Summary

- As widely expected, the FOMC raised its target range for the fed funds rate by 25 bps today. The Committee has now hiked rates by 500 bps since March 2022, the fastest pace of monetary tightening since the early 1980s.

- The FOMC “remains highly attentive to inflation risks,” and Chair Powell noted in his post-meeting press conference that “we are prepared to do more if greater monetary policy restraint is warranted.”

- But the Committee does not appear to be pre-committing to another rate hike on June 14. In its March 22 statement, the FOMC said that it “anticipates that some additional policy firming may be appropriate.” Today’s statement dropped the reference to “anticipates.” Rather, the statement said “in determining the extent to which additional policy firming may be appropriate…”

- The Committee could indeed hike rates by 25 bps on June 14, but that decision will depend crucially on incoming data over the next six weeks. In our view, the bar to a rate hike on June 14 is higher than it has been at past meetings since March 2022.

- In sum, we would characterize today’s meeting as a “hawkish pause.”

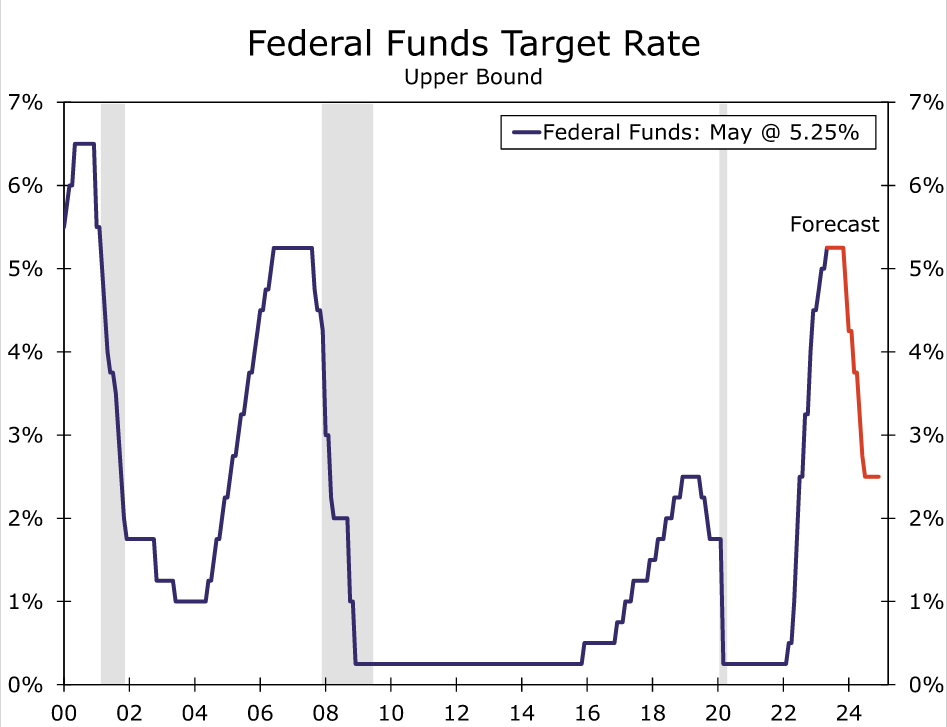

As widely expected, the Federal Open Market Committee (FOMC) decided unanimously today to hike rates by 25 bps, which brings its target range for the federal funds rate to 5.00%-5.25% (Figure 1). The Committee has now hiked rates by 500 bps since March 2022, the fastest pace of monetary tightening since the early 1980s. In explaining its decision to increase the target range again, the FOMC noted that “job gains have been robust in recent months, and the unemployment rate has remained low. Inflation remains elevated.” This characterization of the current state of the U.S. economy is essentially unchanged from the March 22 statement.

In light of the recent turmoil in the American banking system, the Committee continued to express its confidence that the “banking system is sound and resilient.” That said, when it last met on March 22, the FOMC thought that the turmoil was “likely to result in tighter credit conditions.” Today’s statement implied that credit conditions have indeed tightened, which “are likely to weigh on economic activity, hiring, and inflation.” In other words, the FOMC seems resigned to headwinds on growth in coming quarters.

In our view, the most notable part of today’s statement was the section outlining the outlook for policy going forward as the FOMC watered down its language regarding the need for additional monetary tightening. In its March 22 statement, the Committee said that it “anticipates (our emphasis) that some additional policy firming may be appropriate…” In the statement the FOMC released today, the Committee dropped “anticipates” and simply said “in determining the extent to which additional policy firming may be appropriate…” In other words, additional tightening may be needed—Chair Powell said in his opening statement of the post-meeting press conference that “we are prepared to do more if greater monetary policy restraint is warranted”—but the FOMC does not appear to be pre-committing to another rate hike on June 14.

That decision on June 14 will depend crucially on “economic and financial developments” over the next six weeks. The Committee will also continue to assess “the cumulative tightening of monetary policy” which it has already undertaken as well as “the lags with which monetary policy affects economic activity and inflation.” In our view, the Committee is signaling a hawkish pause in the tightening cycle. That is, the FOMC could clearly hike rates again, especially in light of the sentence in the statement reiterating that Committee members remain “highly attentive to inflation risks.” However, the bar to hike again on June 14 appears higher than it has been at past meetings since March 2022.

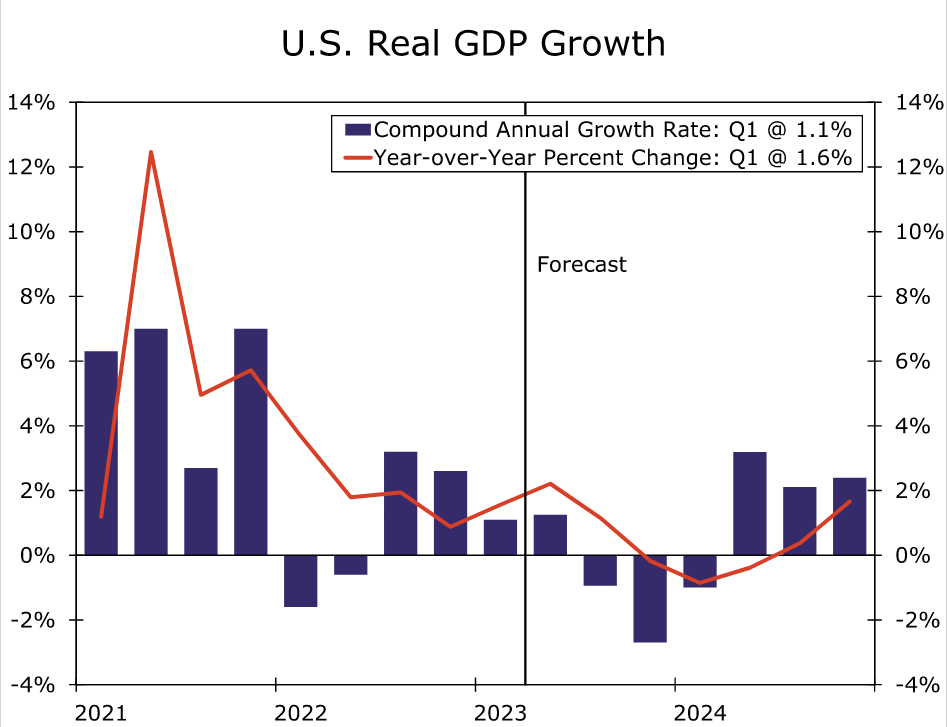

We anticipate that the FOMC will indeed remain on hold on June 14. By the time the July 26 meeting rolls around, we believe that incoming data on economic activity will be soft enough to keep the Committee on hold again. We forecast that real GDP will start to contract, albeit at a gradual rate, starting in the third quarter (Figure 2). This weakness in economic activity should continue to stay the FOMC’s hand at its meetings in September and November. But as the downturn in the economy gathers pace and as the Fed becomes more convinced that inflation is heading back toward 2% on a sustained basis, we look for the FOMC to begin an easing cycle at the very end of this year/early next year (Figure 1).

{kind=link}