After another employment report pointing to further tightening in the US labor market, market participants are nearly fully convinced that the Fed will deliver its fourth consecutive 75bps hike when it meets on November 2, and that’s maybe why they kept buying dollars. However, with still three weeks until the meeting, those bets could well be tweaked and the next data having the potential to do so is the inflation numbers for September, due to be released on Thursday at 12:30 GMT.

Fed plays the hawkish drumbeat

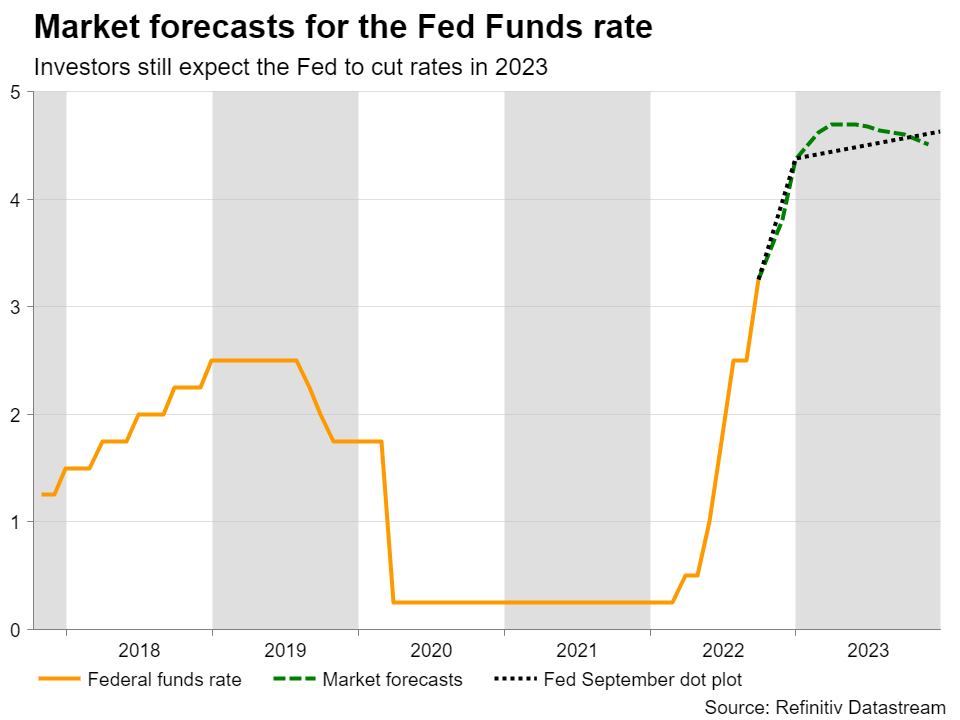

When they last met, Fed officials agreed to raise interest by 75bps for the third time in a row, appearing even more aggressive with regards to their future actions. According to their new dot plot, they were willing to take interest rates up to 4.4% this year and hit a terminal point around 4.6% next year, while they did not anticipate any rate cuts until 2024.

We will get the minutes of the gathering on Wednesday but given that several policymakers have been singing the same hawkish song in the aftermath of the meeting, the minutes may be treated as outdated and have little market impact. Investors are likely to keep their gaze locked on Thursday’s CPIs as they look for more updated information on how the Fed may proceed from here onwards.

Inflation may be stickier than it looks

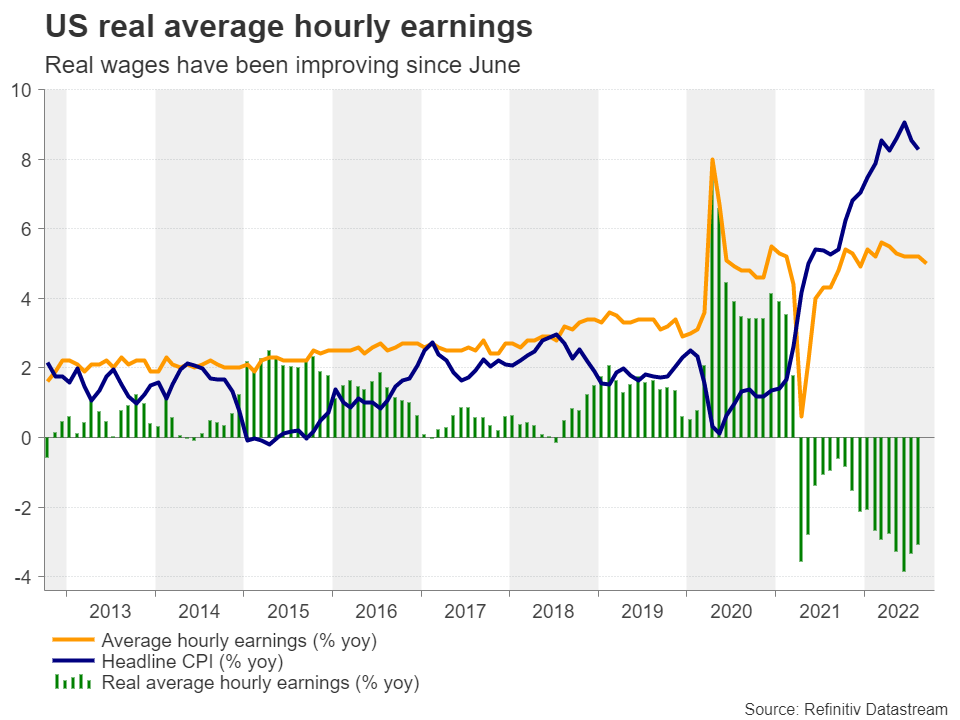

Despite the US economy contracting during the first half of the year, Fed officials have been constantly arguing that due to a very strong labor market, this doesn’t constitute a recession yet. That placed even more emphasis on the labor market, with market participants adding to their rate-hike bets every time the data is pointing to further employment gains. Last Friday, nonfarm payrolls, though slowing, increased at a decent pace and the unemployment rate fell to its five-decade low of 3.5%. Earnings slowed somewhat, but with headline inflation slowing more, real earnings have been on a steady improvement since June.

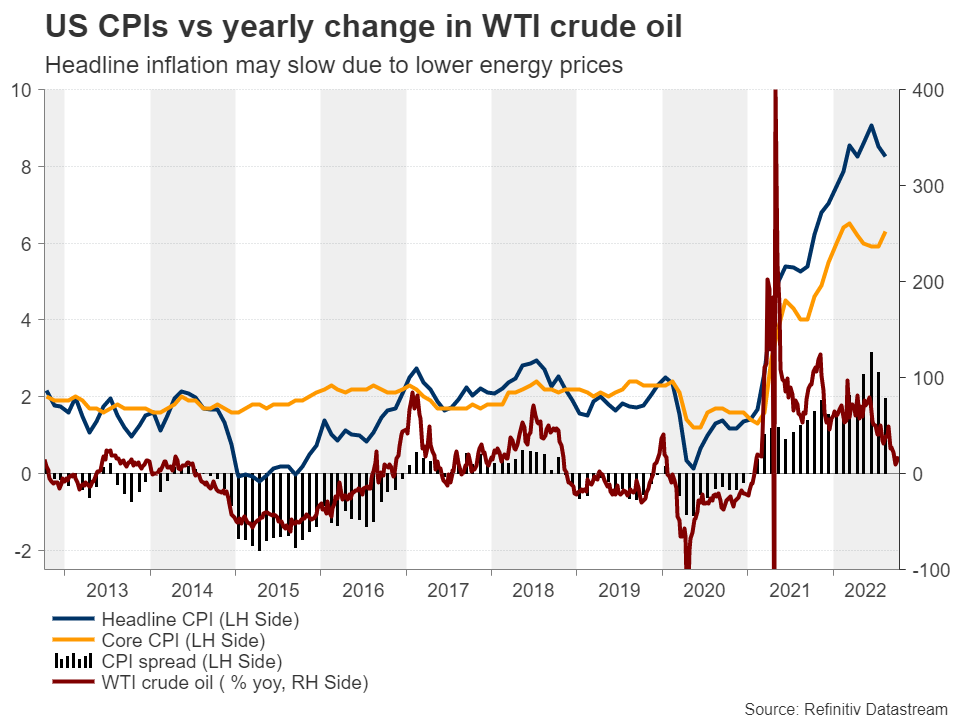

On Thursday, the headline CPI rate is expected to have slid further – to 8.1% year-on-year from the previous month’s 8.3%, but the core is anticipated to have risen to 6.5% from 6.3%. Such a development would imply that the slide in the headline rate is only due to lower prices in items like food and energy and that inflation has become stickier compared to a few months ago. Oil prices have also rebounded from their lows lately following the OPEC+ decision, which could keep headline inflation supported in coming months. Overall, such numbers would probably do very little to revive speculation that the Fed may soon need to slow down its tightening efforts.

According to the Fed funds futures, market participants are assigning a 92% probability for another 75bps hike at the upcoming Fed gathering and they see a terminal rate at around 4.7 in March, which is slightly higher than the Fed’s projections. However, they still see rates 20bps lower by November. Therefore, accelerating underlying inflation could seal the deal for another triple hike, while an upside surprise could prompt participants to price out some of the basis points that they expect to be cut next year.

Dollar to keep flapping its wings

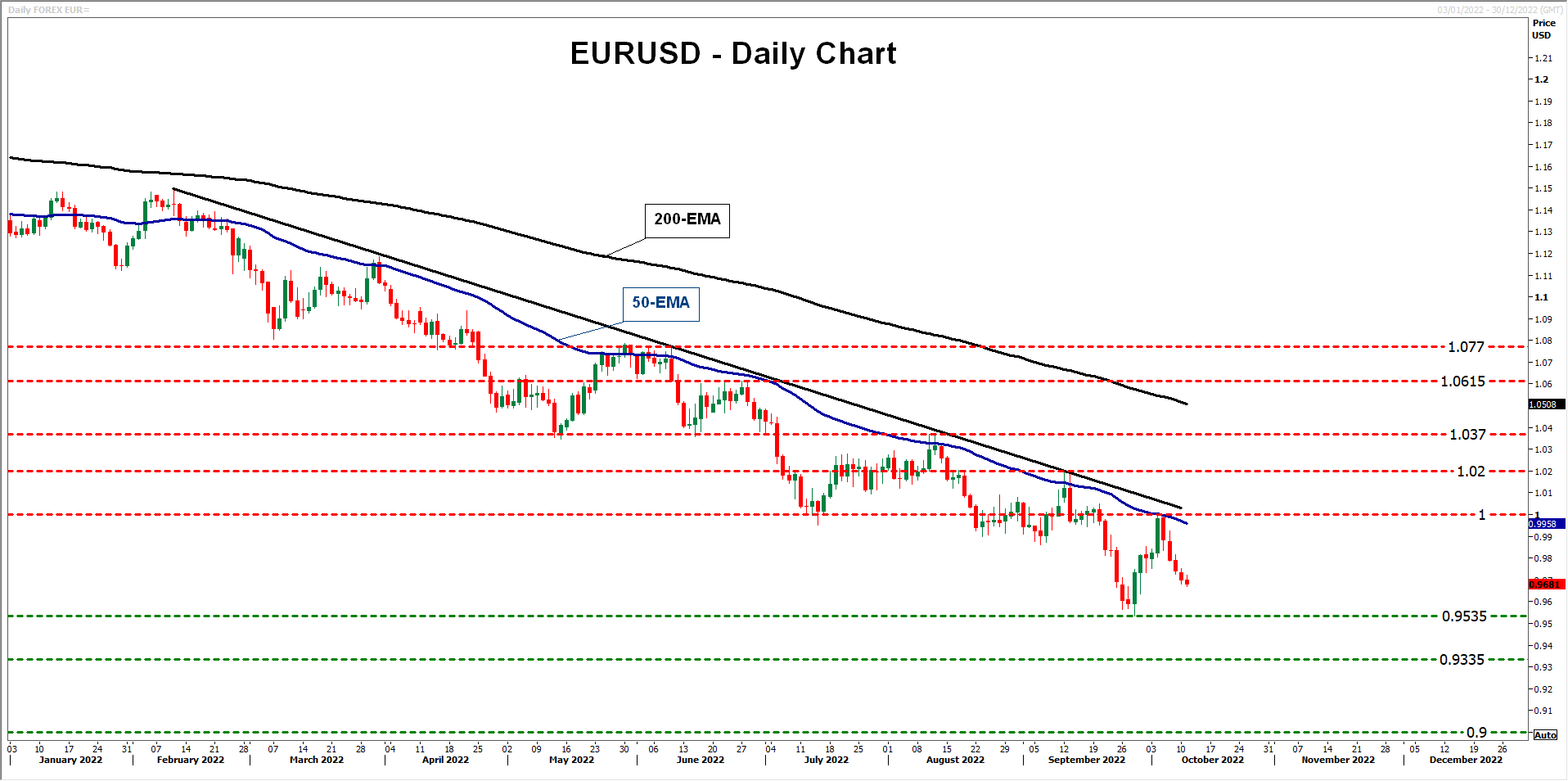

The market reaction could be higher Treasury yields, lower equities, and an even stronger dollar, with euro/dollar sellers perhaps getting confident to aim for another test near the 20-year low of 0.9535, tested on September 28. If they are strong enough to go for a lower low, they will enter territories last seen in June 2002, with the next potential support being the inside swing high of September 16, 2001, at around 0.9335. If that barrier is not able to stop them either, then they could dive all the way down to the round figure of 0.9000, marked by the low of May 15, 2002.

The move that could signal a bullish reversal may be a break above 1.0200 accompanied with improving economic data from the Eurozone and hints that the Fed may eventually not need to hike as aggressively as currently believed. Any signs that the war in Ukraine is moving towards a resolution could also help the euro. The bulls could then get encouraged to aim for the high of August 11 at 1.0370, the break of which could set the stage for extensions towards the high of June 27 at 1.0615.

{kind=link}