The threat of rising interest rates has returned to haunt stock markets. With the Fed going to war against inflation, traders are worried the era of easy money is coming to an end. As a result, volatility has gone through the roof and valuation multiples have compressed, decimating the most ‘bubbly’ pockets of the market. The turbulence is likely to continue, but with the economy still in good shape and buybacks going strong, this storm could ultimately be a gift to investors with long time horizons.

Fed giveth, Fed taketh away

Funny as it sounds, the pandemic turned out to be a blessing for equity markets. Governments and central banks joined forces to fight the crisis, and when extravagant fiscal spending is combined with rock bottom interest rates, that is rocket fuel for riskier assets.

An easy way to think about it is from a cross-asset perspective. With central banks slashing rates and buying truckloads of government bonds, the yields on those bonds crumble and investors searching for juicy returns have to look elsewhere. That pushes money managers to take on more risk in the stock market, pushing valuations higher.

Now this process is going into reverse. Spiraling inflation has changed the game, sending central banks scrambling to raise interest rates to combat inflationary pressures. And with most economies healing so quickly, governments have started to roll back their own spending to control debt levels.

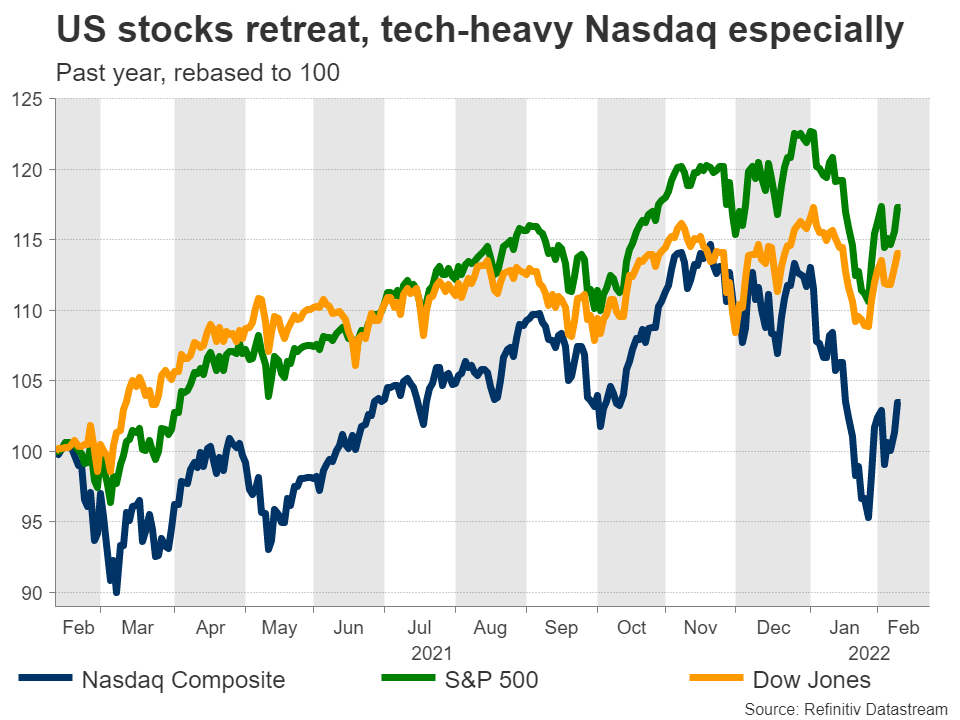

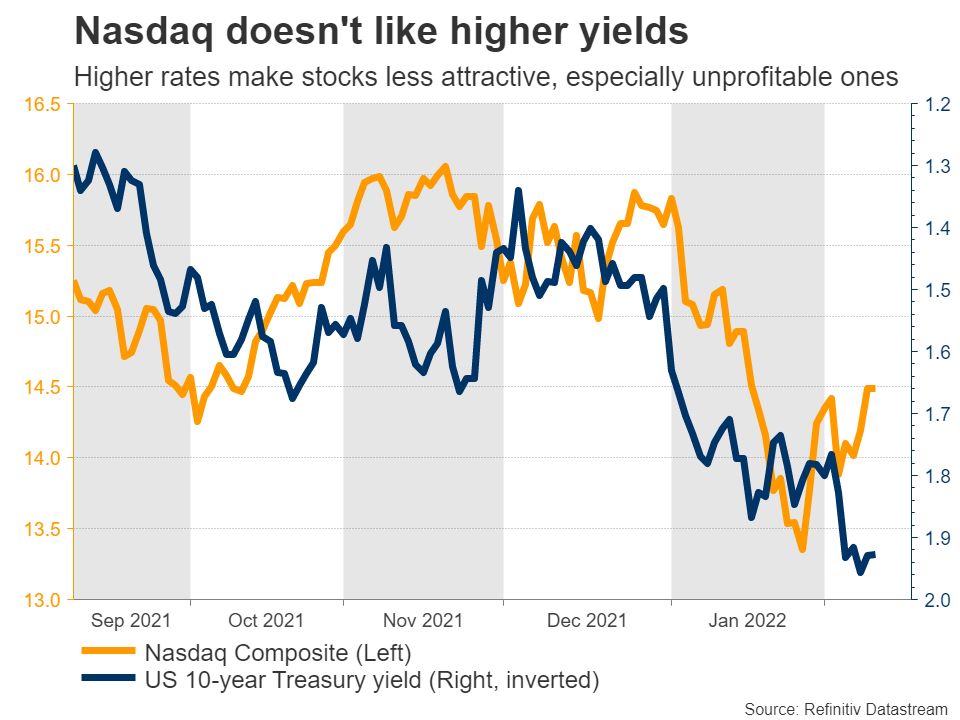

Consequently, markets suffered a sharp selloff. Tech and ‘growth’ stocks have been the biggest casualties, as higher rates generally inflict more damage on shares of companies that are unprofitable or barely profitable. Anything with an expensive valuation has essentially been taken to the cleaners.

The good news

On the bright side, there are several reasons to be optimistic here. First and foremost, the global economy is quite strong. What we’ve seen lately wasn’t a reaction to shifting economic fundamentals but rather traders pricing in tighter monetary policy, precisely because most economies are strong enough to handle that.

In fact, investors may have gone too far already. Money markets are currently pricing in six rate increases by the Fed this year, which is probably on the optimistic side of what is possible. There’s a real possibility the yearly US inflation rate will peak soon as government spending fades, supply chains finally begin to normalize, and tougher year-over-year comparisons kick in from March onwards.

When investors see the first signs of ‘peak inflation’, these ultra-aggressive Fed bets could be dialed back, pushing yields back down and breathing new life into equity markets. Politics point to a similar conclusion. The Democrats will probably lose Congress in November’s midterm elections, which means there won’t be any tax increases over the next couple of years.

Another encouraging sign is that many of the ‘excesses’ in the market have been washed out. Companies trading at crazy valuation multiples have been demolished and a sense of sobriety has returned. Just look at pandemic winners like Zoom that have seen their shares retreat 70% from record highs. It’s a similar story for meme stocks, blank-cheque companies (SPACs), and even some quality businesses like Netflix and Facebook.

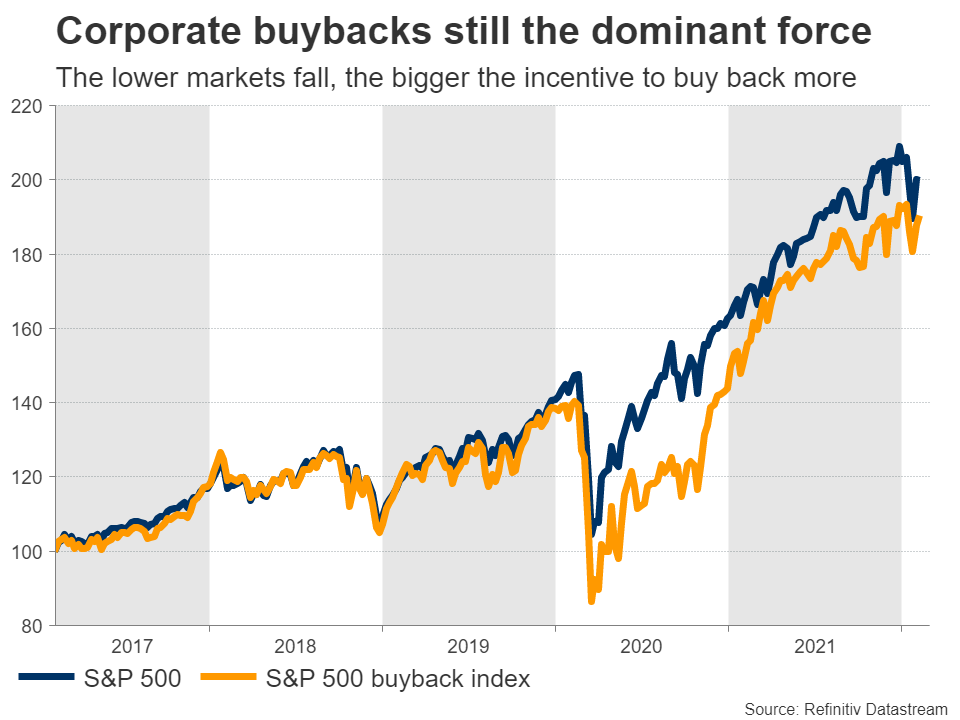

Finally, let’s not forget about buybacks. Companies bought back their own stock at a record pace in 2021, essentially reducing the total number of shares available and improving earnings per share, a process that ultimately pushes prices higher. With most stocks now trading at a discount relative to last year, corporate treasuries could accelerate this process, providing a powerful and consistent source of demand.

The bad news

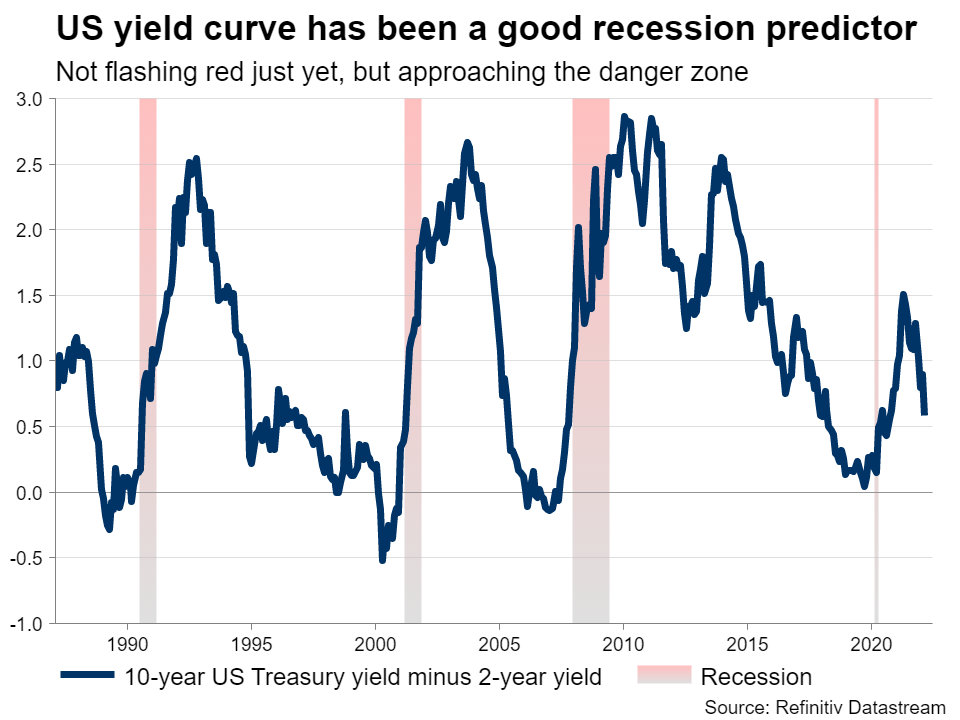

Of course to provide a holistic view, we have to outline the bear case as well. The biggest downside risk is that inflation remains persistently high even after supply chains normalize, forcing central banks to raise rates with even greater force. That would propel yields higher and put the risk of a policy-induced recession on the map.

The other primary risk is that economic growth just grinds to a halt now that the fiscal juice is running out, again putting investors on recession watch, although in that case the Fed would also back off from aggressive rate hikes, negating some of the negative impact.

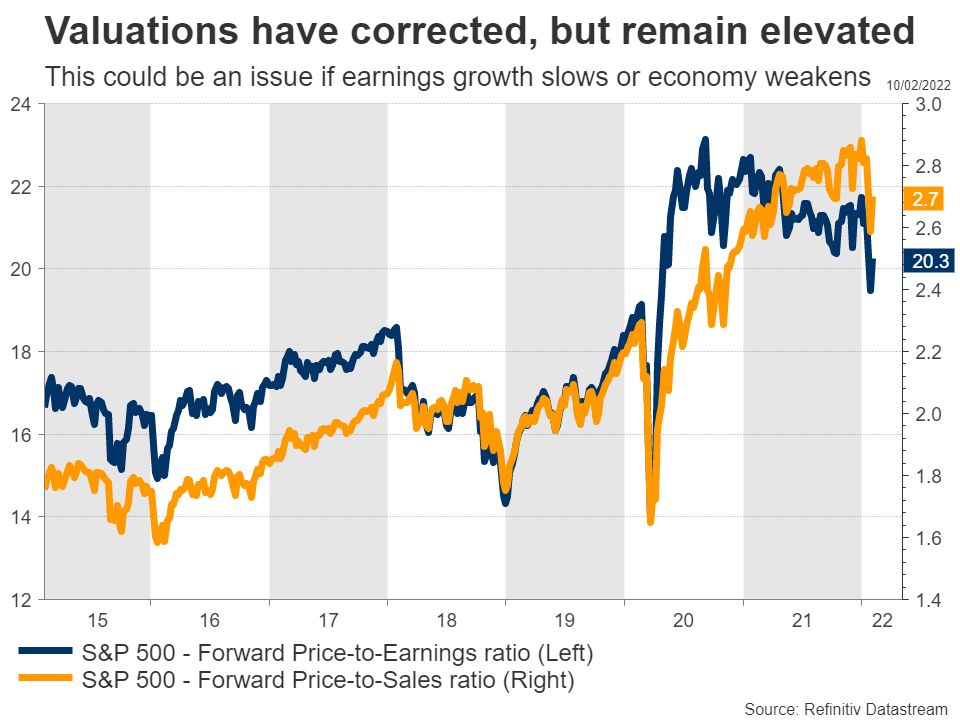

Earnings growth could be another troublespot. While earnings are still growing at a healthy clip, the percentage of companies beating analyst estimates has declined in this reporting season and those that beat do so with a smaller margin. This could be a problem when combined with valuations that are still historically ‘expensive’.

Geopolitics are back on the radar too with the tensions around Ukraine and Taiwan, although markets generally don’t care much about that as long as it’s just political muscle flexing.

The big picture

All told, markets are going through a painful readjustment period as central banks and governments wind down their stimulus. This implies that volatility episodes and sharp drawdowns could become a more frequent phenomenon as Wall Street learns to live without endless liquidity.

But the economy is not falling off a cliff, the amount of rate increases that have been baked into asset prices might already be excessive, and corporate buybacks will remain a dominant force that intensifies the lower the market falls, keeping a soft floor under prices.

The bottom line? Investors willing to stomach the volatility can take advantage of the violent pullbacks to scale into positions for the long term, preferably in high quality companies trading at a discount.

Markets will kick and scream before taking their medicine but as long as a recession is not imminent, they can probably handle slightly higher rates without breaking down. After all, there is still no real alternative.

{kind=link}