- China’s manufacturing PMI returned to expansion at 50.4 (below 50 denotes contraction), with production increasing to a 5-month high. However, new orders fell to their lowest level this year and export sales were down as the trade war continues to bite. Furthermore, outlook for the next 12-months fell to one of its lowest levels in 12-months. So whilst the headline figure seems okay on the surface, the internal data is less so.

- Japan’s manufacturing PMI contracted for a 3rd month at 49.3 (49.4 prior), making it the 7th contraction this year after a 1-moth hiatus in March.

- South Korea’s manufacturing PMI contracted for a 5th month, although at a slower pace of 49 versus 47.3 in July. That Japan has since imposed trade restrictions on South Korea, we’d expect PMI to remain within contraction for the foreseeable future. Which is another red flag for global growth.

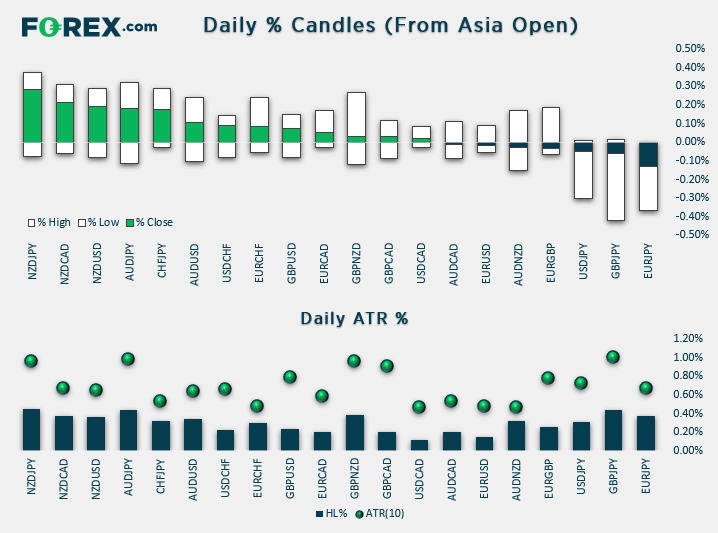

- Minor ranges for FX pairs at the start of the week, with the US 3-day weekend. JPY and USD are currently the strongest majors, CHF and AUD are the weakest. Although it’s difficult to read too much into this, given the lack of volatility.

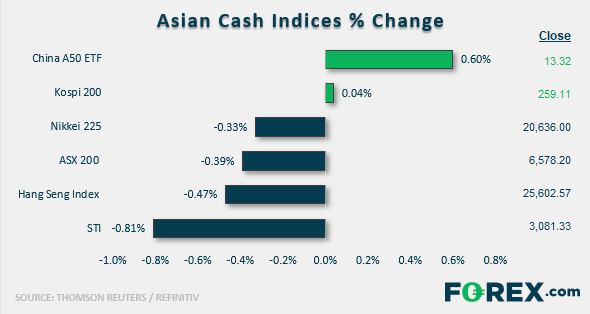

- A mixed picture across equity markets saw Chinese shares rise (led by the CSI 300) yet indices for Australia, Singapore and Hong Kong remained under pressure.

- Whilst the latest round of tariffs weighed on sentiment, Chinese shares were lifted by the positive read on manufacturing PMI.

- Futures markets saw the Hang Seng led indices across Asia lower today.

- Gambling revenues of Macau casinos disappointed to see equities in the sector in the red. Revenue for August was 24.3 billion, and -8.6% on the year to miss estimates of -2% to -6%

- Info tech and energy are leading the way lower for the ASX200, basic materials, technology and healthcare are the only positive sectors according to Reuters sector indices.

Up Next:

- With Labor day in the US and Canada, there’s no data to be released during the US session and volumes are expected to be low.

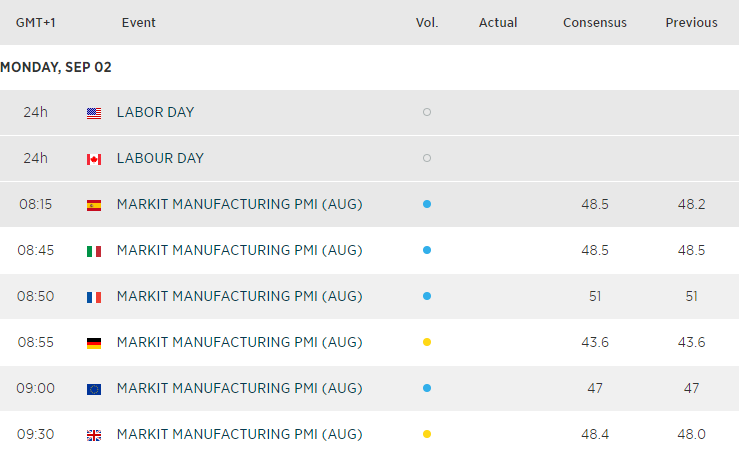

- It’s all about PMI’s today, with reads for Italy, Germany, Euro zone and UK lined up. This places Euro and GBP crosses on the radar, although Brexit developments and related court hearings are likely to be the bigger driver for GBP this week.