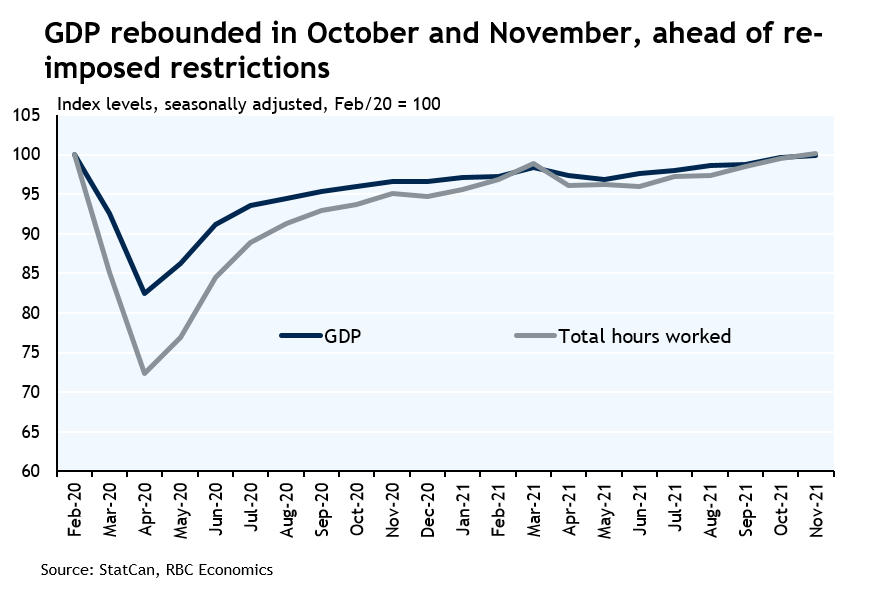

- GDP grew 0.8% in October, backed by a bounce-back in goods-producing industries.

- Preliminary estimate that output grew another 0.3% in November, despite significant disruptions from flooding in BC.

- Omicron threat and re-imposed containment measures adding downside risk near-term, but impact still uncertain.

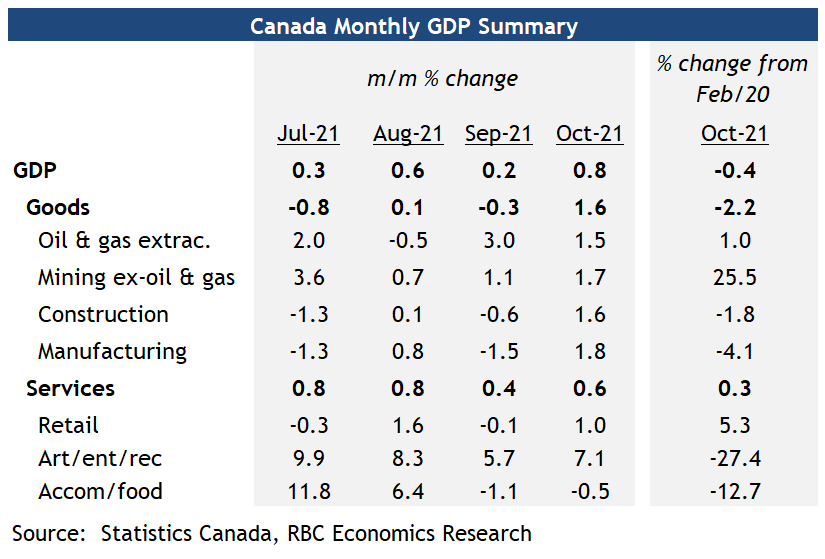

GDP in Canada rose 0.8% in October as supply chain disruptions eased, at least temporarily. Motor vehicle and parts manufacturing jumped 19% after falling sharply in September, but was still almost a quarter below levels in October a year ago with the global chip shortage restraining output. The same is true for auto-related wholesale and retail activities, both of which declined from July to September but rebounded more substantially in October, albeit to levels still below a year ago. Outside of auto products, oil and gas extraction also rose again in October and has now recovered back to above pre-pandemic levels. Oil prices have ticked lower in recent weeks over worries about travel demand given the spread of the Omicron variant, but remain above pre-pandemic levels. Finally, both residential and commercial building activities also posted solid gains in October, pushing construction output higher by 1.6%.

The preliminary estimate of November output growth was up 0.3% from October, smaller than the 0.7% increase in total hours worked earlier reported. Part of the underperformance could be attributed to significant disruptions to local transportation capacity brought on by flooding in British Columbia, which happened after the labour market survey week. Advance estimates of November retail and wholesale trade in November were higher. And early data’s pointing to another increase in auto production as well. We expect the ebb and flow of global supply chain disruptions to continue to impact output, particularly from the manufacturing sector in coming months.

The impact of the new Omicron variant on the economic outlook remains highly uncertain. The re-imposition of some restrictions to hospitality and travel industries will limit growth in the near-term. And health-related concerns might dampen services demand. But how long these restrictions last and how stringent they become are difficult to predict. Still, high rates of vaccination, extended government benefits and accelerated booster rollouts are all expected to help curb the threat. We continue to expect downward but at this time limited impact to our Q4 GDP growth tracking of 6.5%.

{kind=link}