Executive Summary

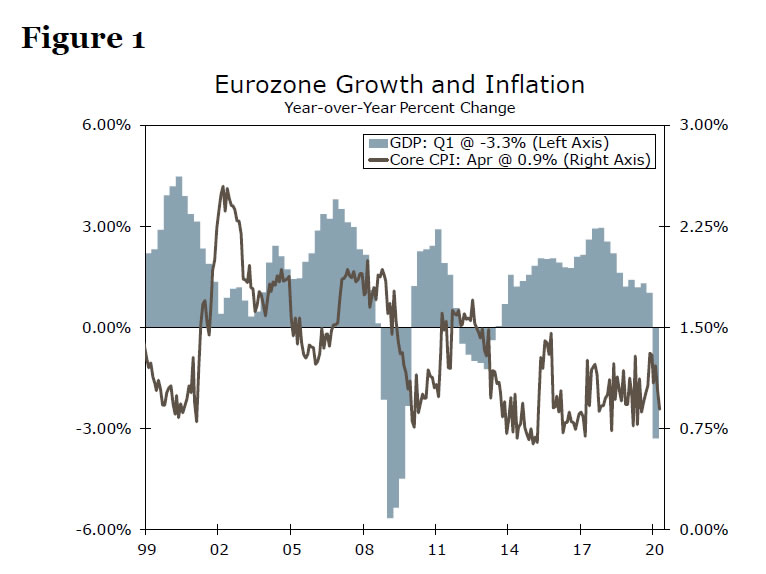

The Eurozone economy declined 3.8% quarter-over-quarter in the first quarter, matching expectations but still the largest quarterly decline on record, with sizable falls in French, Italian and Spanish GDP. April CPI inflation also slowed. The ECB eased liquidity policy at today’s meeting, and we currently expect the central bank to further expand its asset purchases at its July meeting.

ECB Eases Liquidity, Further Monetary Easing Still Likely

It is a busy day for data and events from the Eurozone. The initial estimate of Q1 GDP offered the latest measure of the damage inflicted by COVID-19 on the economy. Eurozone Q1 GDP shrank 3.8% quarter-over-quarter in Q1, the largest decline on record in data back to the mid-1990s, and fell 3.3% year-over-year. Separately, Q1 GDP figures for some large Eurozone countries were also released. French GDP tumbled 5.8% quarter-over-quarter, Italian GDP swooned 4.7% and Spanish GDP fell 5.2%. The individual countries reporting GDP so far represent just over half the Eurozone economy and imply the rest of the region’s economy (in aggregate) declined 2.4% quarter-over-quarter in the first quarter. That is consistent with a German Q1 GDP decline of perhaps 2.5%-3.5% quarter-over-quarter. A smaller fall in Germany relative to France, Italy and Spain would hardly be good news. Moreover, it is clear the Eurozone GDP news will get worse in Q2 before potentially improving later this year. Other data released today include a record German unemployment increase of 373,000 in April and a 5.6% month-over-month fall in German retail sales, while French March consumer spending nosedived 17.9% month-over-month.

The Eurozone April CPI figures were not quite as dire, though disinflationary pressures are clearly building. Headline CPI inflation slowed a bit less than expected to 0.4% year-overyear, on the back of lower energy prices. The core CPI eased to 0.9% year-over-year as services inflation slowed modestly. Given the weakness of economic growth and demand, we expect inflation to slow further in the months ahead.

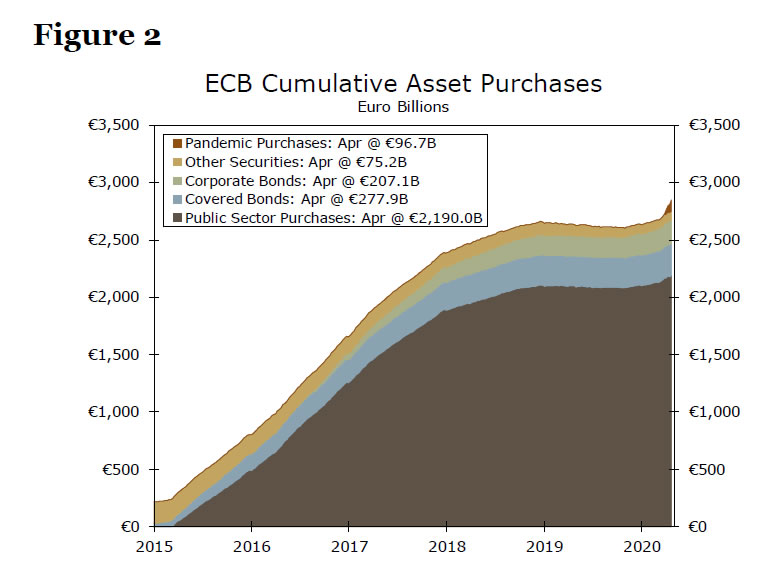

The European Central Bank (ECB) also announced monetary policy today. The ECB kept its policy interest rates steady and made no change to the size of its Asset Purchase Program (APP) or Pandemic Emergency Purchase Program (PEPP), while saying it is prepared to increase the size or extend those purchase programs if needed. However, the terms of the TLRTO operations between June 2020 and June 2021 were eased further, such that the financing cost will be as much as 50 bps below the average deposit rate over the life of those loans. The central bank also announced seven non-targeted pandemic emergency longerterm refinancing operations (PELTROs) to be conducted between May 2020 and September-2021, with the financing rate 25 bps below the average main refinancing rate over the life of those loans.

We currently expect the ECB to increase the size of its PEPP program a further €500 billion at its July meeting and likely extend that program by a few months. Before easing monetary policy further, we think the ECB would ideally like to monitor the economy and COVID-19, as well as assess the impact of its various LTRO operations, through Q2. The risk is clearly for an earlier policy move though, likely depending on the stability of Italy’s bond market in the interim.

{kind=link}