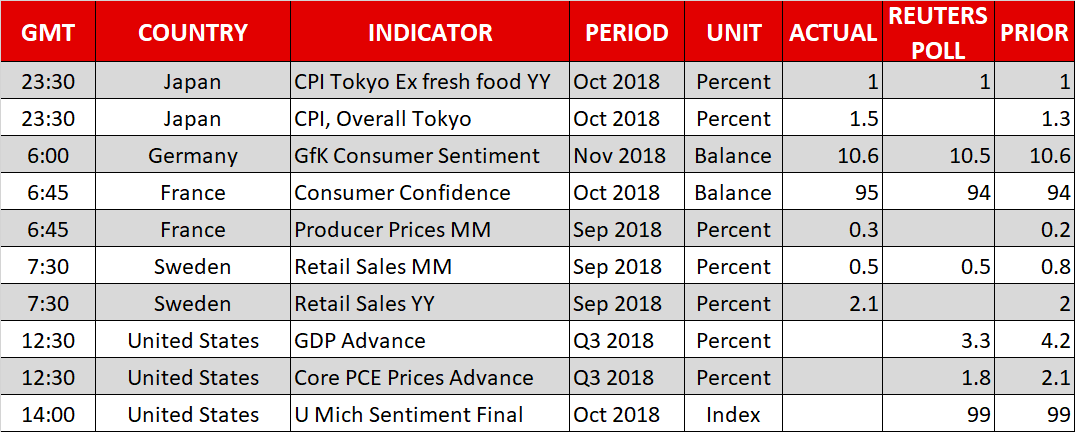

Here are the latest developments in global markets:

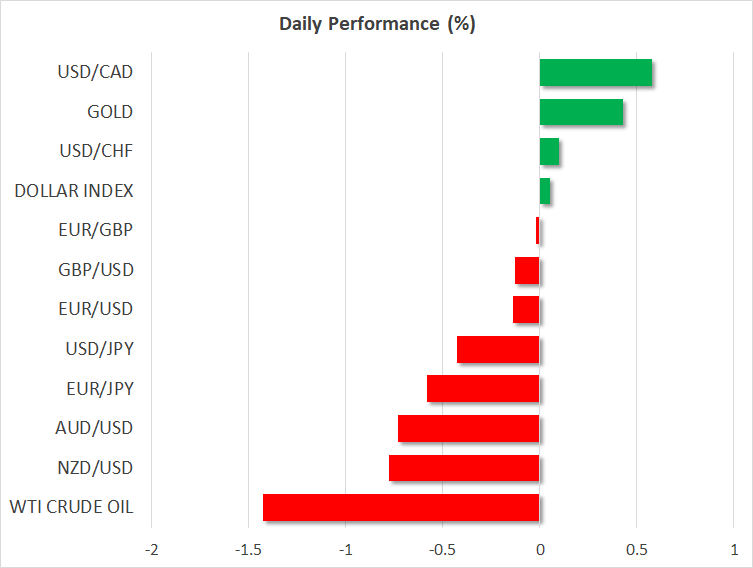

FOREX: The Japanese yen is by far the best performer among the major currencies on Friday, with the session being characterized by broad-based risk aversion thus far. Dollar/yen (-0.40%) is trading just a few pips below the 112.00 handle, while euro/yen (-0.61%) touched a fresh two-month low, as investors sought the safety of the Japanese currency. The dollar is also on the front foot ahead of the release of US GDP data, albeit only modestly. Euro/dollar is down by 0.12%, with the euro still licking its wounds following the ECB meeting yesterday. Sterling/dollar is lower by 0.12% as well, extending losses from Thursday that came on the back of reports Theresa May’s Cabinet cannot agree on a way forward for the Brexit talks to resume. Elsewhere, the commodity-currencies space was feeling the heat of the broader “risk-off” environment. Aussie/dollar (-0.69%) posted a new 2½ year low of 0.7020, while kiwi/dollar (-0.74%) is hovering just above its own multi-year trough. Meanwhile, dollar/loonie climbed by 0.60%, with the Canadian currency surrendering all the gains it recorded after the BoC struck a hawkish tone earlier in the week, to trade much lower.

STOCKS: European stocks were a sea of red at 1100 GMT on Friday, with the pan-European STOXX 600 trading lower by 1.44%, and the blue-chip STOXX 50 down by 1.40%. Accordingly, the German DAX 30 (-1.81%), French CAC 40 (-2.27%), British FTSE 100 (-1.56%) and Italian FTSE MIB (-1.67%) were all on the back foot. In the US, futures tracking the S&P 500, Dow Jones, and Nasdaq 100 were pointing to a significantly lower open today for these indices, greater than -1.0%.

COMMODITIES: Oil prices followed risk sentiment and energy stocks lower, with WTI (-1.46%) trading at $66.35 per barrel, and Brent (-1.25%) changing hands at $75.93 a barrel. Besides poor risk appetite, a warning by Saudi Arabia yesterday that oil markets could be oversupplied by the end of the year may have also contributed to the tumble. In precious metals, gold was higher by 0.46% at $1236 per ounce, enjoying some haven-demand as investors were increasingly turning defensive.

Day ahead: US GDP data in the limelight as risk sentiment remains fragile

Preliminary US GDP figures for Q3 will be the highlight during the remainder of Friday’s session in terms of data releases. Beyond those, currencies will remain sensitive to stock market movements and how risk sentiment develops, in light of the recent volatility.

Kicking off with the data, the first estimate of US GDP for Q3 is due out at 1230 GMT, and expectations are for economic growth to clock in at an annualized pace of 3.3%. While this would mark a slowdown from the robust 4.2% recorded in Q2, it’s still a very healthy print overall, with the Trump administration’s tax cuts seemingly keeping growth above potential. For context, the Atlanta Fed GDPNow model estimates the GDP print at 3.9%, while the New York Fed’s own gauge places it at a mere 2.1%.

Alongside the GDP number, the US will also release the preliminary core PCE price index for Q3. Forecasts point to inflationary pressures having lost some steam, with the core PCE rate expected to cool to 1.8% in annualized terms, from 2.1% in the previous quarter. The dollar will likely take its cue from these prints, coming under renewed buying interest in case of an overall beat, or giving back some of its latest gains on a disappointment. The final University of Michigan consumer sentiment index for October is also due out, at 1400 GMT.

More broadly, the mood in equity markets will likely prove critical in setting the tempo for currencies as well. Following disappointing earnings reports from the likes of Amazon and Google parent Alphabet after Wall Street’s closing bell yesterday, futures tracking the major US indices are flashing red, pointing to a notably lower open today. This has spilled over into broader risk aversion, evident by the defensive yen advancing across the board today, and commodity-linked currencies such as the aussie, kiwi, and loonie all recording sizeable losses.

In euro-related news, Standards and Poor’s is anticipated to announce its decision on Italy’s sovereign credit rating today. A potential downgrade of the nation’s debt, against the backdrop of Italian politicians remaining adamant about their elevated budget deficits, could spell more bad news for Italian assets and by extent, for the single currency.

As for the speakers, ECB President Mario Draghi will deliver remarks at 1400 GMT, but bearing in mind investors already heard from him at yesterday’s ECB meeting, any fresh signals that trigger a reaction in the euro appear unlikely.