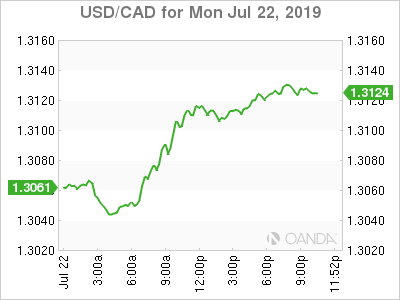

The Canadian dollar fell against the US dollar on Monday. The USD/CAD traded at 1.3122 at the end of the session Canadian wholesale sales surprised to the downside with a -1.8 percent drop, when the forecast called for a 0.8 percent gain. The loonie has risen 3.78 percent year to date against the dollar as the Fed’s 180 degree turn has put pressure on the American currency while the Bank of Canada (BoC) waits patiently on the side lines.

Disappointing data like the today’s wholesale numbers will affect the probabilities of a lower interest rates in Canada. The divergence between the US and Canadian central banks could end up being lower if trade disputes continue at a massive scale, forcing the BoC to lower rates to avoid a recession.

Oil surged, but offered little support to the loonie at the start of the week. With the Wholesale sales data out of the way for this week’s economic calendar, the Canadian currency will be trading on external data with the US PMI, durable goods and advance GDP the most likely to move the needle. The ECB will set the tone this week on how dovish can you go, without actually cutting rates as the market awaits the July FOMC meeting for the first rate cut of the new easing monetary policy cycle.

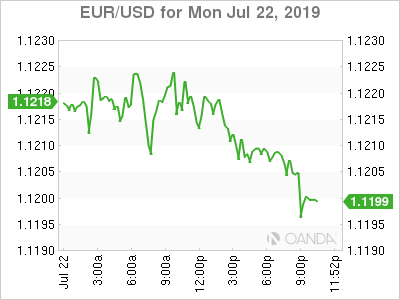

The US dollar is lower across the board on Monday. The greenback will be on the back foot until the second day of the July Federal Open Market Committee (FOMC) meeting. The central bank is expected to cut rates by 25 basis points, but a deeper cut would put more downward pressure for the currency. The EUR managed to gain on the USD, despite the European Central Bank (ECB) publishing its rate statement this week and the anticipation of more dovish rhetoric or almost a 50 percent chance of lowering the deposit rate deeper into negative territory.

ECB President Mario Draghi will finish his mandate this October, with former IMF leader Christine Lagarde his appointed successor. The leadership change brings up timing issues as the central bank will ease more to stave off recession and spark growth but could wait until the new head is in charge.

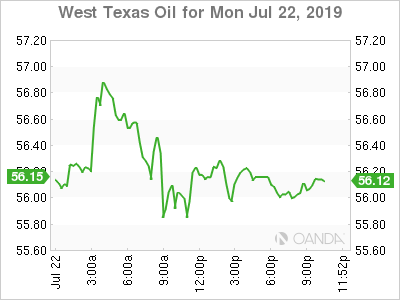

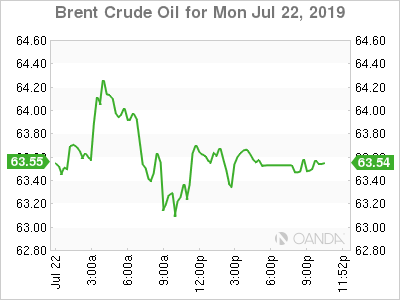

OIL

Oil prices rose on Monday as the Middle East tensions once again resurfaced. WTI and Brent gained on the back of Iran seizing a British oil tanker last week. Ample supply is keeping the rise to a moderate level even after taking the importance of the Strait of Hormuz into consideration.

Lower global demand estimates from OPEC, IEA and EIA have hit crude prices in the last couple of weeks. Weather and geopolitical disruptions have been temporary and only the OPEC+ deal has given traders clarity with the group’s commitment to reducing the oil glut at their expense.

The US pulled out of the Iran nuclear deal and has put economic sanctions in place and has begun to ask other nations to pitch in to protect shipments. The seizure of the UK ship comes at an unfortunate time given the lack of leadership as Theresa May steps down.

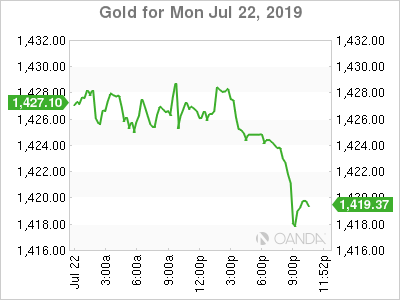

GOLD

Gold trading was choppy at the start of the week. The yellow metal almost ended up where it started and did not trade outside a tight 5 dollar range. There was little data to guide investors with most of the market awaiting PMI data in Europe and the US due Wednesday and the ECB policy statement on Thursday.

Geopolitical uncertainty has kept gold bid as the dollar is under pressure from the upcoming US interest rate cut that has been telegraphed by the Fed. The market has priced in a 25 basis points cut, but a 50 basis points slash is still possible even though Fed members have talked down the probability of a deep cut in July.

Middle East tensions as Iran and the US exchanged comments continue to rise as Iranian forces captured a British tanker. Gold had lost some momentum as a more diplomatic outcome was discussed by Iranian and American leadership, but now military action is back on the table giving a boost to the yellow metal as a safe haven.

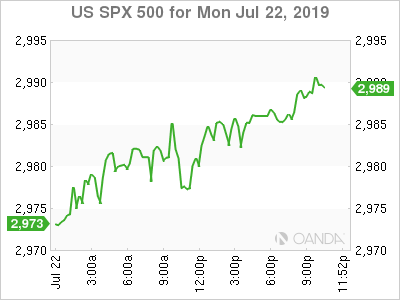

STOCKS

US stocks continued their winning ways as the Fed is expected to cut interest rates on July 31. Tech and energy stocks led the way as US President Donald Trump continued to pile pressure on the Fed to lower interest rates. The Fed is highly anticipated to lower the benchmark rate by 25 basis points in July but could intervene one or two more times in 2019.

US PMI data will provide guidance as the leading indicator could validate a more measured approach by the Fed or put even more pressure on the central bank to act now with a deeper cut to steady the economy.

Earnings data has been better than expected and given the pessimistic guidance not much was expected. Recession fears are still circling about, with Morgan Stanley putting a 20 percent chance of a recession next year.