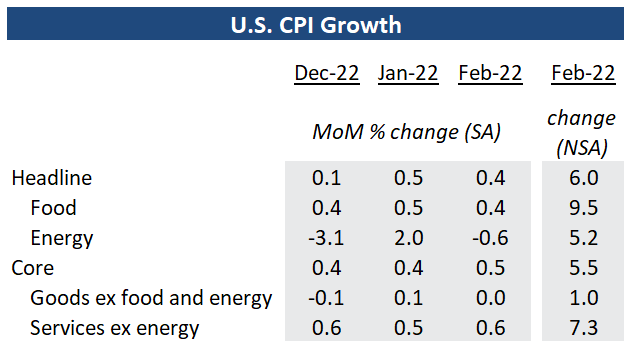

- Headline and “core” ex-food and energy CPI both lower, at 6% and 5.5%

- Details firmer: price pressures broadened, and Powell’s preferred measure ticked higher

- Firm inflation print confronts gathering concerns over financial instability as the Fed draws closer to ending the hiking cycle

February’s inflation report came slightly above consensus expectations, with headline CPI growth ticking lower to 6.5% year-over-year. Food inflation at 9.5% was still elevated but has also continued to moderate after peaking in August 2022. Energy CPI growth slowed to 5.2% year over year, the slowest pace in two years, thanks to declines in fuel oil and utility gas prices. Excluding those more volatile components, “core” inflation slowed to 5.5% year-over-year. The monthly increase however, reaccelerated to 0.5% from January on a seasonally adjusted basis again with 70% of the gain driven by an increase in rent costs. Offsetting some of that strength was weakness in used cars and medical services, both of which saw prices decline again in February.

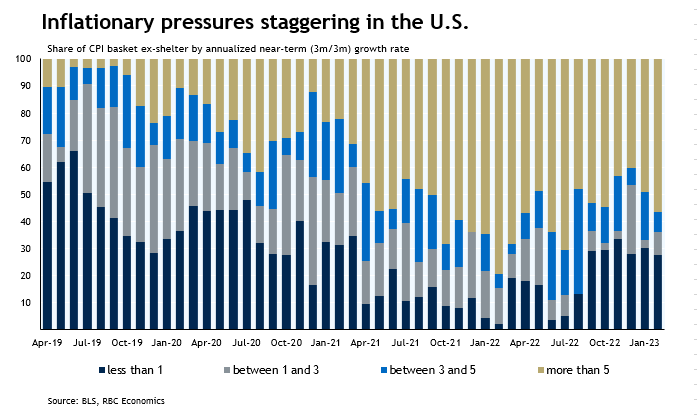

Details behind the CPI prints were firmer. Based on our diffusion measure, the breadth of inflation pressure in the U.S. widened in early 2023 after improving through much of last year. Powell’s preferred inflation gauge – core services ex-rent also grew at a faster 0.5% monthly pace, matching the increase in core CPI. Moving forward, the fact that most of the near-term strength in monthly CPI still reflects past increases in market rents suggests core readings should continue to come down. BLS estimated that the CPI rent measure lags market observed rents by roughly 4 quarters – yearly growth in those market rent measures has already peaked in February 2022.

Strong labour market outturns since the beginning of 2023, alongside elevated wage gains and renewed strength in consumer spending have all been adding upward pressure to the outlook for inflation through this year and next. But much of the impact from monetary tightening to-date has just started to surface – the collapse of three U.S. regional banks over the weekend that rattled bond markets is a prime example. Market pricing after this morning’s report is leaning toward a 25 bp hike for next week’s Fed’s meeting.

{kind=link}