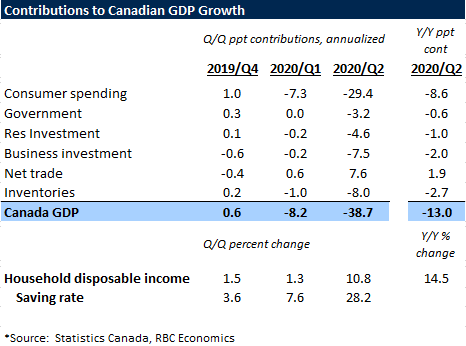

- GDP declined 38.7% (annualized) in Q2 – close to expectations

- Drop in Q2 concentrated in April, June GDP rose 6.5% after a 4.8% May gain

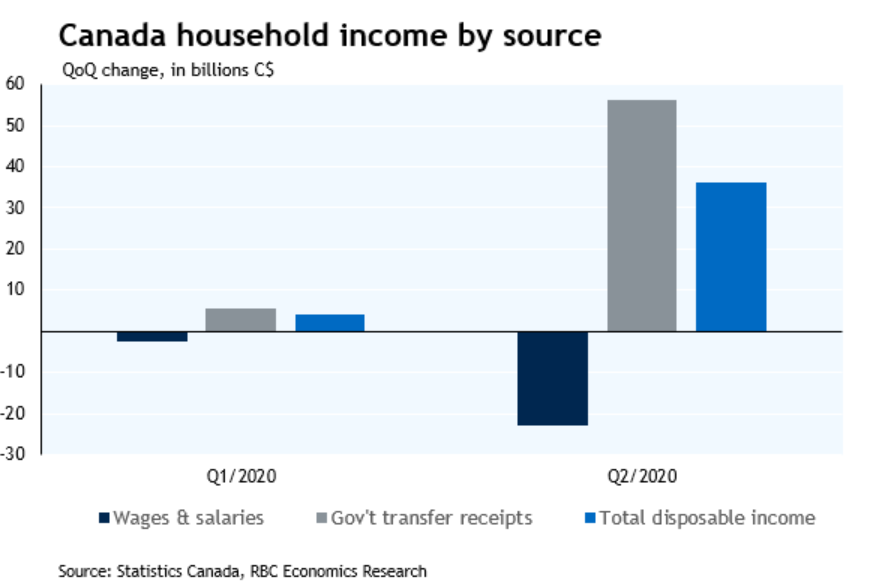

- Household disposable income surged higher despite labour market downturn

The 38.7% (annualized) drop in GDP in Q2 was more than 4 times the biggest prior drop, and built onto an 8.2% plunge in Q1. The pull-back was widely expected at this point, though, and was still slightly less-bad than the 43% Q2 decline the Bank of Canada assumed in the July Monetary Policy Report.

Consumer spending plunged a record 43%, but that was still not quite as weak as the 57% drop in business investment. Virus containment measures clearly weighed on both, with a plunge in oil & gas investment tied to lower oil prices also a factor in the latter. Even government spending posted a sizeable decline with containment measures curtailing normally non-cyclical government services. Net trade was one of the few positive contributors in Q2, but only because imports fell even more than exports.

As-expected, weakness on a monthly basis was heavily concentrated in April, when containment measures were at their peak. GDP rose 4.8% in May and another 6.5% in June. Statistics Canada’s preliminary estimate of July GDP was up another 3%. Together, those gains still only retrace about two-thirds of the 18% 2-month decline over March and April. But that would still leave risks tilted if anything to the upside of our call for a 33% (annualized) bounce-back in GDP in Q3.

The size of that early bounce-back has clearly been helped by the exceptional level of government policy supports for households. Household disposable incomes actually rose almost 11% (non-annualized) in Q2 despite a massive downturn in labour markets. Government transfers to households surged by a whopping $56 billion in Q2 (likely the bulk from CERB payments) versus a $23 billion decline in earned wages & salaries. Retail sales were already already above year-ago levels by June, and home resales have soared into the summer (helped also by pent-up demand from delayed transactions in the spring and low interest rates).

That income boost has also been expected for some time with payments from CERB well-publicized. The concern has long been that still exceptional softness in labour markets (the unemployment rate was still in double-digits at 10.9% in July) would outlast exceptional policy supports. Although the new programs announced last week by the federal government to replace CERB will help ease that transition.

To be sure, the recovery from the pullback in the first half of this year will not be quick, even with an early bounce-back that looks stronger than feared. Labour markets are still exceptionally soft, and it will take time to reconnect workers with jobs. Activity in the oil & gas sector is still very depressed, and possible resurgence of virus spread will remain a risk until and unless an effective vaccine can be distributed. We continue to expect the economy to operate well-below capacity into next year, but perhaps not quite as far below capacity as previously feared.

{kind=link}