The Eurozone will update its CPI inflation and GDP growth readings on Friday at 09:00 GMT. While investors expect a firmer economic expansion and another upturn in inflation, the data could produce only temporary volatility as the war in Ukraine will remain the major, if not, the only driver for the battered euro in the short term.

Euro may shrug off new record inflation

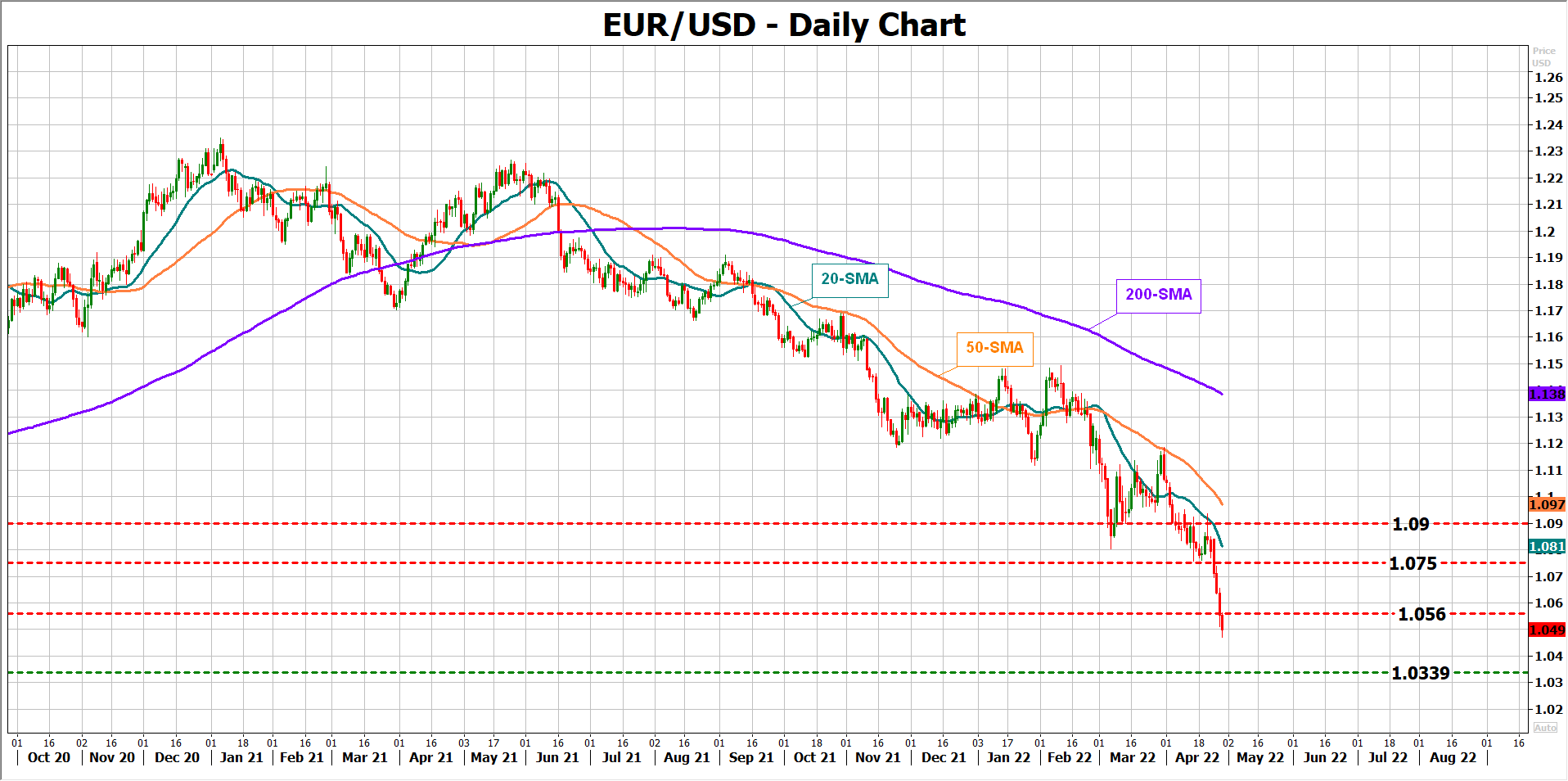

The euro has been hammered badly this week, depreciating by more than 2.0% against the US dollar in the face of hawkish Fed rate hike talk and Russia’s gas supply cuts to NATO members Poland and Bulgaria. That is the largest damage since March 2020, but the week is not over yet and the common currency may have one more opportunity to rebound before the focus solely turns to the 2017 trough of 1.0339 as Friday’s preliminary CPI inflation and GDP growth data appear on the radar.

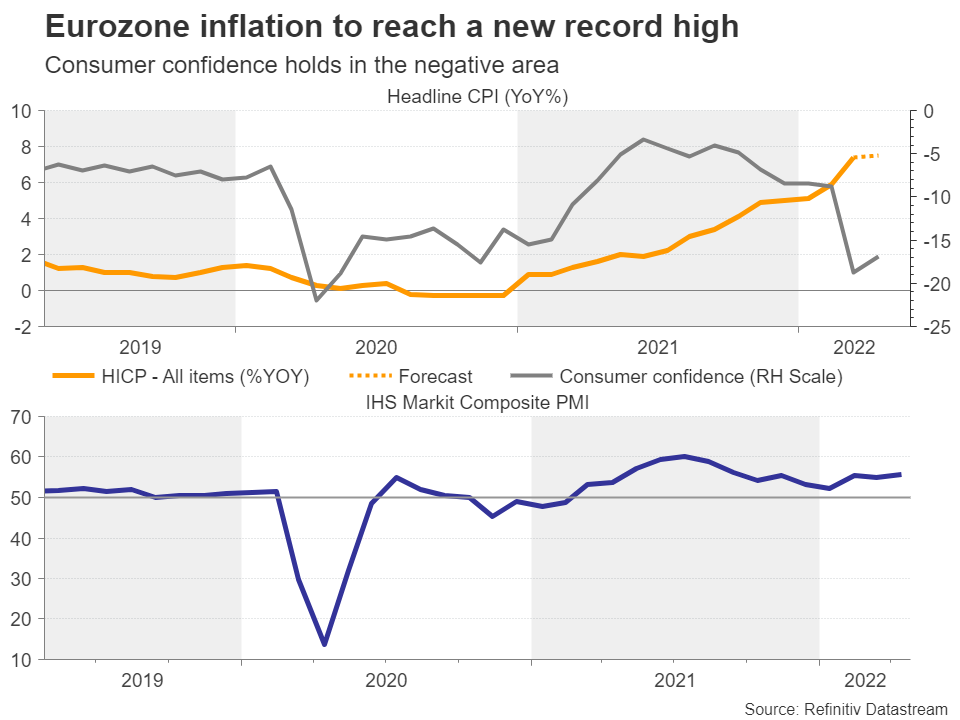

Looking first at CPI readings, there is growing speculation that global inflation is nearing a peak, as year-on-year comparisons with 2021 high levels could produce softer CPI figures. The ECB’s vice president Luis de Guindos reaffirmed his hopes for a peak in inflation today, though the forecasts for the Eurozone flash estimates for April suggest this phenomenon may arise at a later stage, as they point to a new record high of 7.5% y/y from 7.4% previously. Excluding volatile food and energy prices, the core measure is also projected to run beyond the central bank’s symmetrical 2.0% target, unlocking a fresh high at 3.4% y/y, up from 3.2% in March.

The above outcome or even a stronger-than-expected print could amplify calls for a July 25bps rate hike, which is currently almost fully priced in futures markets. However, whether the inflation data will provide the much-needed upturn in the euro remains to be seen.

Under normal circumstances, a continuous inflation spiral would raise the stakes for tighter monetary policy, stirring fresh bullish volatility in the currency as in the greenback’s case. That said, another record CPI mark in the Eurozone may not be very surprising to investors after all. Stronger-than-expected German CPI figures have already foreshadowed this scenario. Also, the war in Ukraine and lately Russia’s gas supply cuts could add more fuel to the already rocketing energy and food crisis in the coming months.

GDP growth may not help the euro either

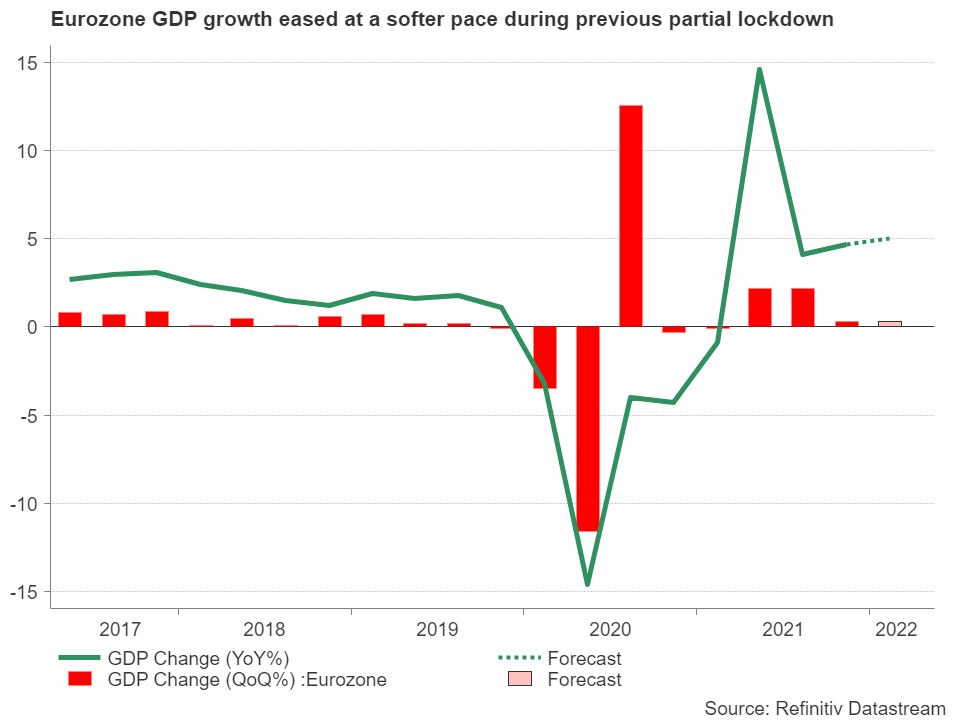

Perhaps, the euro could recoup some lost ground if a potential upbeat inflation report is accompanied by firmer GDP stats. Analysts believe that the Eurozone economy has expanded at a faster annual pace of 5.0% y/y in Q1 versus 4.6% reported in the preceding quarter, and at a steady quarterly rate of 0.3%. Nevertheless, investors could again barely react to the data since Ukraine’s negative economic spillovers may become more evident in the next GDP releases.

Perhaps a sudden pullback in the US core PCE inflation index could give a second chance to euro bulls later on Friday, increasing the likelihood of a narrowing monetary divergence between the Fed and the ECB. But again, given the non-existing support from the recent negative US GDP print, as well as the short-lived impact from the ECB’s recent hawkish rate hike comments, it’s hard to see what can come to the euro’s rescue if not a ceasefire in Russia-Ukraine geopolitical tensions.

EUR/USD

From a technical perspective, the devastating loss in euro/dollar has opened the door for the 2017 trough of 1.0335 but traders may wait for a close below 1.0500 before they engage in additional selling activities. Beneath the crucial 1.0339 threshold, the pair will re-activate the 2008 downtrend, bringing the scenario of parity back into scope after two decades.

In the event of an upside reversal, there is a nearby resistance at 1.056, which the pair needs to claim to continue towards the 1.0750 – 1.0800 region. The 1.0900 round level could be the next obstacle and perhaps the green light for an acceleration towards 1.1045.

{kind=link}