Executive Summary

The most significant change to U.S. monetary policy over the past few months occurred not at a regularly scheduled FOMC meeting, but rather at the Kansas City Fed’s annual Jackson Hole Symposium, which was held virtually this year. During a speech for the symposium on August 27, Federal Reserve Chair Jerome Powell announced that the FOMC would adopt a flexible average inflation targeting regime. Going forward, the committee will aim to “achieve inflation that averages 2% over time.” Powell also revealed that the FOMC will take a more dovish view of labor market developments, stating that monetary decisions will be informed by “assessments of the shortfalls of employment from its maximum level” rather than “deviations from its maximum level.” The upcoming FOMC meeting, to conclude on September 16, will be the first official meeting since these announced changes and will afford Powell the opportunity to further expand upon these major changes to the Fed’s operating framework.

The upcoming FOMC meeting will contain more than just additional information about average inflation targeting. The September meeting will include the first update to the fed funds dots and Summary of Economic Projections (SEP) since June, as well as the initial rollout of 2023 forecasts from FOMC participants. We expect the vast majority of participants will indicate that a fed funds rate between 0.00-0.25% will still be appropriate in 2023 given the new framework. Another key topic will likely be whether the committee has moved any closer towards explicitly tying future rate hikes with time- or objective-based metrics, such as the unemployment rate or inflation. Our sense is that the FOMC is in no rush to tie its hands in this way, but deliberations are likely to continue on the topic at the September meeting. With the fed funds rate likely anchored at zero for several years to come, short- and intermediate-term Treasury yields should remain stuck near current levels. Past the 5Y point, we see moderately higher inflation as a possible catalyst for higher yields.

Average Inflation Targeting: What’s the Deal?

The Federal Reserve has long conducted monetary policy with the goal of satisfying its dual mandate of price stability and maximum employment. In terms of the inflation half of that mandate, the FOMC has held that 2.0% is the inflation target best suited to achieving price stability. After years of inflation coming in below that target, the Fed recently underwent a review of the various policy tools used to achieve its mandates. One of the major outcomes of that review announced at the Jackson Hole Symposium was the Fed’s embrace of “average inflation targeting.” The FOMC voted unanimously to embrace this new approach. So what exactly is average inflation targeting, and how does it change things?

Anchors Away

Financial markets are good at identifying and pricing variable outcomes. When it comes to inflation, monetary policymakers, not just at the Federal Reserve but also many foreign central banks, wrestle with the fact that inflation expectations become anchored to a particular rate. John Williams, the president of the Federal Reserve Bank of New York, has framed the issue as a pricing in of the complete business cycle. He cites an example of an economy in the expansion phase of the business cycle about 80% of the time and in recession the other 20% of the time. His point is that during the expansions, the Federal Reserve generally does an adequate job of keeping inflation around 2.0%; but during recessions, inflation often comes in closer to 1.0%. In Williams’ own words, the “resulting average rate of inflation is about 1.8%. As a consequence, inflation expectations are likely to become anchored at the long-run average of 1.8%, below the desired 2.0% target.”1

In our view, Williams’ way of thinking makes the most pragmatic case for the need to allow inflation to overshoot a bit during economic expansions, such that long-term inflation expectations become anchored to the appropriate target. To some extent, the Federal Reserve has already implicitly done this, though in prior periods Fed officials would go through linguistic exercises when it allowed above-target inflation, assuring markets that it was “looking through” a temporary driver or that higher inflation was “transitory”. The more formal embrace of this new tolerance for above-target inflation plants the seeds for a new era of policymaking. If the Fed is indeed able to anchor inflation expectations at 2.0%, it would lift nominal interest rates during expansions and effectively give the Fed more “ammunition” via rate-cuts the next time a recession comes along.

A Later Curfew?

To the extent that we are really in a new era, one of the questions financial markets will want to explore is just how much of an inflation overshoot the FOMC will allow without signaling a less accommodative policy path. In the past, a classic metaphor has been that the Fed takes away the punchbowl before the party gets too raucous. The interpretation of that metaphor for this era is the following: there is a later curfew, but rather than get a clear delineation of exactly when it is, there will just be some testing of “how late is too late?” without pushing it too far.

There were no immediate answers to these questions at Jackson Hole, and we do not expect to get much clarification at the September 16 meeting either. The Fed is being deliberately vague about the extent of the inflation overshoot it will tolerate, which is why Chair Powell deliberately referred to the new program as a “flexible form of average inflation targeting.” Although we do not anticipate inflation climbing above 2.0% on an ongoing basis in the next couple of years, eventually it could, which will afford the opportunity for some “price discovery” around the Fed’s tolerance range.

When pressed on this in an interview during the Jackson Hole Symposium, St. Louis Fed President James Bullard said “I don’t think you want to get into precise mathematical formulas here. But the spirit of this is that, in the committee’s judgement, it would be wise to allow inflation to be above target for some time to make up for past misses.” That is the essence and spirit of average inflation targeting in a nutshell.

I Used to Hurry a Lot, I Used to Worry a Lot

The new Summary of Economic Projections (SEP) will be the clearest signal yet that the FOMC will be slower to raise rates under its new policy framework. Near-term changes to the SEP should be inconsequential. The virus continues to impart a tremendous amount of uncertainty to the economic outlook, making it unwise to read too much into tweaks to the SEP over the next year or so. Moreover, the outlook has not fundamentally changed. Most observers still expect the economy to operate at a significantly reduced capacity over the next year or two, which should be borne out in the 2020 and 2021 projections for GDP growth, the unemployment rate and inflation.

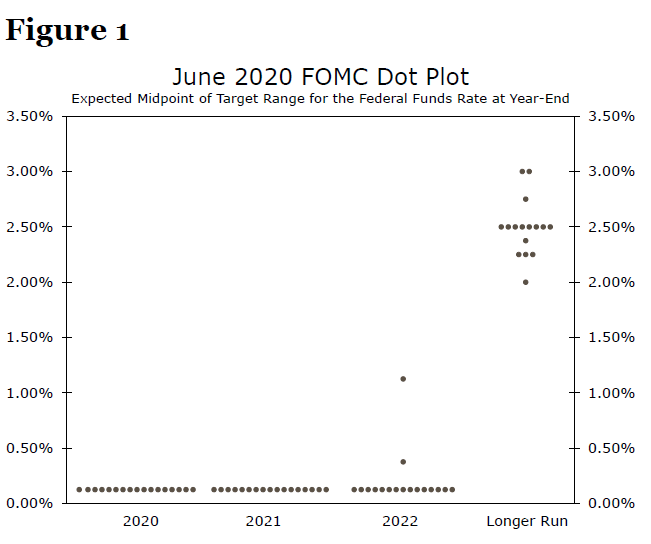

Beyond 2021, however, the SEP should more clearly illustrate the Fed’s new reaction function. The new framework should push out the timing of rate hikes as the committee seeks to see inflation run somewhat above 2% for a time, rather than merely return to 2%. Given that the adoption of the new approach was unanimous, we would anticipate that all FOMC members now expect rates to remain on hold through 2022 (versus two members who in June projected at least one rate hike in 2022—Figure 1). After all, the top end of core inflation projections in June registered 2.2%, which we see as consistent with price growth only “modestly” above 2%.

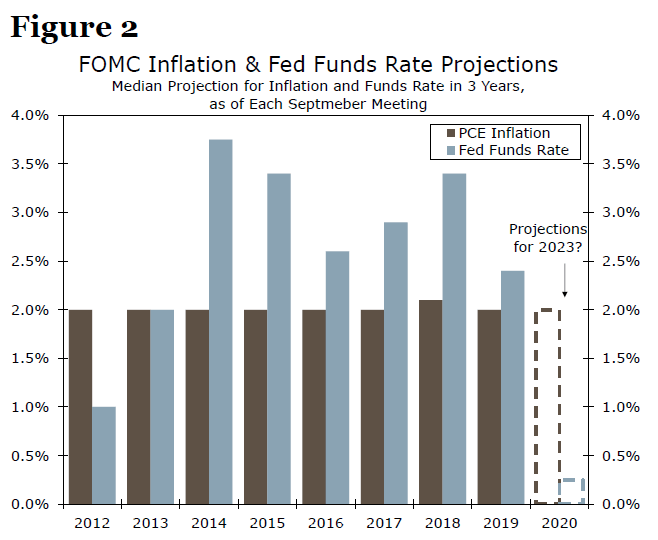

Projections for 2023, which will be added in the September SEP, will be more interesting, in our view. Since the inception of the SEP, the committee has anticipated inflation would return to 2.0% within three years’ time. With the committee fessing up to the fact that 2% inflation is more difficult to achieve than previously envisioned, we would not be surprised to see the median estimate for 2023 remain slightly shy of 2%. Even if the SEP echoes prior optimism that a return to 2% inflation is “only” three years away, we expect the vast majority of participants will indicate that a fed funds rate between 0.00-0.25% will still be appropriate in 2023 given the new framework—a clear break from the past (Figure 2).

As for the longer run, the FOMC’s reaffirmed its goal of 2.0% inflation in its updated Statement on Longer-Run Goals and Monetary Policy Strategy. Projections of longer-term inflation should be unchanged as a result. The long-term outlook for unemployment could fall marginally. Under the FOMC’s new operating framework, low unemployment is not in and of itself a reason to tighten monetary policy. By allowing inflation to run moderately above 2% at times, the FOMC’s more accommodative policy stance should support a slightly lower unemployment rate over time. However, any change to the long-run rate of unemployment should be small because, as the FOMC acknowledges, the labor market is heavily influenced by nonmonetary factors. The new framework should also not lead to a meaningful change in estimates of the longer-run fed funds rate, since it fundamentally does not change the outlook for the real fed funds rate over time and inflation will still be expected to run at 2%.

As we discussed in our Fed Flashlight report in July, the SEP is one way in which the FOMC can provide forward guidance. We would expect officials to discuss forward guidance somewhat further, but the latest projections will give a better sense of how the FOMC sees the economy evolving while at the same time signaling it will be in no hurry to raise the fed funds rate. As a result, we think the announcement of the new framework in concert with the lower path of the dot plot will allow the FOMC to hold off on any calendar- or threshold-based forward guidance for now.

What Is the Outlook for Treasury Yields in this Brave New World?

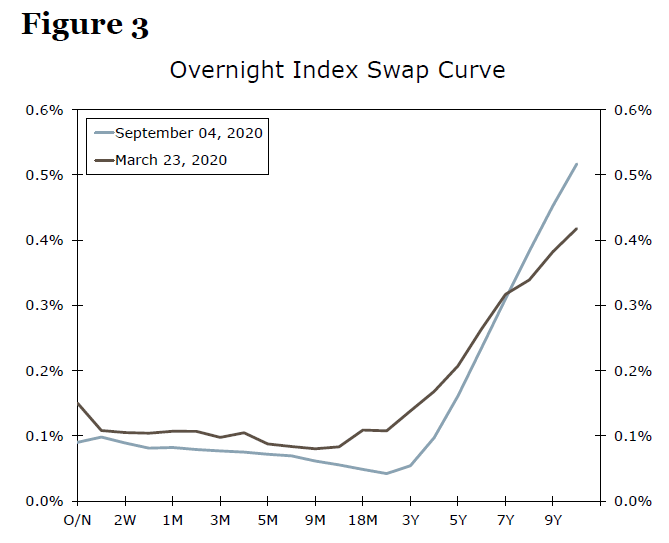

We expect Treasury yields to remain anchored through the 5Y point for the foreseeable future. The adoption of a flexible average inflation targeting framework and new emphasis on achieving maximum employment is clear communication that the fed funds rate will remain very low for a very long time, which should keep rates anchored in the “belly” of the curve as well. Market pricing based on the term structure of overnight index swaps (OIS) shows the curve is inverted from overnight through the 3-4Y point and essentially flat out to five years (Figure 3). A material increase in Treasury yields in the front end and belly of the curve would need to be accompanied by a shift higher in market pricing for the policy rate, in our view. This seems unlikely to occur any time soon given the recent shift in longer run monetary policy strategy.

Farther out the curve, average inflation targeting may give long-term yields a boost. The new framework is a clear departure from past principles where the FOMC would tighten policy preemptively in order to prevent an inflation overshoot. Now the focus has shifted to achieving its maximum employment goal first and waiting to see a more sustained period of inflation in excess of its 2% target. This should help push inflation expectations gradually higher and take long term yields along for the ride.

A key risk to our forecast for long-term yields to rise is a potential shift in the Fed’s stance on asset purchases. Currently the Fed is buying $80 billion per month in Treasury securities across the curve, with purchases distributed to roughly reflect the composition of total marketable Treasury debt outstanding.2 A shift to a more traditional quantitative easing (QE) program, where the focus is to push yields on U.S. Treasury securities lower in an effort to reduce other long-term borrowing costs, would put a cap on how high long-term rates can rise from today’s levels. We do not expect a shift in the stance on asset purchases at the September FOMC meeting. But, a recent speech by Fed Governor Brainard noted the importance of a “pivot from stabilization to accommodation.” The comment was not geared directly toward asset purchases, but up to this point the Fed has maintained that asset purchases have been focused on restoring smooth market functioning (stabilization). The speech may have laid the groundwork for an eventual shift to purchases further out the curve (accommodation).

1 Remarks by John C Williams, President of the Federal Reserve Bank of New York, at the 80th Plenary Meeting of the Group of Thirty, Federal Reserve Bank of New York, New York City, 30 November 2018. https://www.bis.org/review/r181206a.pdf

2 A key caveat to this is that the Fed is not currently buying Treasury bills. Coupon purchases are distributed roughly proportionally to marketable coupon notes and bonds outstanding. See the NY Fed website for additional detail on Treasury purchases.

{kind=link}