The July central banks meetings lived up to expectations as both the Fed and the ECB announced their respective rate hikes but essentially removed their forward guidance. Data dependency is the new name of the game as the market is now counting down to the mid-September meetings. Which are the next key dates until the September 14 ECB gathering? What data figures would the ECB hawks like to see to push for another rate hike? Could the euro manage to defy expectations for a tough August against the US dollar?

ECB’s change of strategy

ECB’s President Lagarde, representing the entire governing council, announced a strategy change, following nine consecutive rate hikes over the past 12 months, by moving to a data dependency stance. Using Lagarde’s own words, “data and our assessment of data will actually tell us whether and how much ground we have to cover”. The market obviously interpreted her message as dovish with the euro underperforming the dollar.

It has always been difficult for central banks to signal the likely end in their hiking (or easing) cycles as they have to maintain the fragile balance in their boards and avoid market disappointment. A big plus for Lagarde, compared to the Fed’s Chairman Powell, is that she appears to have developed a decent relationship with the market in the current hiking cycle. This could prove crucial if the ECB decides to announce another rate hike at the September 14 gathering.

Key dates until the next ECB meeting

With data releases being the new compass for the ECB going forward, Table 1 below shows the key data releases and their respective dates up to the September ECB meeting.

What would the ECB hawks need to see to support a rate hike?

The ECB’s mandate remains price stability. Naturally, they are closely following all the inflation-linked data releases, indicators and projections. This framework includes market-based indicators like the 5year-5year inflation swaps, which remains elevated at 2.48%, the various business surveys and the famous ECB staff projections. Understandably, the market would be on its toes on the relevant dates as seen in Table 1 above. However, the key ones for the next 45 days are the August 23 release of the preliminary August PMIs (specifically, the prices paid subcomponent), and the German and euro area aggregate preliminary CPI prints for August on August 30/31.

A plethora of upside surprises could prove decisive for the September discussion. Especially if the headline euro area CPI stabilizes above 5% following an aggressive downward move since November 2022 and the core CPI indicator continues to confirm its stubborn nature. In addition, the ECB staff forecasts, to be released after the September 14 ECB meeting, play a key role in setting monetary policy. Therefore, the combination of strong inflation prints for August and the 2025 CPI rate staff projection remaining comfortably above the 2% threshold (it was seen at 2.2% at the June 2023 staff projections), could tip the balance in favour of another 25bps rate move.

Certain ECB members seem to care more about growth

Certain ECB members seem to be really concerned by the recent bad run of growth-related data releases, and particularly by the fact that Germany has been the growth laggard in 2023. It is worth noting that we are experiencing a rather rare occasion of France outgrowing Germany for three consecutive quarters. Therefore, ECB members will likely be all over the growth data as the final 2nd quarter GDP prints from Germany and the euro area aggregate are coming on August 25 and September 7 respectively. Stronger growth figures, especially in Germany, would really be welcomed by the ECB hawks.

Furthermore, the German IFO surveys, German factory orders and the various PMI surveys (especially the orders subcomponents) would undoubtedly be dissected by both sides at the ECB as they try to prop up their arguments for the September meeting. Especially in the case of the PMIs, the ECB hawks would really love the headline German manufacturing PMI to reverse its recent tanking and plot a course towards the 50-midpoint. Such a move would probably need further positive news from China, on top of the recent announcements that have not really caused much enthusiasm in the market.

Euro would benefit from stronger data releases

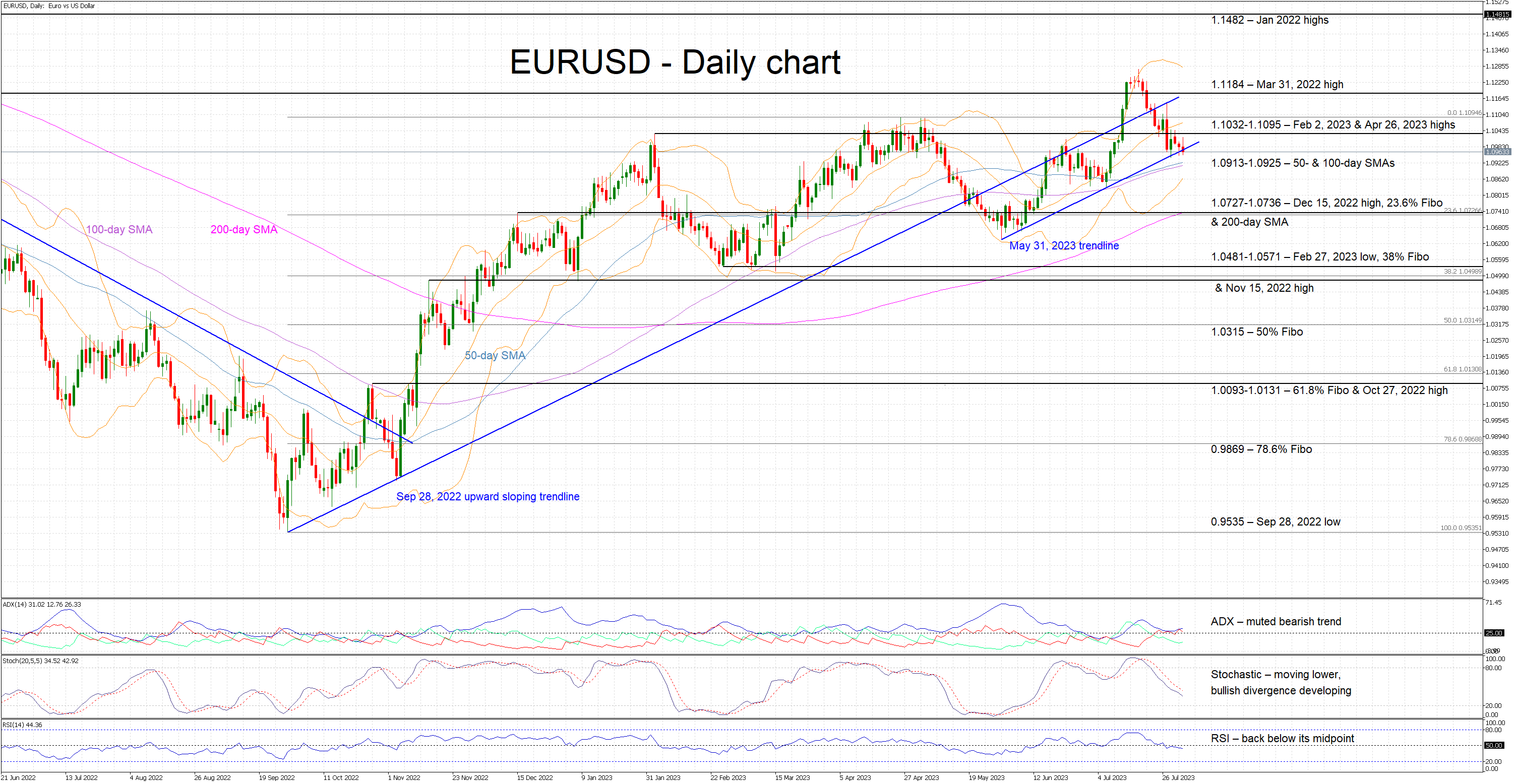

The euro remains on the backfoot as the main driver of its recent performance was the market’s confidence that the ECB will maintain its hawkish strategy. Removing this factor, the euro looks very vulnerable and thus raising questions for the viability of the long-term rally recorded against the US dollar since the September 28, 2022 low. A plethora of upside data surprises, particularly on the inflation front, could reenergize the euro bulls in recording a new 2023 high above the current one at $1.1275. On the flip side, the $1.0913-$1.0925 area is important from a short-term perspective as a break of this range would open the door to a more aggressive move towards $1.0727.

{kind=link}