Wednesday June 14: Five things the market is talking about

Soft U.S inflation data is raising market uncertainty about the Fed’s policy plans for the rest of the year. Will Fed Chair Janet Yellen clarify their outlook this afternoon?

The Fed is widely expected to agree on an interest-rate increase today (2:00pm EDT) at the conclusion of its two-day meeting. U.S policy makers will probably also acknowledge recent inflation declines, while sticking to previous guidance for another hike before year-end and a first step towards unwinding its +$4.5T balance sheet.

Note: Fed officials have said for months they were discussing how to reduce the balance sheet, and last month outlined a proposed approach that would let increasing amounts of securities mature over time.

Any ‘dot plot’ downshift would definitely cast doubt on the Fed hiking three times in 2017.

Ahead of the U.S open, the ‘mighty’ dollar has weakened for a third consecutive day, Treasury prices have edged a tad higher and global equity markets are mixed.

Note: Bank of Japan (BoJ), Swiss National Bank (SNB) and Bank of England (BoE) are also scheduled to weigh in with policy decisions this week.

1. Global equities mixed performance

In Japan, stocks ended marginally lower in choppy trade overnight, as investors abstained from taking positions ahead of the Fed’s rate announcement. The Nikkei share average fell -0.1%, while the broader Topix Index also closed down -0.1%.

Down-under, Australia’s S&P/ASX 200 Index climbed +1.1% to its highest print since mid-May.

In China, the Shanghai Composite Index tumbled -0.8% and the CSI 300 Index dropped -1.3%, its biggest loss this year.

In Hong Kong, the Hang Seng Index pared losses, up +0.1%, while in South Korea the Kospi Index fell -0.1%.

In Europe, indices trade modestly higher following on from yesterday’s rebound stateside. The French CAC is the out performer, whilst the FTSE MIB (Italy) again lags.

U.S stocks are expected to open little changed.

Indices: Stoxx50 +0.6% at 3578, FTSE +0.3% at 7527, DAX +0.4% at 12820, CAC-40 +0.9% at 5306, IBEX-35 +0.1% at 10896, FTSE MIB +0.1% at 21107, SMI +0.3% at 8897, S&P 500 Futures flat

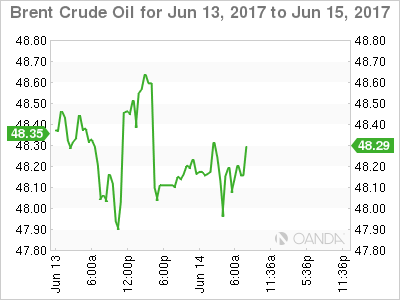

2. Oil prices fall as OPEC output, U.S crude stockpiles rise, gold unchanged

Ahead of the U.S open, oil prices are under pressure after industry data yesterday revealed a build in U.S crude stocks and OPEC reported a rise in its production despite a pledge to cut output.

Brent crude oil is down -45c a barrel at +$48.27, while U.S light crude (WTI) is -50c lower at +$45.96.

Note: Crude prices have fallen more than -10% since late May, pulled down by heavy global oversupply that has persisted despite a move led by OPEC to curb production.

Oil stocks are near record highs in some parts of the world, and producers that are not part of the OPEC deal are increasing output.

API data yesterday showed that U.S crude stocks rose by +2.8m barrels in the week to June 9 to +511.4m, compared with expectations for a decrease of -2.7m barrels.

According to BP data yesterday, global energy demand grew by +1% in 2016, a rate similar to the previous two years, but well below the 10-year average of +1.8%.

The market will take its cues from today EIA report at 10:30 am EDT.

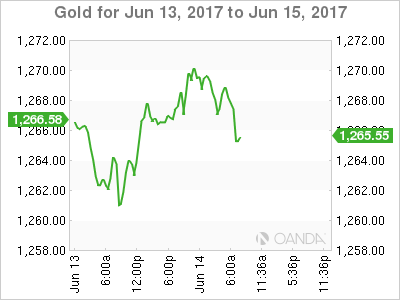

Spot gold is little changed ahead of the Fed rate announcement (+0.1% at +$1,267.05 per ounce). Yesterday, the yellow metal touched its weakest price since June 2 at +$1,259.16.

3. Yields require Fed guidance

U.S equities continue to climb, yields have fallen (U.S 10’s at +2.21%) and volatility remains low, despite recent Fed rate increases and plans for more.

Note: A Fed board whitepaper estimated that the expansion of Fed bond holdings since the crisis likely lowered the yield on the benchmark 10’s by a percentage point from where it would otherwise have been. By 2023, the paper said, the yield would still be about -25 bps lower despite an anticipated shrinkage in the balance sheet.

The Fed’s portfolio of assets has grown to +$4.5T from around +$800B before the crisis through a series of bond-buying programs aimed at lowering long-term interest rates. Allowing these assets to roll off is expected to push up long-term rates.

Market volatility has been well contained thus far, but is expected to pick up when fixed income dealers knows when the Fed will begin the process of reducing its balance sheet, the pace and the likely size of the balance sheet at the end.

Elsewhere, U.K, Germany and French benchmark yields all rose +1 bps, while the Aussie benchmark yield is little changed at +2.40%.

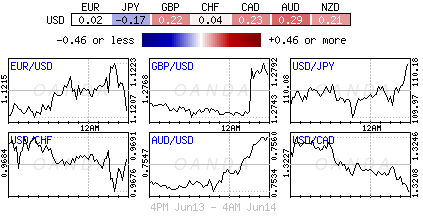

4. Dollar small under pressure

It comes as no surprise that the FX market is relatively steady ahead of the expected interest rate hike by the Fed.

The dollars next step will depend on what clues Ms. Yellen will serve up regarding the Feds policy for the rest of this year.

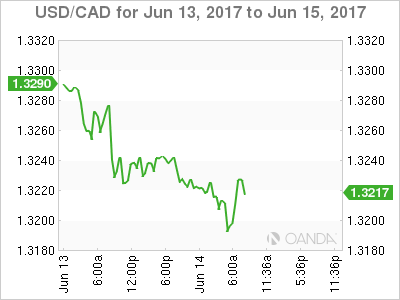

USD/CAD (C$1.3198) continues to trend lower, trading atop of its two-month lows following ‘hawkish’ comments from Bank of Canada’s Deputy Governor Carolyn Wilkins Monday and Governor Poloz yesterday pointing out that the central bank may consider curtailing its accommodative monetary policy in view of the broadening economic growth.

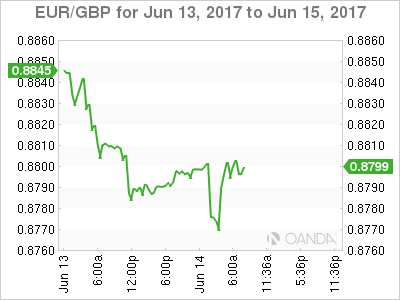

GBP (£1.2745) is off its overnight highs, but is supported now that PM May seems to have secured the support of the DUP to form a working government. U.K wage data (see below) registered a lower reading for the second consecutive month hindered some of the pounds progress. Sterling ‘bulls’ believes that last week’s snap election results have reduced the odds for a "hard" Brexit actually occurring is also supporting the pound. The Bank of England (BoE) rate announcement is due Thursday, no change is expected.

5. UK Real Wages Fall Again, China sales improve

Data this morning showed that the U.K. unemployment rate held steady in the three months to April, but regular wages adjusted for inflation fell on the year for the second consecutive month, suggesting accelerating inflation is squeezing British shoppers’ wallets.

The unemployment rate stood at +4.6% – the lowest rate since mid-1975 – but real wages fell by -0.6% compared to the same period last year. Inflation stood at +2.9% in May, the fastest pace of price growth in nearly four-years.

In China, retail sales rose +10.7% y/y in May, in line with consensus, while industrial production was up +6.5% vs. an expected +6.4% gain.