Summary

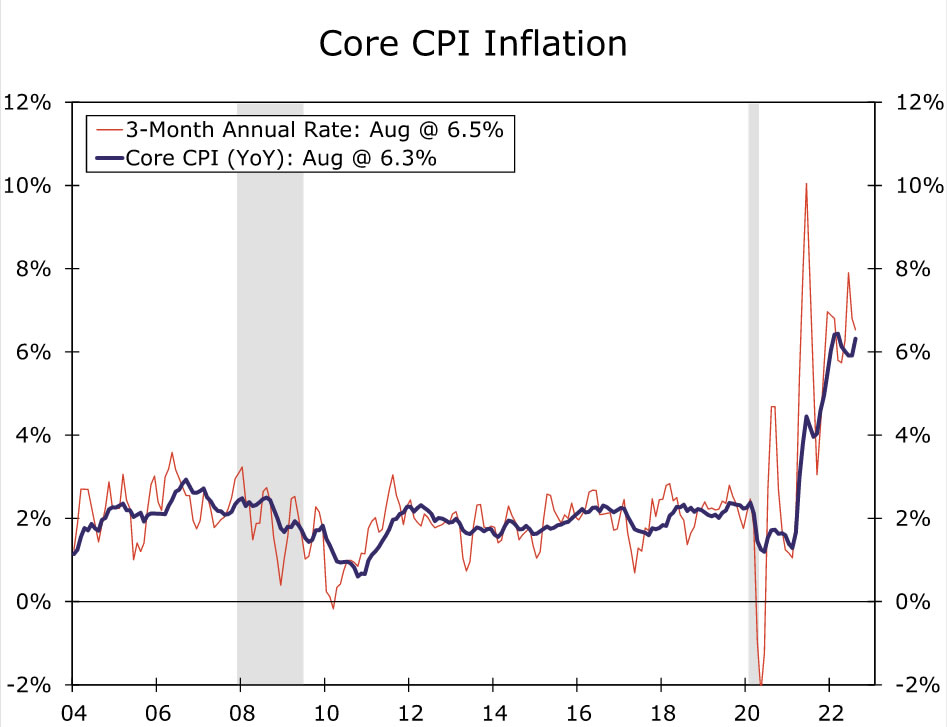

Another super-sized 75 bps rate hike at next week’s FOMC meetings seems all but assured. Employment growth has been robust over the past two months, averaging 421K new jobs in July and August. Headline inflation has been relatively tame over the same period, but falling gasoline prices have accounted for the bulk of the weakness. Excluding food and energy, core inflation has remained far too high for the Fed’s liking. Over the past three months, core inflation has risen at a 6.5% annualized rate, more than triple the central bank’s 2% target.

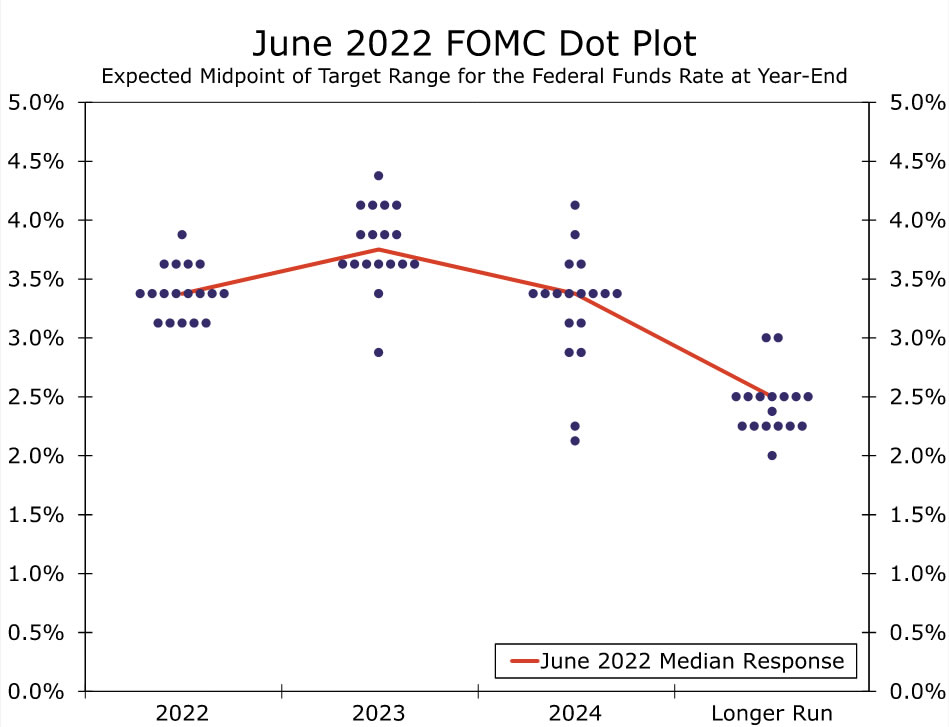

Next week’s meeting will also include an update to the FOMC’s Summary of Economic Projections (SEP). We expect the 2022 median projection for the federal funds rate to be 3.875%, up from 3.375% in the June SEP. We think the 2023 median dot probably will be above the 2022 dot, but only modestly so. Despite the hawkish rhetoric, few Fed officials have publicly advocated for a peak federal funds rate that is well above 4%. Our expectation is that the median projection for the 2023 fed funds rate will be 4.175%. For 2024 and 2025, we think the dots will show a steady easing of policy as inflation moves back to 2%. We expect the changes to the SEP inflation projections will be relatively modest, but weaker GDP growth and higher unemployment projections for 2023 seem likely in our view.

At some point, Chair Powell and his FOMC colleagues will feel confident enough that they can slow the pace of monetary policy tightening. With the federal funds rate soon to be above 3% for the first time in 15 years and with QT running at full speed, monetary policy is rapidly moving towards restrictive territory. That said, we do not think the FOMC is ready to slow the pace of tightening yet, let alone reverse course. Chair Powell’s speech at Jackson Hole made clear that the Federal Reserve views its fight against inflation as far from finished. We expect a similar message to come through in the post-meeting press conference next week.

The FOMC to Keep Rolling with Another 75 Bps Hike in September

Unrelenting inflation along with a boiling hot jobs market led the FOMC to deliver its second-straight 75 bps rate hike at its most recent meeting in late July. The decision for another jumbo move—the likes of which prior to June had not been seen since 1994—came despite signs of economic activity beginning to soften. With 225 bps of tightening delivered over just four meetings and indications that spending and investment are wobbling, Chair Powell noted in July’s post-meeting press conference that at some point it will become appropriate to slow the pace of rate increases. Deciding when exactly to ease up on the brakes, however, depends on incoming data. Not only does the FOMC want to assess the cumulative affects of tightening to date, but, in our view, it wants to move away from meeting-specific guidance given the fast pace at which the inflation and broader economic backdrop continue to evolve.

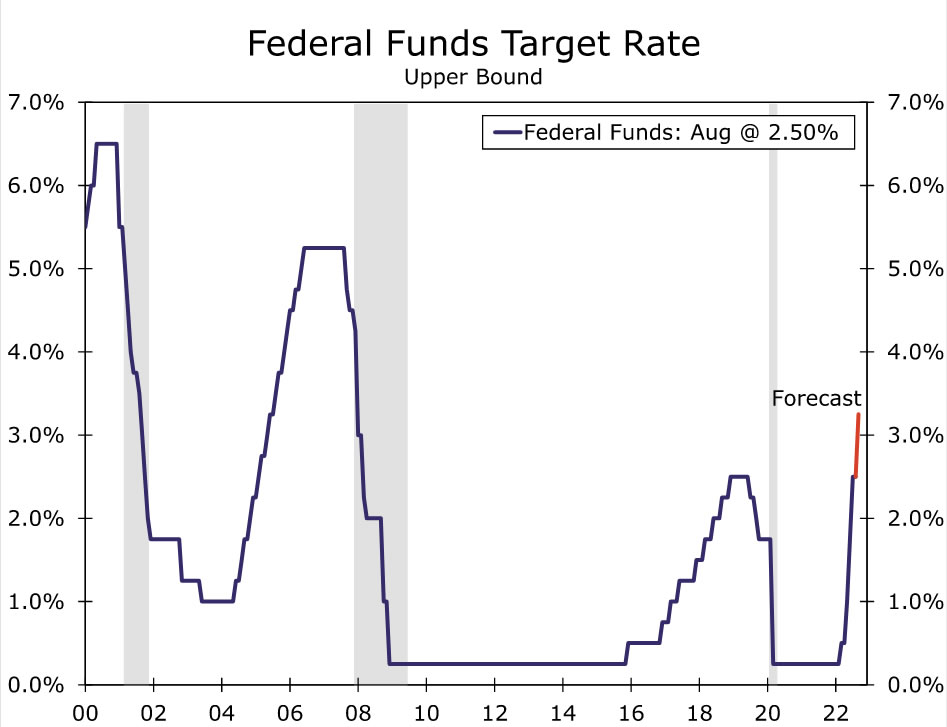

While FOMC officials have been playing their next move closer to the chest, the time to start slowing rate increases does not appear to be in hand just yet. We expect the FOMC to raise the fed funds rate by another 75 bps in September, bringing the target range to 3.00-3.25%. If realized, this move would put the federal funds rate at its highest level in 15 years (Figure 1). Consumer spending remains under pressure from inflation but thus far has not buckled. Similarly, industrial activity has shown signs of stabilizing relative to a couple of months ago when growth in industrial production essentially stalled.

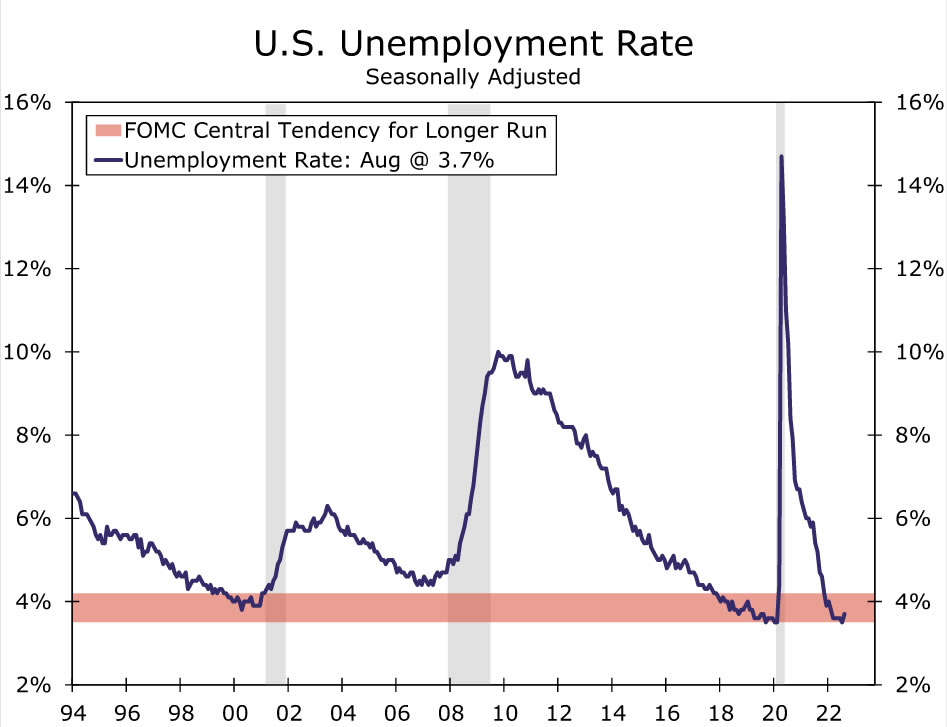

More importantly for the FOMC, the labor market remains exceptionally strong. Employment growth cooled slightly over the inter-meeting period, but the labor market is still incredibly tight. Hiring in August followed up July’s blockbuster print with a gain of 315K jobs, robust in its own right. The unemployment rate moved up to 3.7%, but the increase was due to an encouraging rise in labor force participation rather than an increase in layoffs. At just 3.7%, the unemployment rate remains near the low end of what Fed officials agree is sustainable over the long run (Figure 2). Job openings, hiring plans and businesses reporting at least one job hard to fill have softened since the Fed’s past meeting, but only minimally. All told, tightness in the labor market eased only incrementally since the previous FOMC meeting.

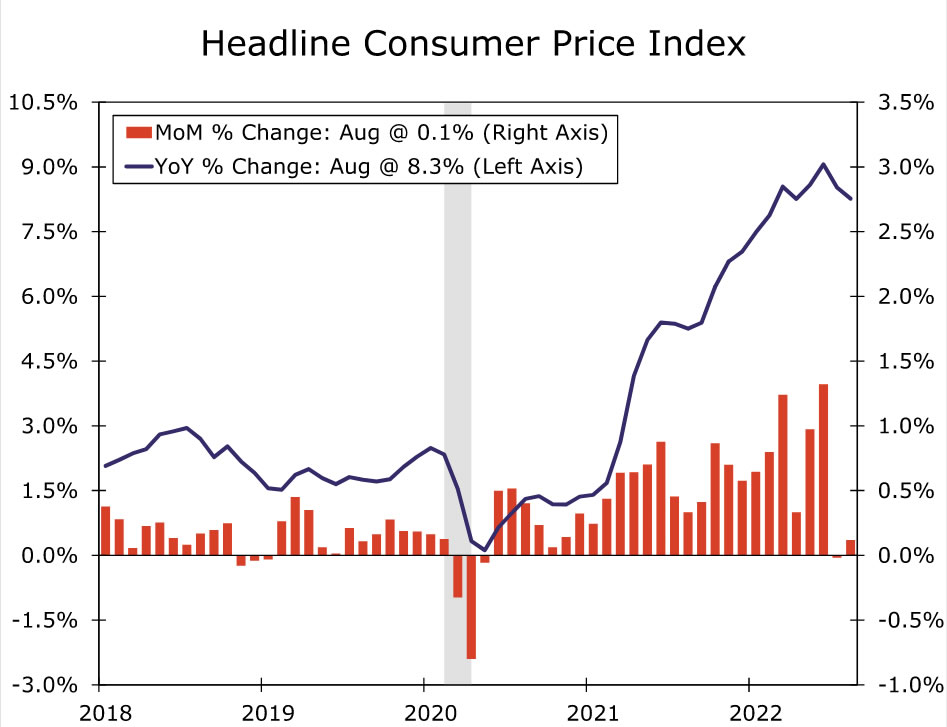

Headline inflation has been relatively benign over the past two months. The overall CPI was flat in July relative to the previous month and increased just 0.1% in August (Figure 3) Chair Powell has stated that he would like to see “compelling evidence that inflation is moving down,” and the two past two CPI prints would seem to offer some preliminary evidence. But, with a drop in gasoline prices driving much of the recent softness, a sustained return to 2% inflation remains far from assured. Core inflation has not eased nearly as much as headline inflation and is still advancing well-ahead of the Fed target. The August CPI report showed core inflation registered a 6.5% annualized pace over the past three months (Figure 4).

While some recent slowing in price growth is a step in the right direction, it comes at a time when FOMC members sound more resolute in their efforts to return inflation to 2% for the long haul. In a pointed speech at the Kansas City Fed’s annual symposium at Jackson Hole, Chair Powell made clear that the FOMC is laser-focused on restoring price stability. Chair Powell and other members appear wary of easing up prematurely, citing historical comparisons to the 1970s and coalescing around the view that policy will need to be restrictive for some time. The steady string of tough talk on inflation continued even after the August jobs report showed slight cooling in the labor market and estimates rolled in that consumer price growth was tame in August. Financial market participants have taken notice: at present, the market is fully priced for a 75 bps rate hike at the September FOMC meeting.

September’s increase in the fed funds rate will be complimented by the reduction in the Fed’s balance sheet hitting its full stride. Starting this month, up to $60 billion each month of maturing Treasury securities will roll off the balance sheet, a doubling from the June-August pace of $30 billion per month. The cap on mortgage-backed securities paydowns also has doubled to $35 billion per month, although by our estimates paydowns are expected to run well below this cap for the foreseeable future since mortgage demand has slowed to trickle in recent months amid higher rates.1

Smaller Yet Meaningful Changes Likely Coming in the New SEP

The FOMC updates its Summary of Economic Projections (SEP) four times a year: March, June, September and December. The past few updates have contained sizable revisions to the outlook for economic growth, inflation and the federal funds rate amid a rapidly evolving economic landscape. Next week’s update will once again include some revisions, but we expect them to be more modest than the ones that occurred in March and June.

In our view, the biggest changes to the FOMC’s projections for the federal funds rate (i.e. the dot plot) will be for 2022. In June, the median participant projection for the 2022 year-end fed funds rate was 3.375% (Figure 5). If the FOMC hikes by 75bps next week as we expect, that would put the midpoint of the fed funds target range at 3.125% with two meetings still to go this year. We think the 2022 median dot will move up to 3.875% to reflect a more aggressive path of tightening.

As discussed earlier, Fed officials have made clear in their public comments that monetary policy easing remains a long way off. Thus, from a signaling standpoint, we think the 2023 median dot probably will be above the 2022 dot, but only modestly so. Despite the hawkish rhetoric, few Fed officials have publicly advocated for a peak federal funds rate that is well above 4%. Our expectation is that the median projection for the 2023 fed funds rate will be 4.125%. For 2024 and 2025, we think the dots will show a steady easing of policy as inflation moves back to 2% and the Committee responds accordingly by gradually moving the fed funds rate back towards its longer-run level of 2.5%.

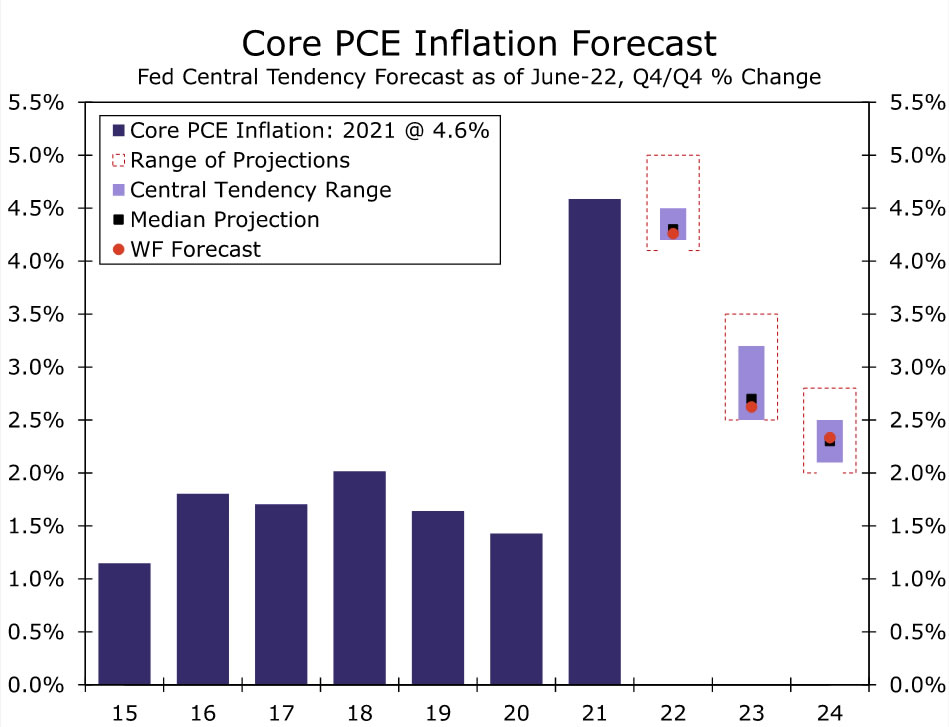

In the June SEP, the median FOMC participant looked for PCE inflation to be 5.2% in 2022 and 2.6% in 2023. Our most recent forecast, published on September 9, is roughly in line with these projections. We look for inflation as measured by the PCE deflator to be 5.1% and 2.3% in 2022 and 2023, respectively. Similarly, the median FOMC projection in the June SEP for the core PCE deflator was 4.3% in 2022 and 2.7% in 2023, and our latest forecast looks for a comparable 4.3% in 2022 and 2.6% in 2023 (Figure 6). Tweaks may be coming, but we do not expect sweeping changes to the inflation outlook in the updated September SEP.

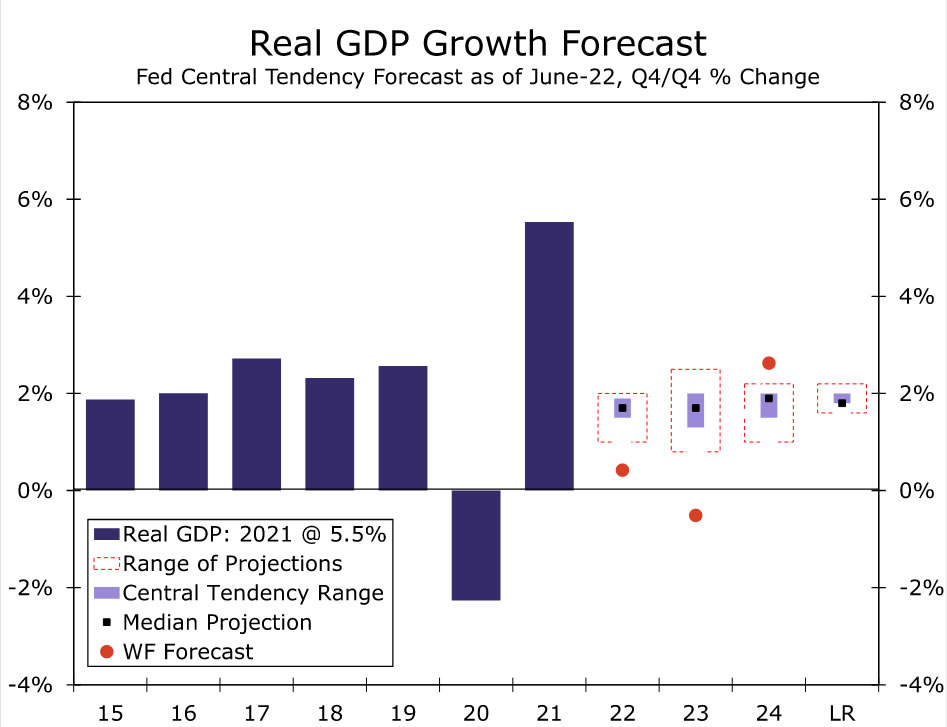

The FOMC’s projections for economic growth in 2022 likely will come down, reflecting the two consecutive quarters of negative real GDP registered in the first half of this year. Our own estimate is for GDP to register just a 0.4% year-over-year rise in Q4, well below the 1.7% median estimate in the June SEP (Figure 7). The 2023 estimates for GDP growth and unemployment should be more telling of how bumpy the FOMC sees the road to bringing down inflation. In June, the median 2023 estimate for GDP growth (1.7%) was only a hair below the Committee’s estimate for the economy’s long run trend growth rate (1.8%).

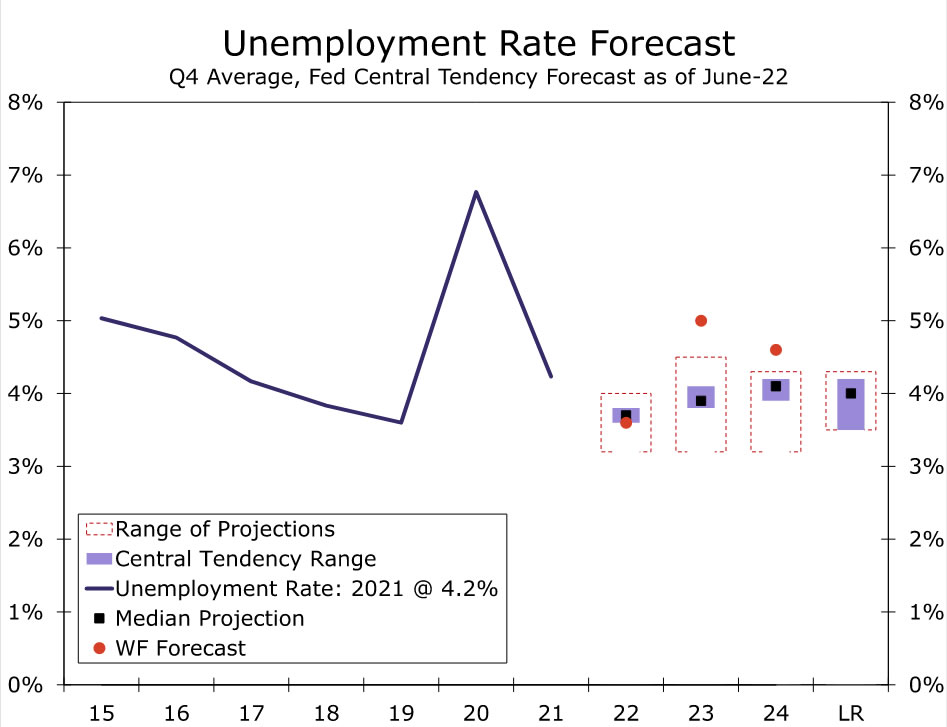

We would not be surprised to see the 2023 growth projection decline further as the FOMC signals a more restrictive stance of policy will be needed to bring down inflation. Similarly, we expect the median estimate for the unemployment rate at the end of 2023 to move up (Figure 8). While we do not believe the SEP will signal that a recession is likely to ensue from the prolonged stance of more restrictive policy, as our own forecast suggests, we expect it paint a more realistic portrait in that restoring price stability will impart a meaningful hit to economic growth and the jobs market.

It remains to be seen whether next week will mark the final 75 bps rate hike of the tightening cycle. For essentially the entire year, the FOMC has been increasingly hawkish at each successive Committee meeting in response to alarmingly fast inflation. July’s downside miss on inflation was promptly offset by an upside miss in the August CPI report, putting pressure back on the FOMC to remain diligently hawkish at next week’s meeting. But with the federal funds rate poised to be above 3% after next week’s meeting and QT running at full speed, Fed officials may finally start to feel that the pace of tightening can moderate in Q4 and beyond. That said, there is a big difference between slowing the pace of tightening and a full-blown policy pivot. Chair Powell’s speech at Jackson Hole made clear that the Federal Reserve views its fight against inflation as far from finished. We expect a similar message to come through in the post-meeting press conference next week.

{kind=link}