Having defied recession predictions, the Eurozone economy will attract some headlines on Friday when the latest flash PMI readings are due (08:00 GMT). Growth in the euro area has been slowly gaining momentum since late 2022 when the impact of the energy crisis started to dissipate. But there are some doubts as to how strongly the economy can bounce back when interest rates continue to go up. With the European Central Bank’s next policy decision approaching, how important will the data be, and can it help the euro make a convincing break above $1.10?

Relief as Europe avoids a recession

Summer is just around the corner and it’s looking like European economies managed to exit the winter season with only a few minor bruises. Yes, energy bills remain too high for most households and businesses and higher prices in general have been a heavy burden, hampering growth. But inflation in the euro area is on its way down and a recession isn’t on the near-term horizon.

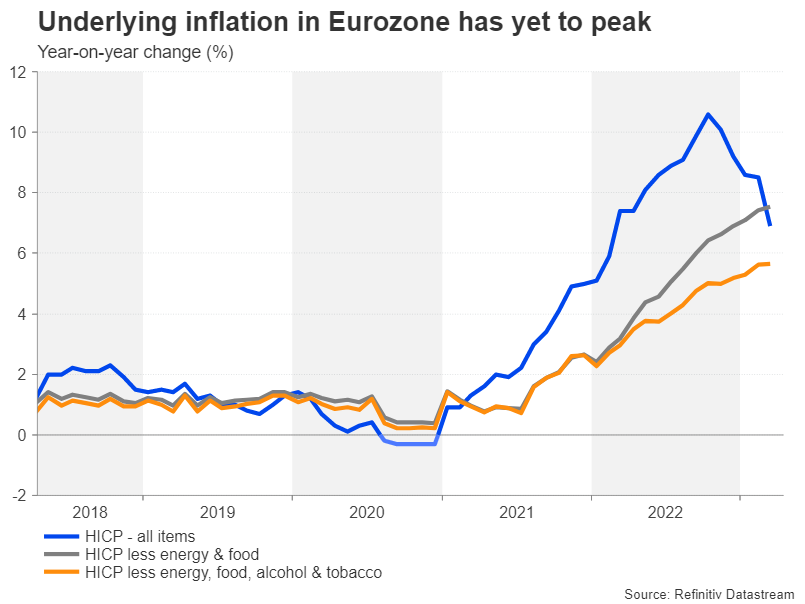

However, the ECB is not done raising rates and growth has been quite sluggish in the last three quarters, so a brighter outlook is far from certain. The most pressing issue for policymakers is the stickiness in core inflation (excluding food, energy, alcohol & tobacco prices), which currently stands at 5.7%.

But more rate hikes to come

Given all the hawkish soundbites coming from the Governing Council, it’s clear that the ECB won’t be satisfied until underlying price indicators have made more progress in edging closer to the 2% target. At the moment, the Eurozone’s two core inflation measures have yet to show a definite sign of having peaked, despite the significant drop in headline CPI in recent months.

What this means is that a 50-basis-point rate hike is essentially at play at the May 4 policy meeting. It wasn’t so long ago in the aftermath of the banking turmoil that investors had priced out the likelihood of large rate increases. But recent remarks from policymakers suggest that the option is firmly on the table in May and Friday’s data may help sway some minds.

Risk of growth stagnating again

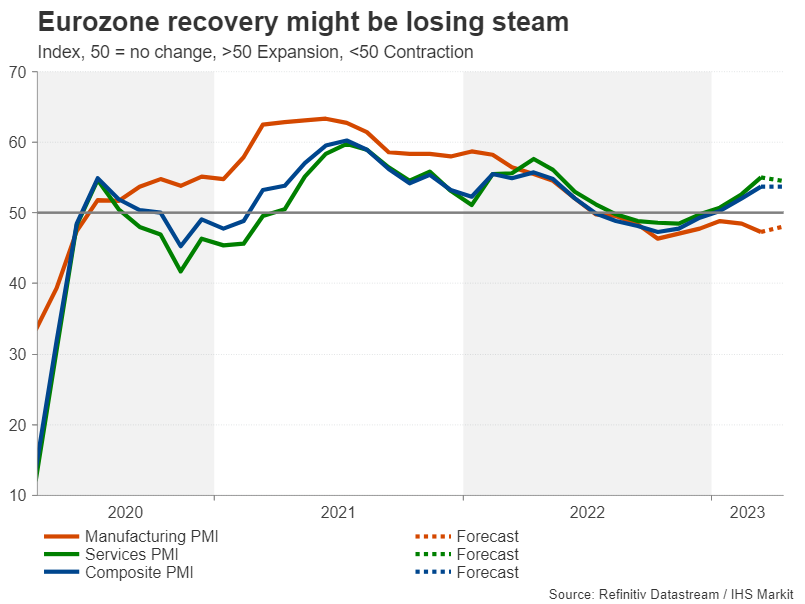

After an impressive rebound, the services sector might have lost some steam in April as analysts expect the services PMI to edge lower slightly from 55.0 to 54.5. Any figure above 50 indicates expansion and that hasn’t been the case for the manufacturing sector. Weak domestic and overseas demand have been a drag on business orders, but the manufacturing PMI is forecast to improve somewhat to 48.0 in April from 47.3 previously. This modest uptick is expected to keep the composite PMI unchanged at 53.7.

There are other data coming up ahead of the May decision that will be important, particularly the flash CPI numbers on May 2. But the PMI surveys will nevertheless offer a crucial insight on how well optimism is holding up, as well as the direction the various components such as input prices and employment are headed in.

Euro outlook positive amid hawkish ECB, soft dollar

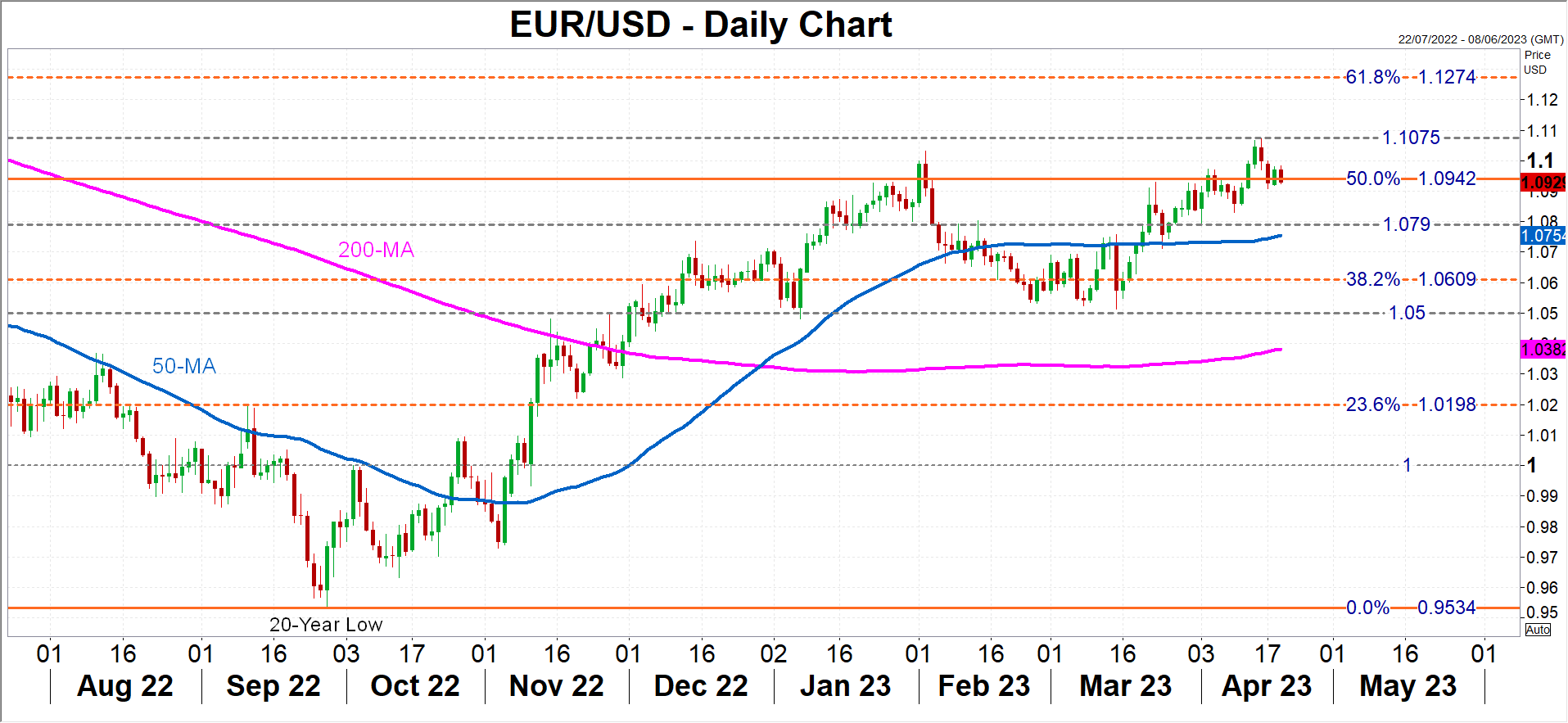

Stronger-than-expected PMI figures could push up bets for a 50-bps hike at the next meeting, which at the moment is only about 35% priced in, setting the stage for another leg up for the euro. The single currency suffered a mild pullback after hitting a wall at $1.1075. Hawkish expectations could enable a break above this key resistance, bringing the 61.8% Fibonacci retracement level of the 2021-2022 downtrend at $1.1274 into view.

However, any disappointment in the PMI indicators may facilitate a deeper downside correction, forcing the 50% Fibonacci to give way. Immediate support is likely to form in the $1.0750-$1.0790 region, comprising the 50-day moving average and a recent congestion point, after which, the $1.05 level would come into focus.

Yet, traders should be wary about anticipating an even sharper slide, as in the bigger picture, the US dollar’s heydays seem to be over. Yield spreads between US and European government bonds have been steadily narrowing over the past few months amid the growing expectation that the Fed will pause its tightening cycle before the ECB does. Unless that view starts to alter, the euro’s downside will be limited.

. Growth in the euro area has been slowly gaining momentum since late 2022 when the impact of the energy crisis started to dissipate. But there are some doubts as to how strongly the economy can bounce back when interest rates continue to go up. With the European Central Bank’s next policy decision approaching, how important will the data be, and can it help the euro make a convincing break above $1.10?){kind=link}