With the Fed trying to get on top of inflation no matter what it takes and showing no interest to come to investors’ rescue, traders will keep looking for any cracks within the US economy this week. US housing data will feature the calendar on Tuesday and Wednesday at 14:00 GMT, while the Fed’s favorite core PCE inflation report will provide extra details about consumption on Friday at 12:30 GMT. The king US dollar has proved resilient to recession risks so far, therefore it might barely react to the data.

Recession watch

The slowing US housing market is rekindling some memories from the 2007-2009 Great recession but there is some confusion about whether it’s a red flag for the economy nowadays. New home sales have been trending downwards so far this year and the August reading is expected to mark a new low at 500k from 511k previously, the lowest in six years. Pending home sales due on Wednesday could show a steeper contraction of -1.4% from -1.0% previously, remaining negative for the third consecutive month.

The period of lockdowns lifted home sales to a 13-year high, but the uptrend took a halt after the government terminated the pandemic-related subsidies and the Fed started to hike interest rates in the face of rising inflation. With the average mortgage rate for a 30-year loan jumping to 6.29% recently and big property companies raising prices by 50% in the second quarter, households are reluctant to expose their finances to more expensive loans. Of course, selling existing houses could boost profits, but buying a new property at a significantly higher interest rate would eat up those benefits.

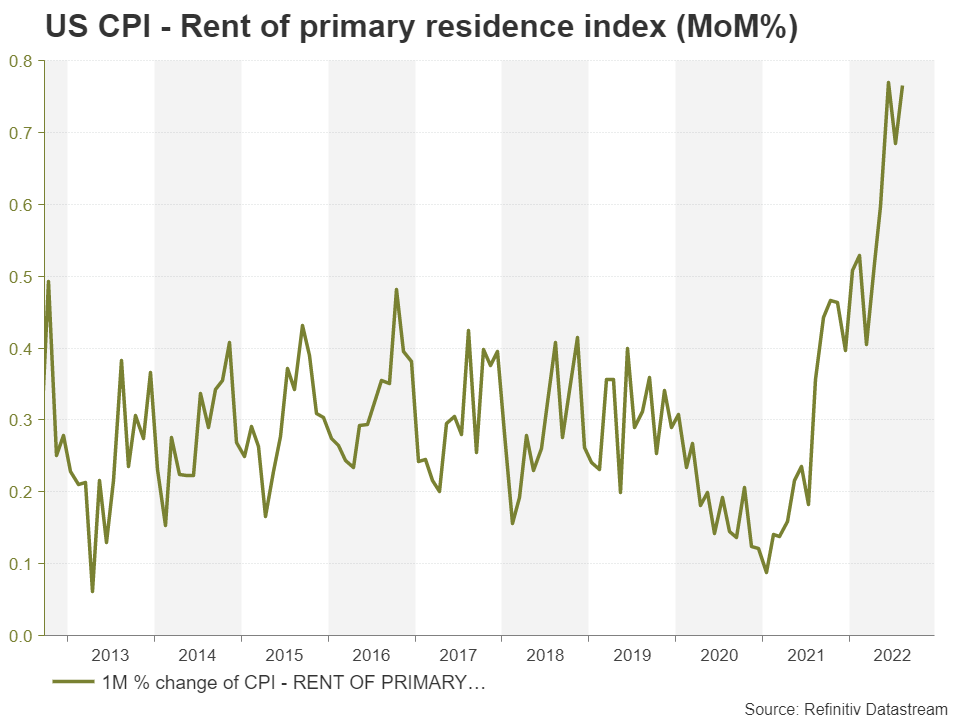

A stabilization in the red-hot rent market in August, perhaps on the back of state limits in some regions, was probably a catalyst to a softer house demand too. Though, more than half of renters are still facing elevated prices year-on-year and given the inflation in construction materials as well as the tight supply of houses, there is little prospect for a significant slowdown in the market.

Eyes on consumption

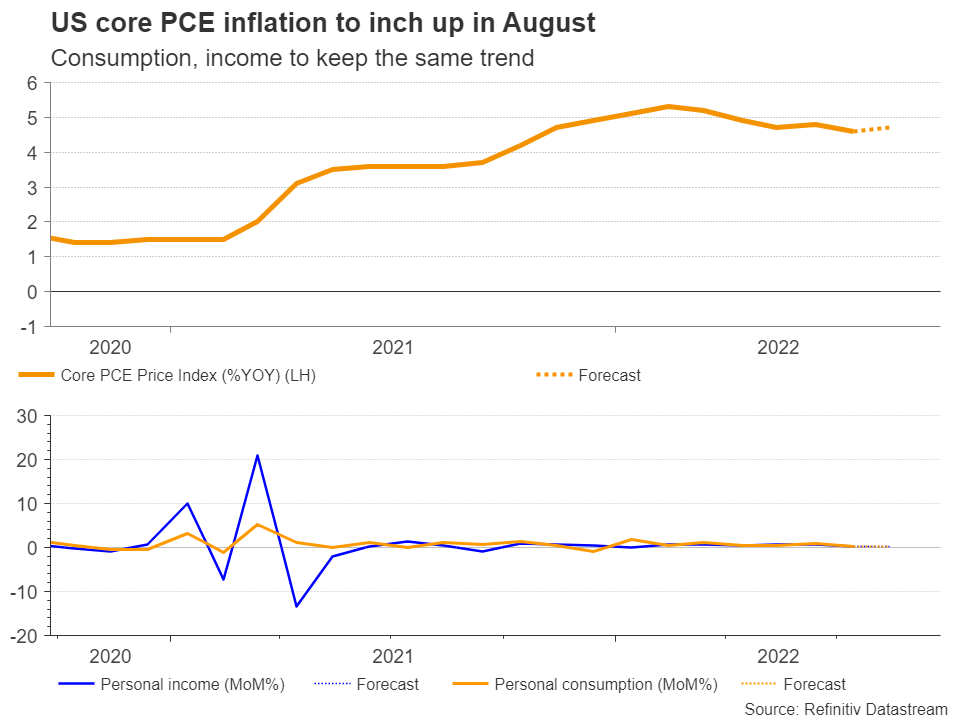

The strength in the labor market is also a tailwind for the real estate sector, delaying any defaults in loan payments. Personal income and consumption figures accompanying the core PCE inflation on Friday could provide some updates on that front. Although expectations are for a minor monthly pickup to 0.3% and 0.2% respectively, the indicators may not raise any concerns if they stay within normal levels. A potential mild increase in the core PCE inflation to 4.7% y/y would not be something new either after a similar pace in the core CPI inflation reading.

Fed comments are more important

Hence, unless a significant negative deviation from forecasts takes place, this week’s dataset may not have the power to shake the dollar. It’s obvious that monetary policy is the main player in town in global markets, therefore investors may appear more sensitive to speeches from Fed policymakers in the rest of the week, especially if comments shed more light on how big the size of future rate hikes will be. Chairman Jerome Powell, as well as Charles Evans and James Bullard will be commenting at events today, while James Bullard, Loretta Mester and John Willams will follow next later in the week.

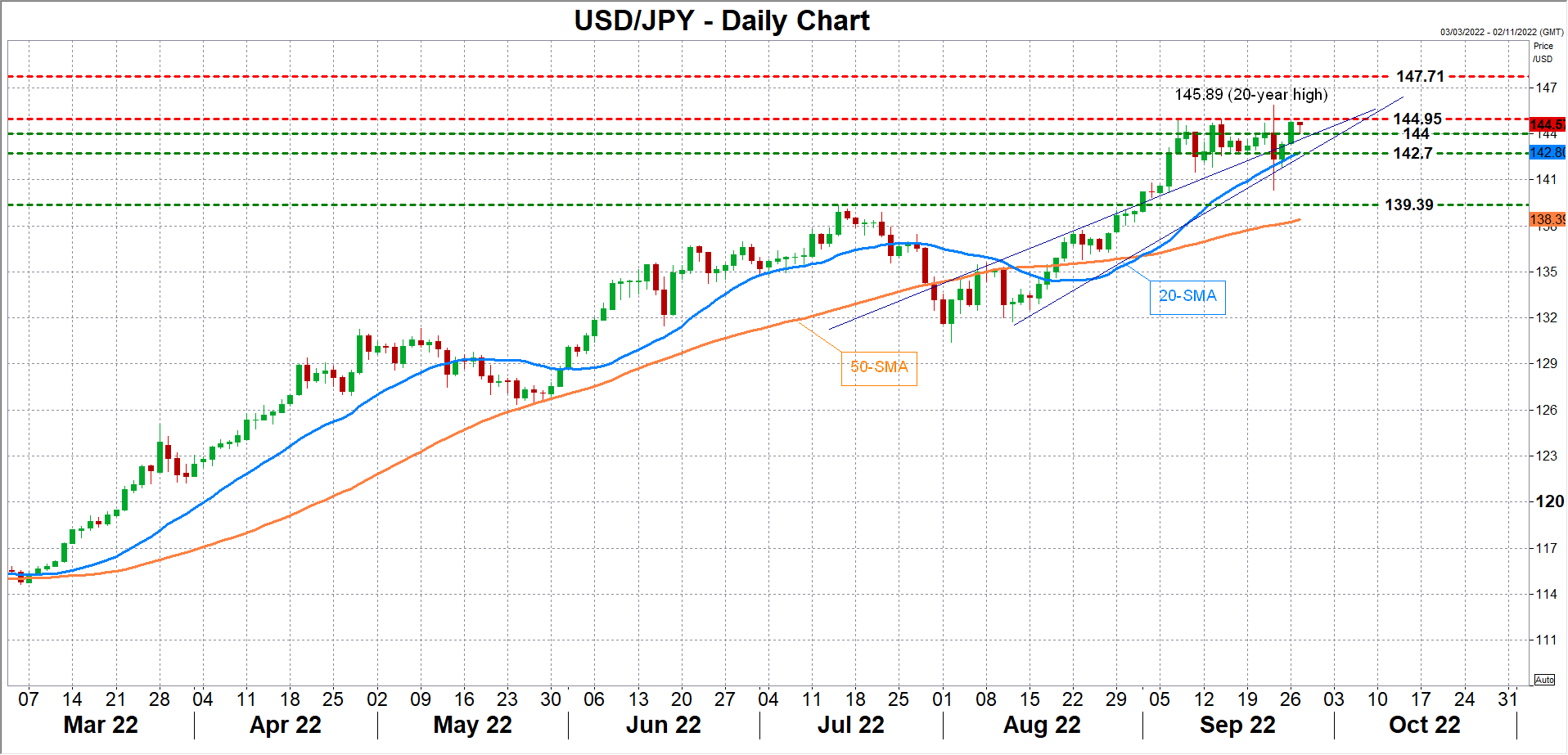

USD/JPY

Looking at charts, all eyes are back on the 144.95 ceiling in dollar/yen following the full recovery from last week’s low of 140.34. Although the continuous depreciation in other major currencies is feeding speculation for a coordinated Japan-style FX intervention against the greenback, any downfalls could be short-lived as long as the US is magnetizing investors’ interest by leading monetary tightening and through its relatively safer geopolitical and economic conditions. The Fed will need to enhance its hawkish tone if it aims to reach the 1998 peak of 147.71 this week.

Otherwise, a surprisingly conservative communication could see the pair testing the 144.00 round level ahead of the 20-day simple moving average (SMA) at 142.78. Yet, only a freefall below July’s high of 139.39 would ruin the bullish trend in the market.

{kind=link}