The week is loaded with US economic data releases, most of which are scheduled for Friday. There has been a shift in the trading dynamics governing the dollar lately, with strong data being unable to boost the reserve currency. If this pattern continues, it would be another sign the overall trend is exhausted.

Dollar refuses to obey

Let’s start with the good news – the US economy is in good shape. The jobs market is approaching full employment, consumers continue to spend with confidence, and inflationary pressures have intensified.

As such, markets have priced in six rate increases by the Fed for this year, betting that the central bank will be forced to slam on the brakes to bring inflation under control. But despite these huge moves in bond markets, the dollar remains flat for the year. Even fears of armed conflict in Ukraine couldn’t boost the reserve currency for long.

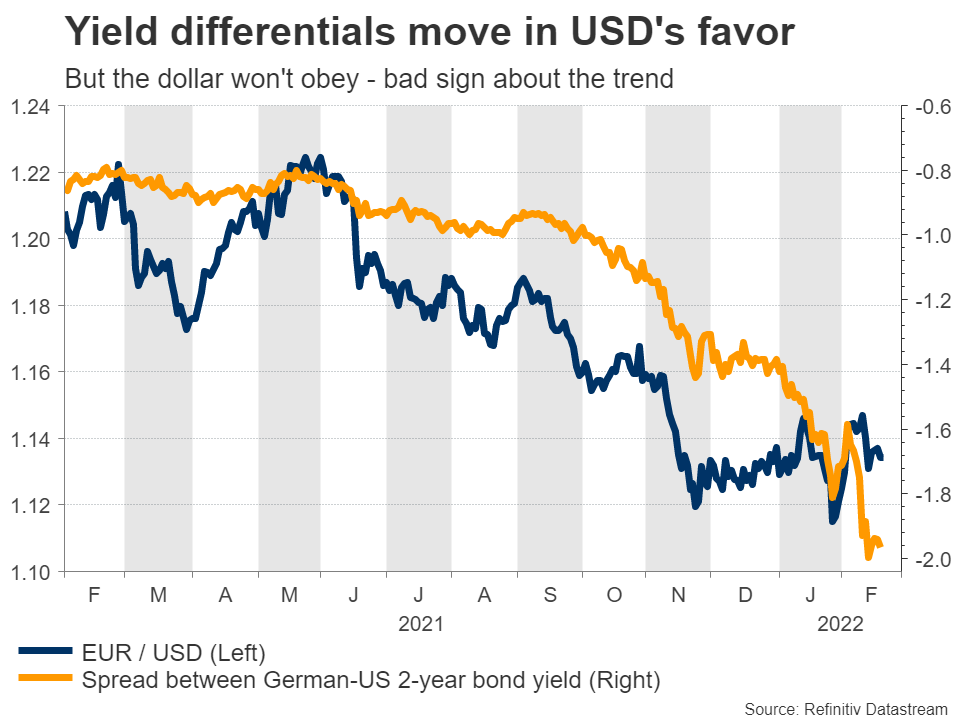

This sluggish behavior has been on full display lately as the greenback has been unable to capitalize on positive surprises in important US economic indicators. A stellar jobs report, another scorching hot inflation number and a massive beat in retail sales over the past few weeks did not have the impact someone would expect – the dollar barely rose in the aftermath or even fell.

When a currency cannot rally on good news, that’s an ominous sign. It suggests the uptrend is running out of steam.

Another round of data

Now the question is, will the dollar continue to behave this way? We’ll get the answer after the next batch of economic data. The show will get started on Tuesday with the Markit PMIs for February. Then on Thursday, the spotlight will fall on the second estimate of GDP for Q4 and a parade of Fed speakers.

But the main event is on Friday, when the core PCE price index is released. This is the Fed’s favorite inflation measure and it will be accompanied by consumption data and durable goods orders, all for January. Most of these indicators are forecast to have improved from the previous reading.

Admittedly these indicators are a little ‘outdated’ by now, but nevertheless, it will be interesting to see how the dollar reacts to any surprises.

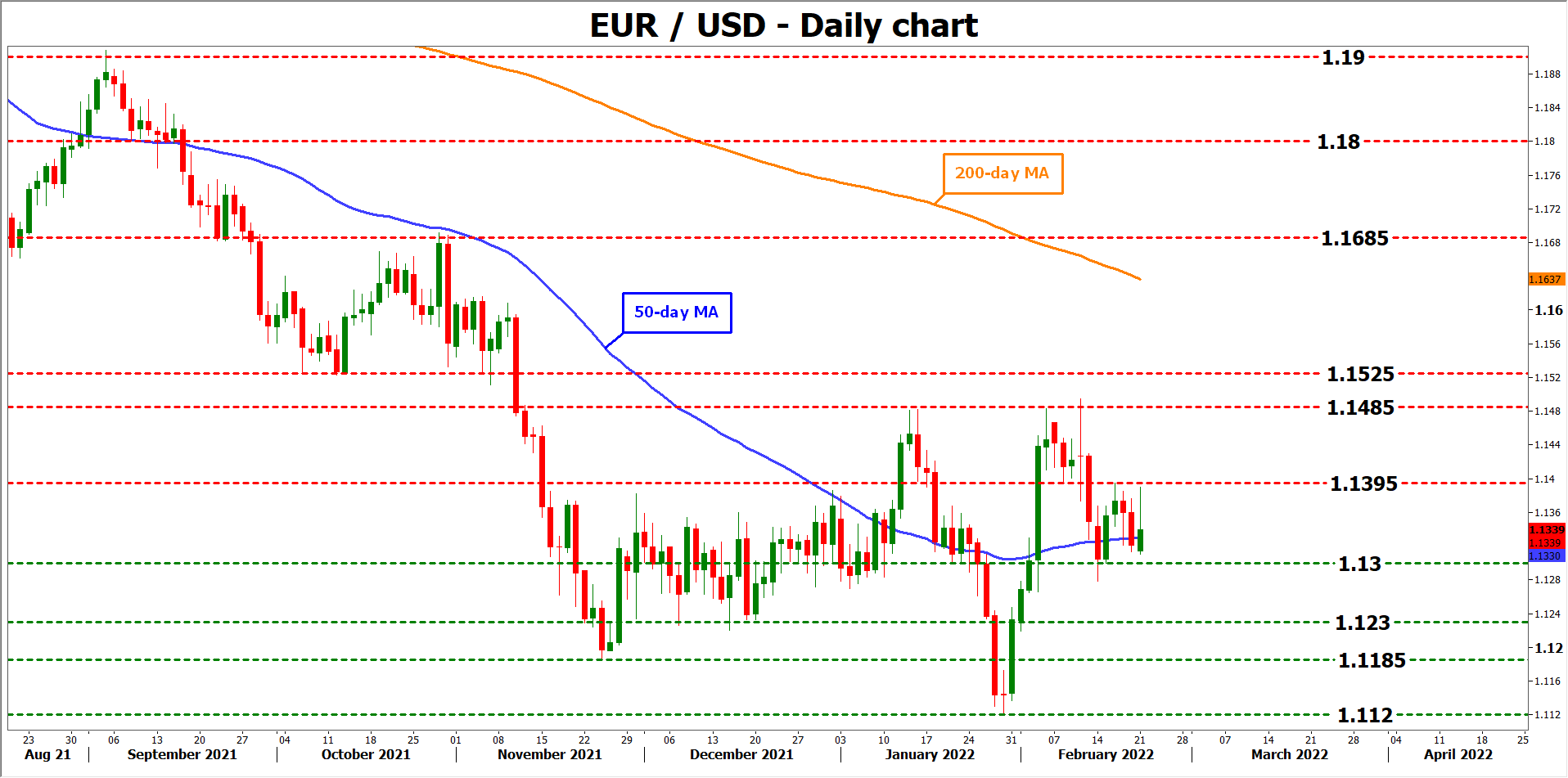

Taking a closer look at euro/dollar, the pair has been trapped in a narrow range between 1.1395 and 1.1300 for a week now, and a break on either side is needed to give traders a clearer sense of direction.

Dollar outlook

Overall, the dollar’s performance has been rather disappointing. The stars have aligned this year with geopolitical tensions, volatility in stock markets, and traders betting aggressively on Fed rate increases – yet the greenback has nothing to show for it.

Of course, we cannot analyze the dollar in a vacuum. Much of this lackluster performance boils down to the euro, which came back to life after the European Central Bank signaled that rate increases are on the menu for this year.

Still, the dollar’s future doesn’t seem very bright here. Traders may have gone too far already with Fed bets and when inflation finally peaks, some of those bets could be dialed back. That might happen relatively soon as government spending is fading, supply chains have started to correct, and the year-over-year comparisons in inflation will become tougher after March.

Politics argue the same point. The Democrats will probably lose Congress later this year, which means the days of generous government spending are over. Combined with the Fed raising rates, economic growth will likely slow. All this suggests the dollar’s rally might be on its final legs.

The main risk to this view? Inflation remains persistently high, forcing the Fed to tighten even more aggressively. But that could also backfire, by raising the risk of a policy-induced recession.

Either way, it’s just difficult to see a ton of upside for the dollar from here, with the Fed already priced so generously.

{kind=link}