Sunrise Market Commentary

- Rates: US eco data are key this week

The Jackson Hole meeting turned out to be a non-event with markets now looking to this week’s US eco data to get trading guidance. The calendar is back-loaded, suggesting a slow start today. US Hurricane Harvey left no traces on markets with Brent crude stable around $52.5/barrel. The US Treasury’s supply operation could weigh on US Treasuries. - Currencies: EUR/USD extends gains as Draghi stays muted on recent strength

Yellen and Draghi didn’t bring any news on monetary policy last Friday. However, markets interpreted it as a ‘Nihil obstat’ to further sell the dollar and buy the euro. Today, the eco calendar is thin. Especially the price data in the EMU and the US later this week might by key for EUR/USD trading. Is enough bad news for the dollar discounted?

The Sunrise Headlines

- US equities closed the final session of last week’s trading mixed with a small outperformance of the Dow Jones. Overnight, most Asian equity indices trade positive with China outperforming.

- Theresa May is facing renewed pressure from her own party over Brexit after Labour announced it would change tack and campaign to keep Britain in the EU single market, at least during a transitional period.

- The ECB’s ultra-easy monetary policy is working and the euro zone’s economic recovery has taken hold even if more time is needed to lift inflation to the bank’s 2% target, ECB President Draghi said on Friday in Jackson Hole.

- Earnings growth for China’s industrial firms cooled in July after accelerating for three straight months, reinforcing expectations the economy will slow over coming quarters as higher lending costs and property market curbs bite.

- China’s central bank raised its official yuan midpoint to 6.6353 per dollar, the strongest level since Aug. 19, 2016, reflecting broad weakness in the US currency in global markets.

- Houston and surrounding areas faced epic flooding and more days of heavy rain from Tropical Storm Harvey, which turned freeways and roads into rivers, inundated homes and required rescues for thousands of stranded people.

- Today’s eco calendar contains EMU M3 money supply data and the US trade balance. The US Treasury starts its end-of-refinancing operation with a $26B 2-yr Note and a $34B 5-yr Note auction.

Currencies: EUR/USD Extends Gains As Draghi Stays Muted On Recent Strength

EUR/USD up as Draghi is muted on EUR strength

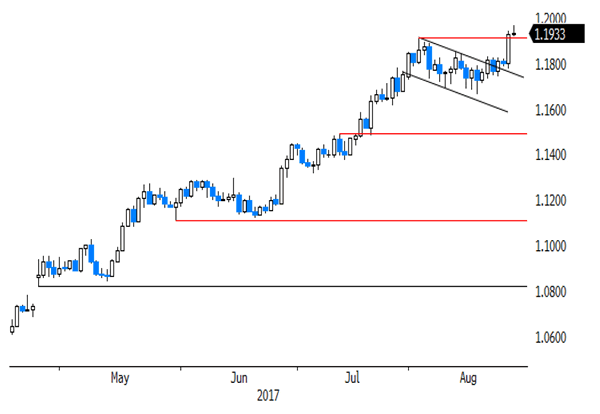

On Friday, the speeches of Fed’s Yellen and of ECB’s Draghi at Jackson Hole didn’t bring any concrete news on monetary policy. The focus was on the appropriate level of financial regulation and on free trade. Even so, currency markets still reacted to what wasn’t said. Yellen stayed muted on the timing of further US rate hikes and ECB’s Draghi didn’t give an open warning on the recent rise of the euro. Especially the latter was considered as a ‘nihil obstat’ for further euro gains. EUR/USD set a correction top north of 1.19 and closed the week at 1.1924. USD/JPY also dropped off the intraday highs and finished the session at 109.36.

Overnight, Asian equities trade mixed to slightly higher. Japanese indices are little changed as USD/JPY returned to the low 109 area post-Jackson Hole. The PBOC set the fixing of USD/CNY at the strongest level for the yuan since August last year. The dollar remains in the defensive across the board. The trade-weighted dollar trades in the 92, 50 area. EUR/USD remains well bid and trades in the 1.1920 area.

The economic calendar is thin today. In EMU, the M3 money supply is expected marginally lower for July (4.9% Y/Y from 5% Y/Y). We look whether the growth continues to recover. However, markets usually ignore the M3 release. In the US, the inventory and the trade balance figures for July are interesting for fine-tuning the early estimates of Q3 GDP. However, we expect it only to be of intraday significance. Investors will look forward to a series of important eco data in EMU (CPI) and the US (consumer confidence, PCE deflators, payrolls) later this week. Markets will look for confirmation that recent good US eco data might allow the Fed to continue its path of gradual rate hikes. The fiscal plans of the Trump administration, unveiled later this week, are a wildcard for USD trading. In a day-to-day perspective dollar sentiment clearly remains fragile. Friday’s reaction of the dollar and the euro told more about underlying market sentiment than on content of the speeches of Draghi and Yellen. For now, there is no indication that a the dollar decline/euro rally will halt right now. However, Friday’s jump in EUR/USD occurred even as changes in interest rate differentials remained very limited. This kind of divergence between interest and FX markets can’t continue for ever. We also look out for more outspoken comments from ECB members on the recent euro rally and on its impact on inflation and monetary policy .

Broader context and technical picture. Late June, EUR/USD started a new up-leg as investors anticipated a reduction of ECB bond buying. The Fed was expected to remove policy stimulation only in a very gradual way as US inflation remains soft. Uncertainty on the policy of the Trump administration was a secondary negative factor for the dollar. EUR/USD set a new correction top north of 1.19 before consolidating in a narrow 1.1662/1.1910 range. The top of this range is now again under severe strain post Jackson hole. The day-to-day momentum remains euro positive. However, we assume that the EUR/USD rebound has gone far enough if the recent improvement in USD eco will be confirmed. A return of EUR/USD to the 1.15/16 area is possible. Pockets of US political risk are a (negative) wildcard for the dollar.

A downward correction in core (US and European) yields supported the yen in August. USD/JPY declined from mid-114 mid-July to 108.60. The April correction low (108.13) remains the line in the sand. For now, this level won’t be easy to break as quite some USD bad news is discounted after the recent protracted setback. A cautious buy-on-dips approach (with stop-loss protection below 108) may be considered.

EUR/USD: ‘by default’ euro buying persists

EUR/GBP

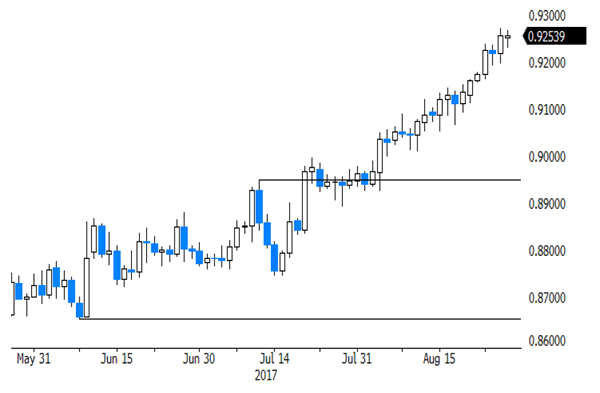

EUR/GBP rally resumes on euro strength

Sterling trading was order-driven in absence of eco releases. There was again a lot political position talking ahead of this week’s new round of the Brexit-talks. EUR/GBP initially hovered in the 0.92 area, but jumped higher in lockstep with the rise of EUR/USD after the speeches of Yellen at Jackson hole. EUR/GBP finished the session at 0.9255. At the same time, cable also profited from the USD decline and finished the session at 1.2882.

There are again no UK data today. So, FX traders will focus on the start of the third round of Brexit negotiations. The focus remains on the separation issues rather than on the cooperation between the two blocks in the post-Brexit era. In theory , this should be negative for sterling. However, we have the impression that the UK negotiators are turning less strict. For now, this didn’t help sterling. Even so, especially the EUR/GBP cross rate already discounts a lot UK negative news. We look for a signal that the rally has run its course.

From a technical point of view, EUR/GBP cleared 0.8854/80 resistance (top end June), opening the way for further gains. The move was the result of euro strength (strong EMU data and expectations of APP tapering). Simultaneously, UK price data were soft enough to keep the BoE side-lined as the Brexit negotiations continue. MT, we maintain a buy EUR/GBP on dips approach as we expect the combination of relative euro strength and sterling softness to persist. The 0.9415 ‘flash-crash spike’ is the next target on the charts. However, we don’t jump on the up-trend anymore after the recent rally and wait for a correction, e.g. to the technical support in the 0.88/89 area.

EUR/GBP: rally resumes on Euro strength