Fed Preview: On Hold

- We expect the Fed to maintain rates unchanged next week, markets price in a modest 25% probability of a 25bp hike.

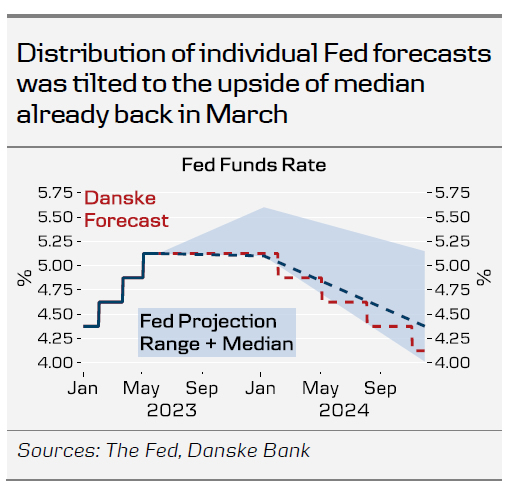

- Focus will be on communication around potential hike in July & the updated dots. The Fed is unlikely to close the door for hikes, but we doubt they will materialize.

- We see downside risks to consensus expectations for May CPI, and forecast +0.2% m/m (4.2% y/y) for headline & +0.3% m/m (5.2% y/y) for core.

Markets have focused on the renewed uptick in macro momentum, which has resurfaced fears of inflation turning more persistent. But we doubt the rise in leading indicators will be sustained, and see evidence of underlying inflation continuing to gradually ease.

While the May NFP surprised markedly to the upside, the underlying details were much weaker. Employment growth is heavily concentrated on sectors such as leisure & hospitality, which have for a long time suffered from labour shortages. As labour force participation is recovering, employment rises even if broader labour demand is weakening. But importantly, supply-driven employment growth is not inflationary, rather the opposite.

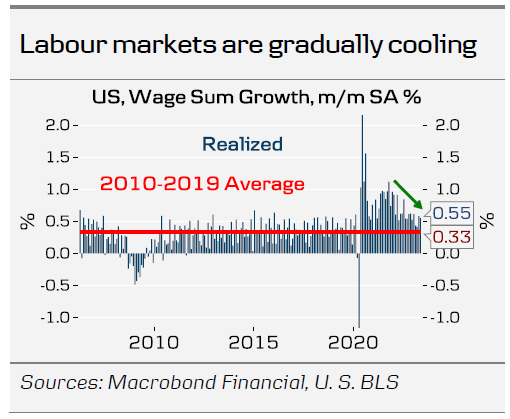

The number of employed workers declined by 310k, which together with labour force growth of 130k suggests that slack is finally forming into labour markets. As such, wage sum growth remains on a downtrend, and our preferred measure of underlying inflation, core services CPI & ex. housing & health care, has also stabilized in the last two releases.

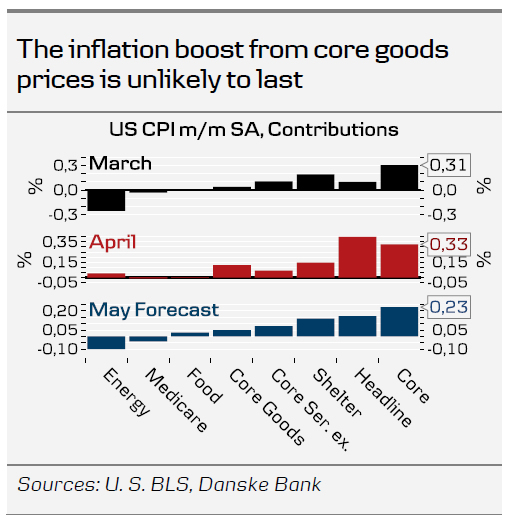

We expect the May CPI, released just ahead of the FOMC meeting, to slow down to 0.2% m/m (4.2% y/y) driven by negative contribution from energy prices. We also forecast Core CPI to continue cooling to 0.3% m/m (5.2% y/y). Manufacturing PMI price indices and used car prices suggest that the April uptick in core goods CPI will not be sustained, while we also look for continuing gradual slowdown in core services and shelter components.

Markets are pricing in a larger (75-80%) probability for a hike in July. Notably, it would only require two individual FOMC participants to shift their 2023 rate projections higher to lift the median ‘dot’ to 5.25-5.50%, which could spark a hawkish initial reaction in the markets. We still think the bar for restarting hikes in July will be high unless inflation pressures clearly accelerate over summer, which we consider unlikely. Private consumption has so far remained markedly resilient compared to the plunge in real disposable income, but with excess savings soon depleted, we think growth backdrop will remain weak.

Negative signals from longer-lead monetary indicators combined with the risk of tightening liquidity conditions over summer will further discourage rate hikes when inflation has already turned lower. Consumers’ inflation expectations have continued declining, and currently hover around 4-5%, suggesting that holding nominal rates at 5% will maintain monetary policy stance sufficiently restrictive.

We make no changes to our forecasts, and expect the Fed to maintain rates at the current level for the remainder of the year. A pause could pose near-term upside risks to EUR/USD, but we still maintain a bearish view on the cross towards H2.

{kind=link}