Market movers today

Today is a quiet start to the week on the data front.

US election. Focus continues to be on the repercussions of the US election.

We will keep a close eye on the COVID-19 situation. There might be more partial lockdowns and maybe we will start to see some positive impact on the virus numbers in the countries that had imposed restrictions early.

ECB. Later this week ECB’s annual Forum will take place with a significant number of ECB officials speaking. Draghi has previously used this occasion to signal policy changes. However, we doubt such messages will be conveyed this year due to ECB’s pre-announcement of new measures in December.

The 60 second overview

US election. Over the weekend, Joe Biden was declared the winner of the US election by almost everyone, except perhaps president Donald Trump and his supporters. However, it may very well be that Joe Biden won the battle but lost the war, as the Democratic Party may not win the majority in the Senate, rendering it impossible for president-elect Biden to get his economic policy through Congress.

It all boils down to whether the Democratic Party is able to win both special Senate runoffs in Georgia taking place on 5 January (if it wins it would be 50-50 and vice president-elect Kamela Harris would have the decisive vote). Unfortunately for the Democratic Party, Georgia is usually considered a Republican state. Short term, president-elect Biden has made it clear that the first thing on his agenda will be the handling of COVID-19 and he has already created a COVID-19 task force. Also remember that although Biden may turn out to be a ‘lame duck’ on domestic policy due to a divided Congress, he would have much more power in foreign policy and we will most likely see a normalisation of the relationships with the EU, NATO, WHO and WTO. See also Harr’s View: Why markets should ignore US election uncertainty, 8 November 2020.

Brexit – keep talking. Over the weekend, PM Boris Johnson and EU Commission President Ursula von der Leyen agreed to continue negotiating in the upcoming week with the next soft deadline mid-November looming. We have yet to see any signs of white smoke but on the other hand we have not seen the same tendency to yell at each other in the media. We continue to expect a simple free trade agreement but will admittedly be more concerned if there is no progress around 1 December, so the next three weeks are going to be important.

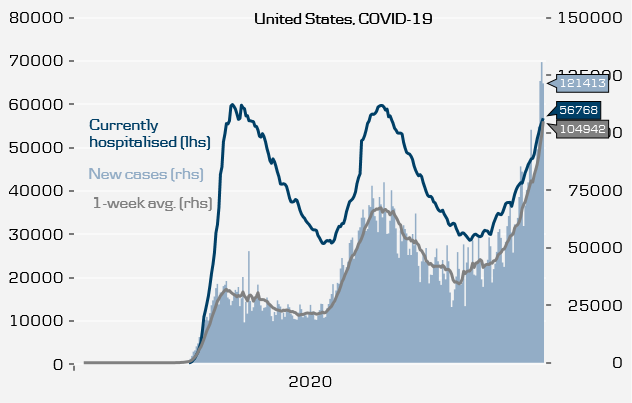

COVID-19. We will also keep a close eye on the COVID-19 situation. US COVID-19 cases rose to a new high over the weekend moving above 120,000 cases per day, see chart.

There is a clear risk the rise in big gatherings during the election days will lead to a further push higher over the coming week. In Europe new cases also keep rising but some of the countries that introduced lockdown measures early start to see improvement (Ireland, the Netherlands and Czech Republic). On a positive note, AstraZeneca’s CEO last week said a vaccine could be ready by the end of December or early January.

Macro. Chinese exports surprised to the upside over the weekend rising 11.4% y/y (consensus 9.2%). The vice governor of the People’s Bank of China warned Friday of a monetary exit saying ‘exit is a matter of timing and it is also necessary’. In Turkey the finance minister resigned over the weekend, a day after the central bank governor was fired.

Equities. In Asia stock markets have extended the rally from last week with most Asian indices seeing robust gains. The S&P500 future is close to recent highs after adding close to 2% pulled higher by rising optimism in the tech sector.

FI. After trading close to recent lowest levels, German and US bond yields increased after the stronger than expected US labour market report. On Friday, Moody’s upgraded Greece to Ba3 (still three notches below IG) despite the negative impact from the coronavirus.

FX. EUR/USD failed to break 1.19 on Friday and while EUR/NOK held above the 10.85 level held back as oil prices crept lower, EUR/SEK closed the week at lows (10.25) not seen since August. Meanwhile USD/JPY held firm at recent lows while a range of EM currencies including MXN and CNY have seen continued support.

Credit. Markets started Friday on the back-foot, but recovered in the late hours of trading. Both iTraxx Xover and Main tightened 2bp ending in +314bp and +53bp, respectively. In cash bonds the tightening was only prevalent in HY (-2bp) while IG was unchanged. The positive tone was mainly driven by the decent non-farm payrolls and a strong Biden finish in the US election.

Nordic macro and markets

We have no big market movers today but attention will be on inflation prints in both Norway and Sweden this week.

{kind=link}