Here are the latest developments in global markets:

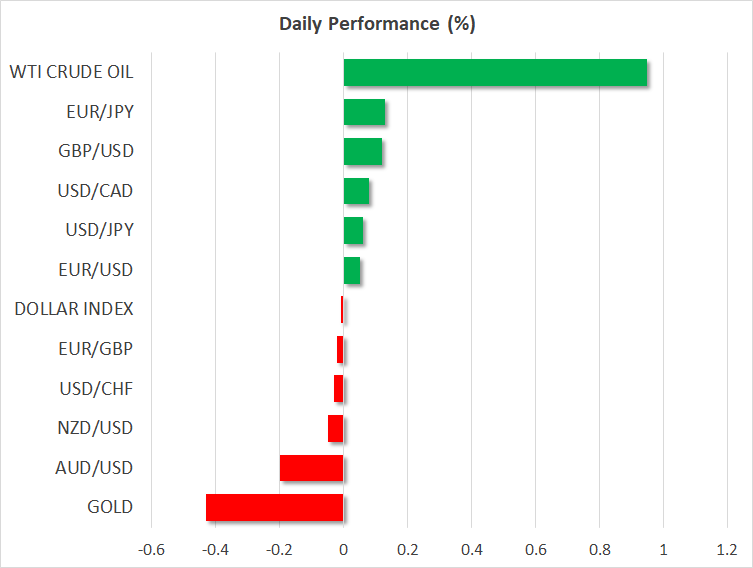

FOREX: The dollar soared to a fresh high last seen in June 2017 against a basket of six major currencies, as risk sentiment was reinvigorated. The pound was the worst performer, as ratings agency S&P warned of a recession in case of a no-deal Brexit. The defensive yen was the second-worst performer in the face of stronger risk appetite. Meanwhile, the aussie is on the back foot on Wednesday, giving back some of its gains from the previous session, amid disappointing inflation data out of Australia and PMIs from China.

STOCKS: US markets came roaring back on Tuesday, without any clear trigger behind the bounce, and curiously overlooking a simultaneous rebound in US bond yields. The Dow Jones was the best performer (+1.77%), while the benchmark S&P 500 (+1.57%) and the tech-heavy Nasdaq Composite (+1.58%) followed in its tracks. Moreover, the optimism seems to have lingered, as futures tracking the Dow, S&P, and Nasdaq 100 are all pointing to a higher open today as well. Correspondingly, Asia was a sea of green on Wednesday. Japan’s Nikkei 225 and Topix rose by 2.16% and 2.15% respectively, while the Hang Seng in Hong Kong gained 1.35%. In Europe, all the major indices were looking set to open notably higher according to futures markets.

COMMODITIES: Oil prices were on the rise on Wednesday, recovering some of the losses from the previous two sessions. On the one hand, the demand picture looks bleak, as global growth is wobbly and crude demand could be one of the first casualties if the US-China trade conflict escalates further. On the other, the looming sanctions on Iran coupled with reports that OPEC and allies are considering productions cuts, likely kept a floor under prices. In precious metals, gold is down by more than 0.4% today at $1,215 an ounce, feeling the heat of a stronger dollar and the improvement in risk sentiment. A dip back below $1,214 would turn the short-term technical picture back to neutral.

Major movers: US equity markets roar back; dollar soars to fresh 1½-year high

The overarching theme during Tuesday’s trading session was a revival of risk appetite, though once again, in the absence of any fresh catalyst – other than an upbeat reading on US consumer confidence. US stock markets came roaring back, with commodity currencies such as the aussie and kiwi also advancing. Accordingly, the defensive Japanese yen was the second-worse performer among the major currencies, after sterling, weighed down by a lack of haven demand.

Meanwhile, the dollar index soared to a fresh 1½-year high, with the US currency drawing strength from an uptick in longer-dated US Treasury yields. The move highlights that the greenback has the best of all possible worlds at the moment. Namely, it can act both as a haven asset when risk sentiment deteriorates given its status as the world’s reserve currency, and also outperform in a risk-on environment given its high-carry appeal.

In the UK, the pound surrendered ground as Brexit uncertainties continued to ride high. Credit ratings agency S&P issued a stark warning that the probability for a no-deal Brexit has risen, and that such an outcome would likely trigger a recession, and alongside it a rating downgrade. This probably served as a reminder that the talks remain in a deadlock, with any deal now unlikely to be reached before December, if at all. Such a timeframe would also allow little time to push any deal through Parliament, which itself isn’t going to be a picnic for PM May.

In the eurozone, GDP growth for Q3 disappointed, clocking in at a mere 0.2% in quarterly terms, from 0.4% previously. The print underscores that the slowdown seen in PMI surveys is manifesting into the “hard data” too, and that the ECB may have an increasingly difficult task of unwinding its stimulus while staring down the barrel of a slowing economy. Euro/dollar fell below 1.1350.

Overnight, the BoJ kept its policy unchanged, downgrading its inflation forecasts. Other than that, there were practically no fresh signals on policy, and the reaction in the yen was accordingly non-existent. All in all, with underlying inflation still so far away from target, the BoJ appears unlikely to alter its ultra-loose policy framework anytime soon. In isolation, this argues for a weaker yen over time, particularly against currencies of nations that are raising rates – like the dollar – as the yield differential between Japan and other economies widens.

Day ahead: Eurozone flash inflation, US ADP jobs data and Canadian growth figures coming up

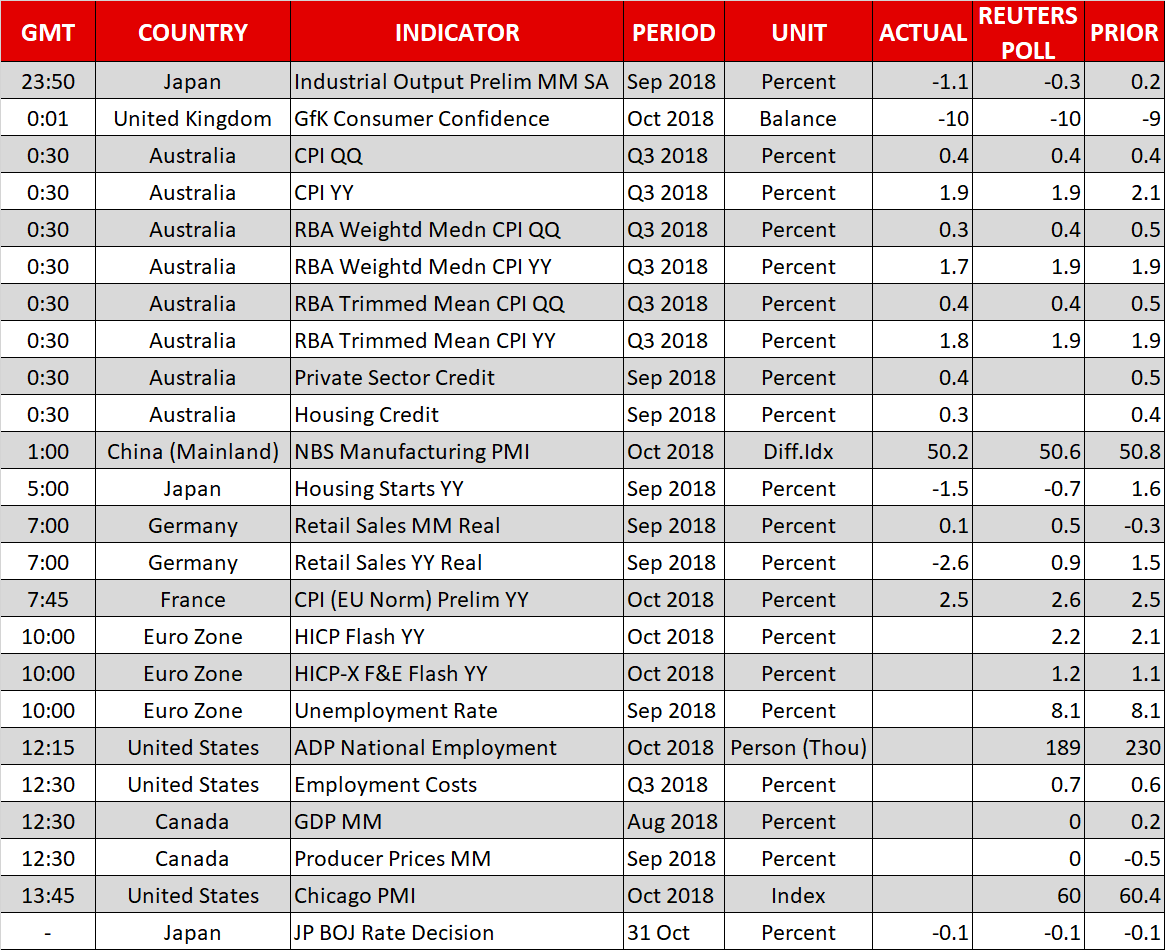

Eurozone inflation figures, the ADP employment report out of the US, and monthly GDP numbers out of Canada are some of the highlights on Wednesday’s economic calendar.

The prints for eurozone flash inflation for October will be released at 1000 GMT. The harmonised index of consumer prices (HICP) is anticipated to have grown by 2.2% y/y in October, above September’s 2.1% and matching its highest since December 2012. For perspective, the ECB’s target for annual inflation is “close to but below 2%”. Still, the significance of the overshoot in headline inflation might be downplayed, as underlying price pressures remain relatively subdued. In this respect, core HICP that excludes volatile food and energy items is projected to grow by 1.2% y/y, up from September’s 1.1%. A notable beat in the numbers may see the battered euro – EURUSD is trading around two-and-a-half-month lows – post a relief rally.

Also out of the euro area at 1000 GMT will be September’s unemployment rate. That’s expected to match August’s 8.1% rate, which is the lowest since late 2008.

Out of the US, October’s ADP national employment report on the number of positions added to the economy by the private sector is due at 1215 GMT. The number of jobs added is forecast to stand at 189k, down from 230k during September, though still constituting a relatively robust figure. Traders may use the ADP data to speculate on how Friday’s nonfarm payrolls report will come out, though it bears mention that the two prints are far from perfectly correlated. Elsewhere, Q3 employment costs are also due out of the US at 1230 GMT; this is a gauge of wage growth and thus is worth keeping an eye on. Lastly, October’s Chicago PMI is slated for release at 1345 GMT.

The reading on Canada’s August GDP growth will be made public at 1230 GMT. Zero growth is forecast by analysts during the month, after economic activity expanded by 0.2% m/m in July. September’s producer prices out of the nation will be hitting the markets at the same time.

Meanwhile, global trade – the Sino-US dispute –, Italian and German politics, as well as Brexit uncertainty remain in the background, with any headlines having the potential to rattle the markets. Relating to the latter, UK PM May and finance minister Hammond will be meeting chief executives and international investors to discuss Brexit and the nation’s latest budget.

ECB members Nowotny and Nouy will be speaking at 0900 GMT and 0905 GMT correspondingly, while the Bank of Canada Governor Poloz and Senior Deputy Governor Wilkins will be appearing before a Senate Committee at 2015 GMT.

In equities, General Motors will be reporting quarterly earnings before the US market open.

In energy markets, EIA data on US crude stocks due at 1430 GMT are predicted to show an inventory buildup of around 4.1 million barrels during the week ending October 26, following a rise by roughly 6.3m in the previously tracked week

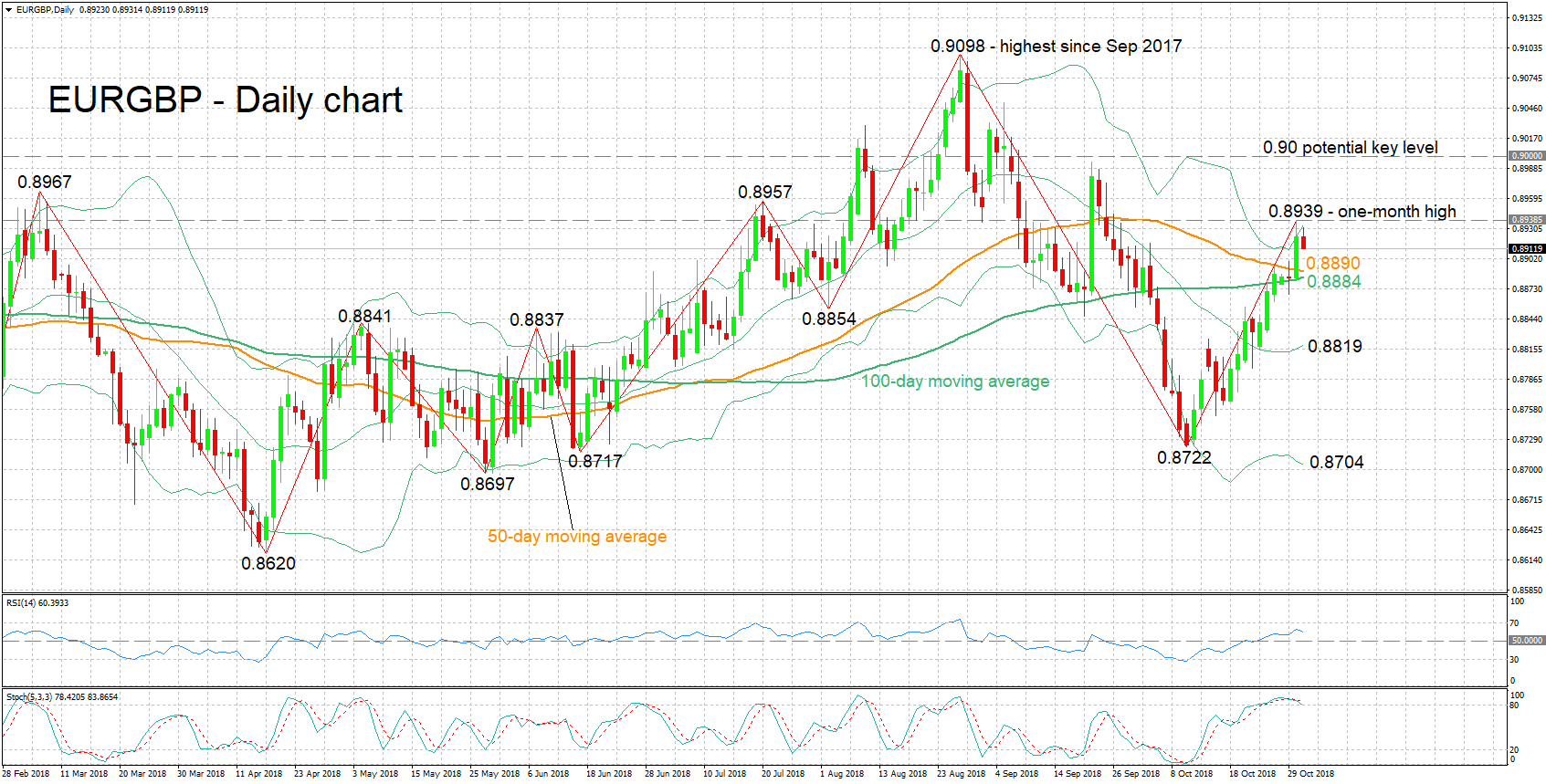

Technical Analysis: EURGBP bullish bias though stochastics signal caution in very short-term

EURGBP has staged a recovery after hitting its lowest since mid-June of 0.8722 on October 10. On Tuesday it touched a one-month high of 0.8939, while it is currently trading not far below that peak. The RSI, which is in bullish territory and has been rising in recent weeks, is projecting a bullish short-term picture. The stochastics though are signaling that losses may be in store in the very short-term; the %K and %D lines have recorded a bearish cross.

Stronger-than-anticipated inflation figures out of the eurozone are likely to push the pair higher. Immediate resistance could take place around yesterday’s high of 0.8939; the area around this captures a couple of tops from previous months at 0.8957 and 0.8967, as well as the upper Bollinger band at 0.8933. Further above, the 0.90 handle may act as a psychological barrier, while higher still, the attention would turn to late August’s high of 0.9098.

On the downside and in the event of disappointing data out of the euro area, support may come around the current levels of the 50- and 100-day moving average lines at 0.8890 and 0.8884 respectively; the zone around these includes numerous tops and bottoms from the past. Steeper losses would shift the focus to the middle Bollinger line at 0.8819 – a 20-day MA line –, while further below the 0.8722 bottom would increasingly come into scope.

Brexit headlines can also move the pair.