The European Central Bank will conclude its meeting at 12:45 GMT Thursday. Markets widely expect an easing package of around €500bn in QE purchases, likely complemented by more ultra-generous loans to banks. Yet, this move has already been telegraphed and priced in, so if policymakers want to sink the supercharged euro, they need to deliver something larger – which may be difficult. In the bigger picture, the euro may be driven mostly by Brexit and the US stimulus game.

Houston, we have a problem

The ECB is in a tough spot. Back at its previous meeting, it pre-committed to delivering a significant easing package in December to help the European economy get through the new lockdowns. President Lagarde highlighted the mounting risks and made it clear her central bank will deliver at this meeting.

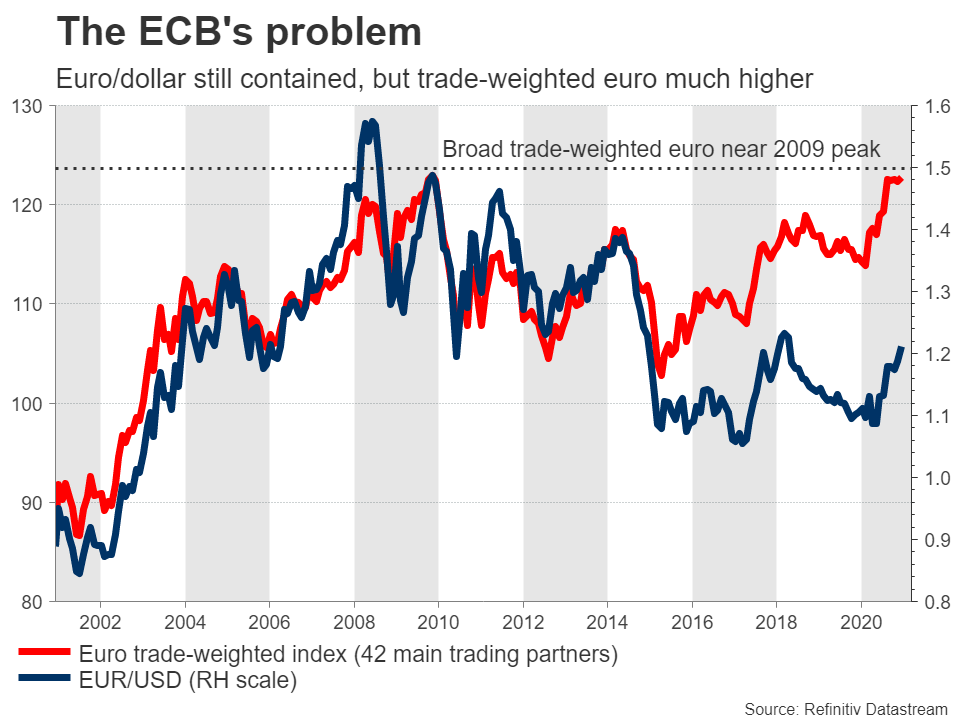

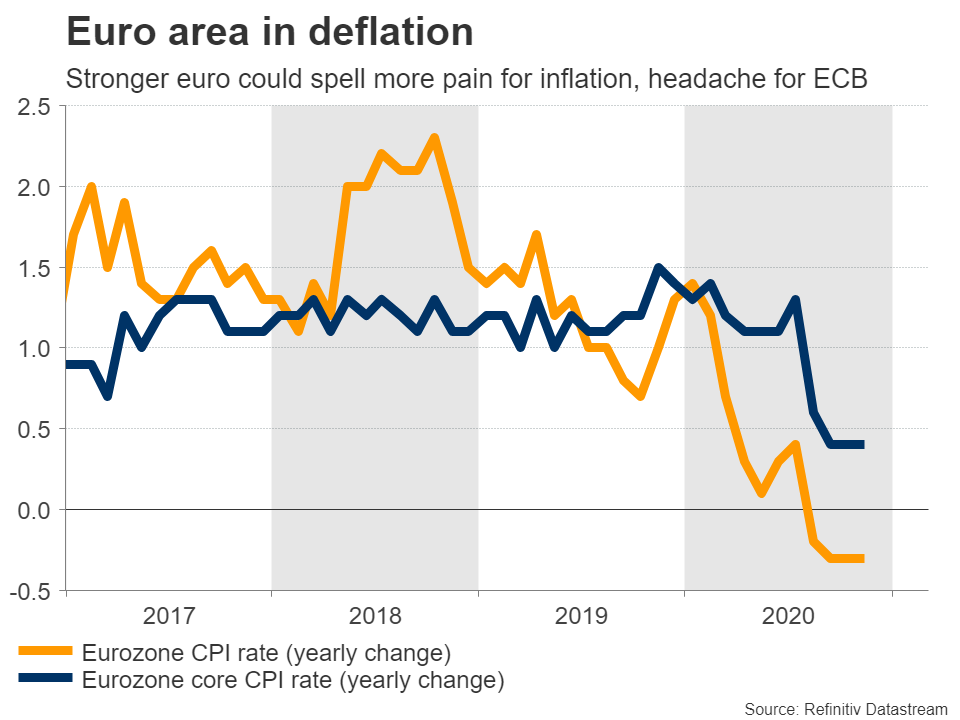

The problem is that all this has been priced into the euro already, and yet the currency continues to surge. The broad trade-weighted euro, which is what the central bank cares about, is near its peaks from 2009. A stronger currency can hold back economic growth and inflation. Considering that the Eurozone is already in deflation, an even stronger euro could be a real headache for the ECB.

So what can a central banker do? In a situation like this, the ECB wants to deliver something larger than investors expect, to push the euro back down. The consensus is for another €500bn in QE purchases, so if the ECB wants to clip the euro’s wings, it needs to deliver a package of around €750bn. A rate cut could also do the trick, but judging from recent comments, there is no appetite for that yet.

Why is over-delivering difficult?

The main reason is the division within the Governing Council between ‘doves’ and ‘hawks’. The doves argue the ECB should go all-out, as the risks of not doing enough outweigh the risks of doing too much. The hawks argue that with interest rates already negative, the benefits of more QE are minimal and doing too much could encourage excessive speculation, fueling asset bubbles.

Likewise, when the ECB pre-committed to a new stimulus package back in October, vaccines had not been announced yet. The vaccine news won’t have any impact now, but it does minimize many of the longer-term risks, so some policymakers may feel it is unnecessary to go all-out.

To be clear, this doesn’t mean the ECB cannot over-deliver. It can, and President Lagarde will push for that, but she may not succeed. Perhaps a ‘cheaper’ solution is to simply voice concern about the exchange rate. However, that is unlikely to work either. The markets only respond to ‘jawboning’ when there is a credible threat of action to back it up. Just saying you want a weaker euro doesn’t work for long, and the ECB has already played this card.

Market reaction and the big picture

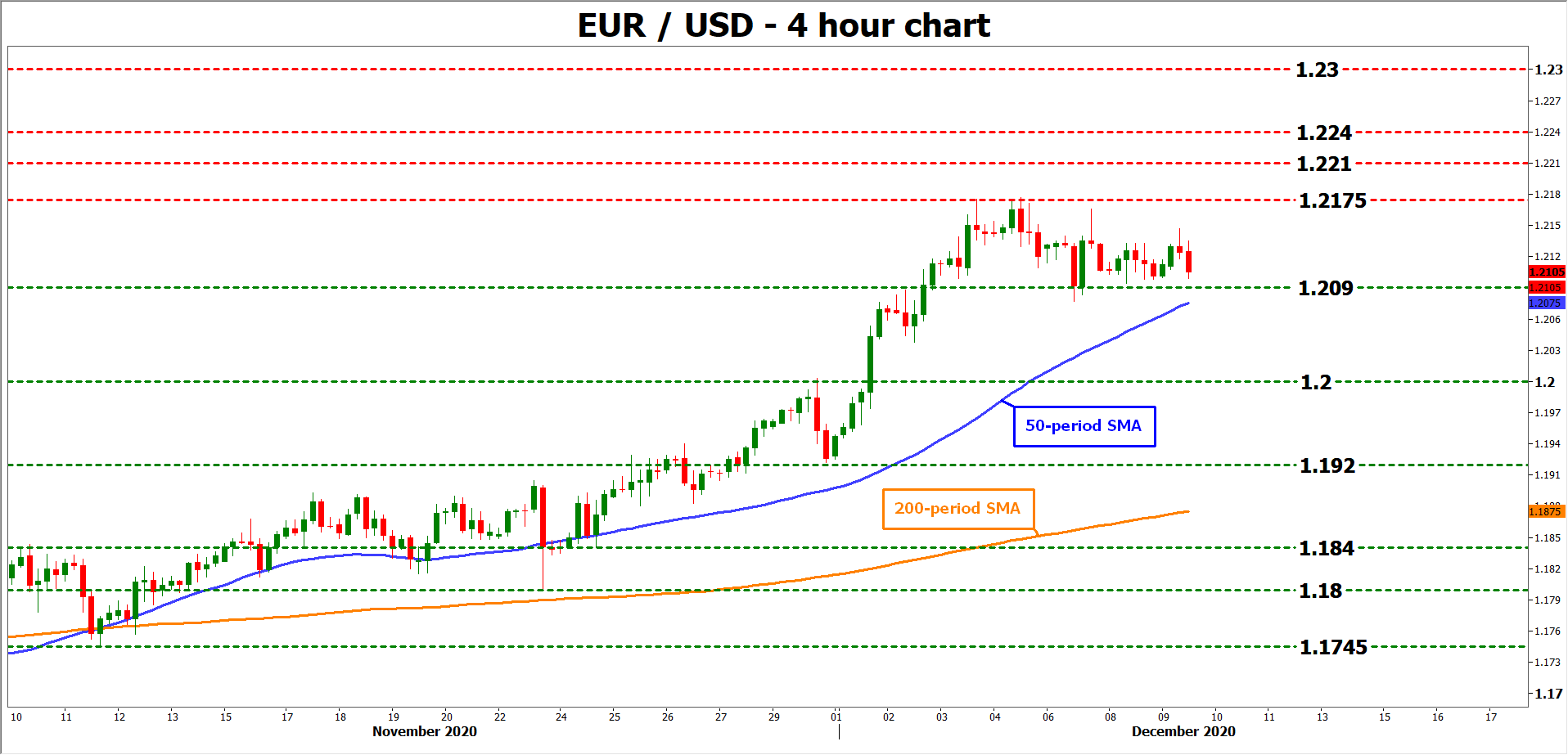

If markets are indeed disappointed by the size of this package, the euro could move higher. Taking a closer look at euro/dollar, a potential spike up may stall initially around 1.2175, where an upside break could turn the focus towards 1.2210.

Otherwise, if the ECB manages to overdeliver, immediate support may be found near 1.2090, with a downside break opening the door for the 1.2000 handle.

In the bigger picture, the euro’s fate hangs mostly on external factors, namely on how the Brexit saga concludes and how big of a relief package the US Congress delivers.

A Brexit deal being completed soon could catapult both the pound and the euro higher, but on the other hand, the downside for both currencies in case of no-deal may be even bigger as markets have already priced in a lot of optimism. A deal still seems like the most likely outcome, but it may be a stormy ride until we get there.

The other downside risk may be a stronger dollar. Short-dollar/long-euro is already a very crowded trade, which implies that any piece of good news for the dollar could lead to a powerful rebound as shorts are ‘squeezed’. The catalyst for that could be a smaller-than-expected relief package from Congress or a risk-off episode that fuels safe-haven demand for the reserve currency.

{kind=link}