- Skyrocketing bond yields put markets in a spin

- Fed’s higher for longer calls grow louder

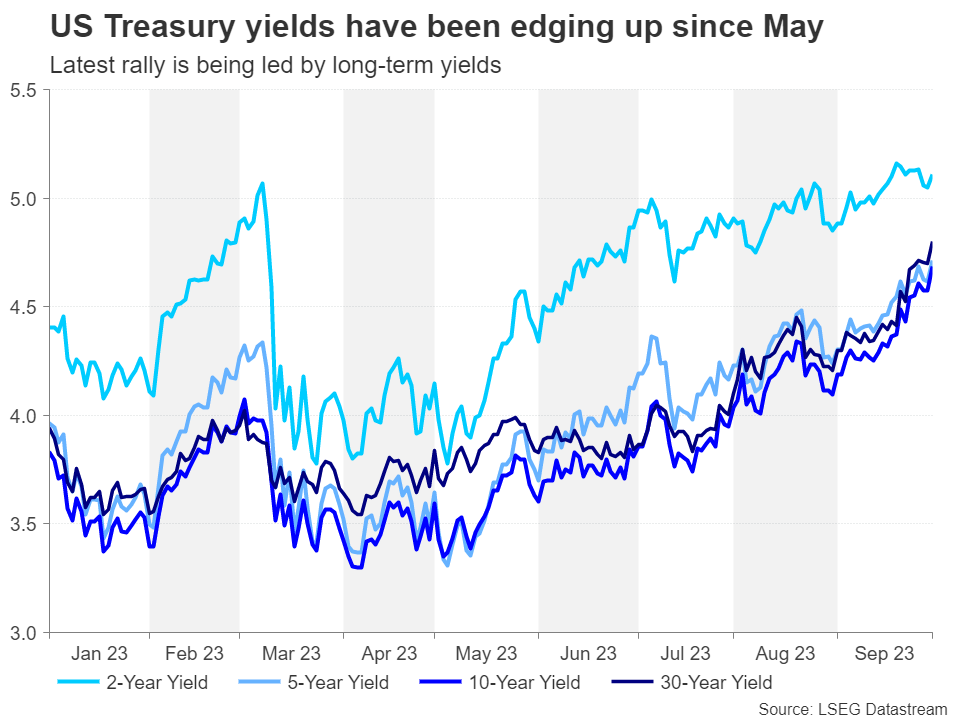

- US 10-year yield approaches 4.8% at 16-year high

- Can they reach 5.0% and how soon before something breaks?

Yields heeding the higher for longer message

Yields on government bonds are flying again as central banks are all singing from the same hymn sheet lately, flagging that interest rates will stay high for a longer period of time. This isn’t exactly a new revelation for investors but more recently, the message has started to sink in deeper as the combination of persistent price pressures and resilient economies has taken everyone by surprise.

With rates potentially yet to peak in the United States and elsewhere, government bond yields have been rallying since May when the US banking turmoil began to dissipate. However, this latest leg of the rally isn’t so much driven by expectations of where interest rates will peak but more about how long they will stay at elevated levels.

There may be more tightening to come

The Federal Reserve and even the European Central Bank may yet have to tighten further, but it’s unlikely this would involve anything more than a 25-basis-point hike. What’s gotten markets so jittery is the prospect of rates staying near current levels for an extended duration. That is why long-dated government bonds have borne the brunt of the latest selloff, pushing 10-year yields to more-than-decade highs.

The last time the 10-year Treasury yield was above 4.8% was at the onset of the global financial crisis in the summer of 2007. Not long after that, rock-bottom rates became the norm. This highlights just how markedly the inflation picture has altered since the pandemic, with the supply and energy shocks irreversibly lifting prices.

Job not done yet on inflation

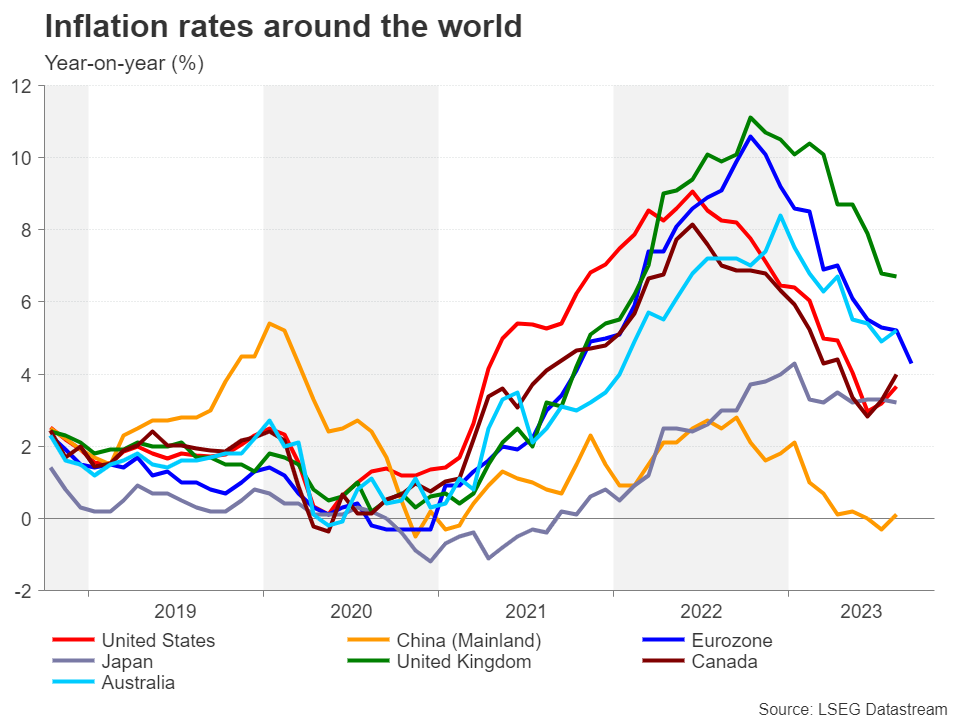

However, falling inflation has been the big story of 2023 – so why are the Fed and other central banks still thinking about hiking further? The problem is that despite good progress, inflation in most places has some distance to cover before reaching the 2% target. In the US, the core PCE measure of inflation stood at 3.9% in August – almost double the Fed’s objective.

Inflation may have come down sharply over the past year as the energy crisis subsided, but the next phase may take a lot longer. There are several factors that could prevent inflation from dropping all the way down to 2% in a quick manner and they vary in each country. In America, it is the tight labour market and robust consumer spending.

The elusive soft landing

The Fed is in a tricky spot at the moment when it comes to correctly gauging how restrictive policy has become. It risks tightening more than it has to should it act solely on the actual data, or doing too little should its caution on the basis that there are transmission lags in monetary policy prove to be a miscalculation. With various measures of inflation expectations converging slightly above 2% and hiring slowing down lately, the Fed seems to be taking its chances with the latter option.

But this is not the entire explanation. The Fed is desperate to engineer a soft landing for the economy, which comes at a price as it would necessitate taking a more patient approach to hitting the 2% target in a sustainable manner. Policymakers are thus effectively making a conscious decision to let inflation run above target for longer so as not to choke off economic growth.

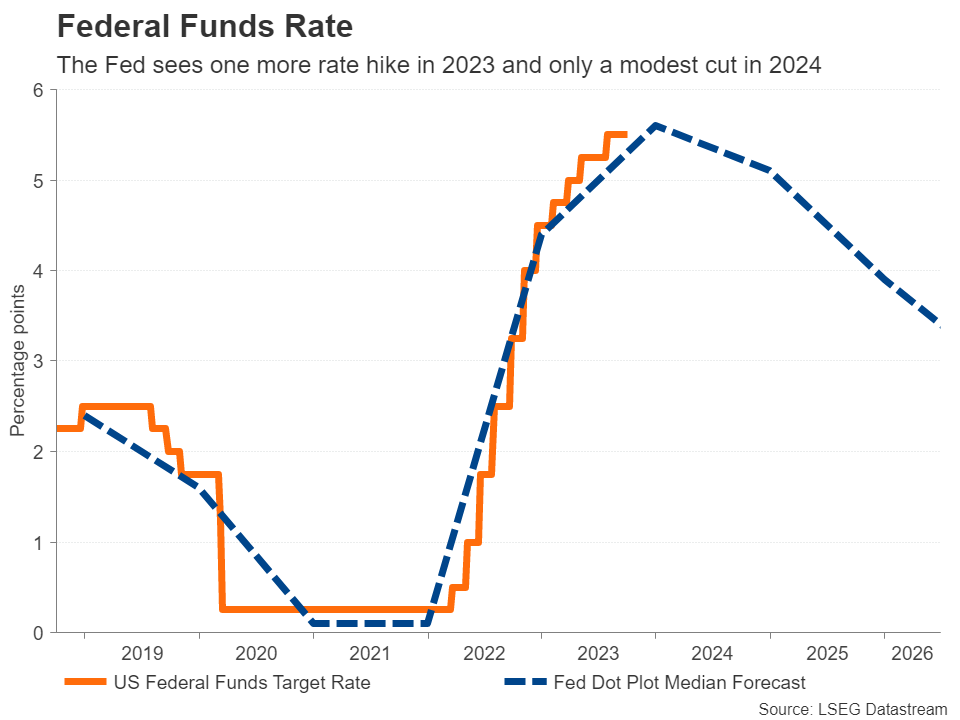

What this means for monetary policy, however, is that whilst rates would peak somewhat lower, they’re less likely to be cut sooner. For the US where the economy continues to display remarkable resilience, this is even more significant as any cut would risk fuelling renewed inflationary pressures.

Is the only way up for yields?

The recent gains in Treasury yields may be a reflection of this realisation by investors. The question now is, can yields rise further, and if so, at what point will higher yields inflict some serious damage on the economy?

For the moment, neither consumption nor the labour market are showing any major signs of cracks. Should this still be the case by December, the Fed may well end the year with another rate increase. Not only that, but the Fed might also lift its projected rate path again, spurring another rally in long-term yields.

Assuming that the outlook in Europe and elsewhere doesn’t improve, the US dollar would be in a position to appreciate further, while there could be more pain in store for US equities. So far though, the upside surprises in the economic data, the artificial intelligence (AI) mania as well as the defensive nature of many tech stocks have all contributed to driving Wall Street indices higher even as financial conditions have tightened.

Small cracks are appearing in the economy

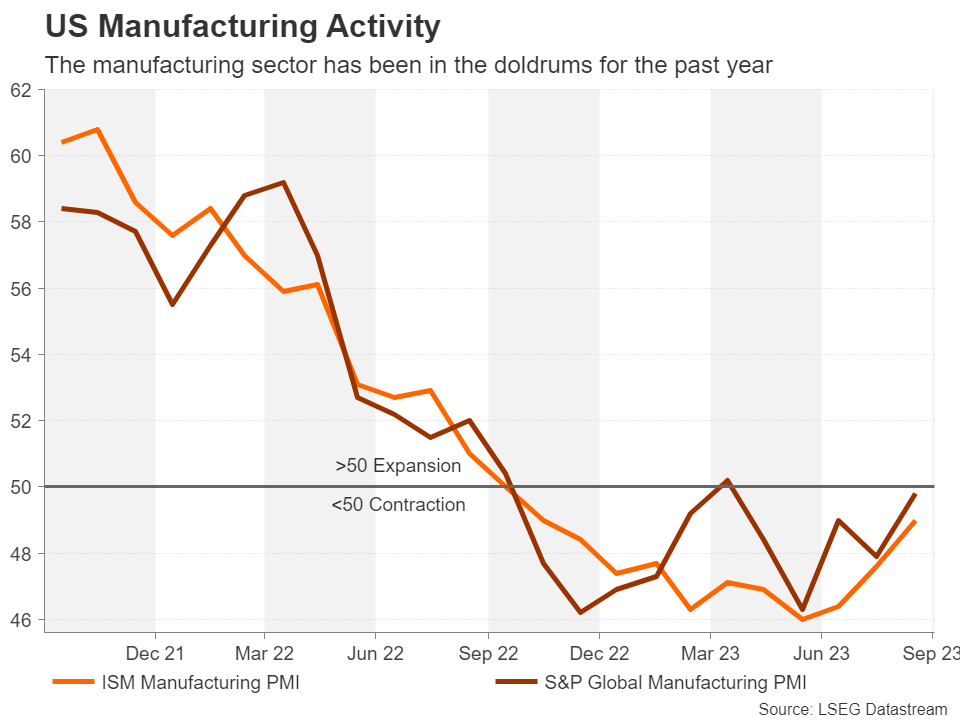

But it’s hard to see this picture lasting once the 10-year yield nears the 5.0% level. Looking under the hood, there are several signs of trouble brewing. The manufacturing sector is contracting, and banks are lending less, hitting struggling businesses and new investment. Households have almost drawn down on their excess savings and this coincides with an increase in the number of households unable to pay their credit card debts. In addition, Americans will soon have to start repaying their student loans as the pandemic support expires.

Resurgent oil prices are another worry as they threaten to push up costs again just as the pain was easing. Not to forget the slowdown in Europe and China that’s bound to affect the earnings for US multinationals, all this could yet kill any momentum in the economy, if not tip it into recession.

Is a recession only delayed, not cancelled?

For now, the expectation of a soft landing is maintaining the upward pressure on yields, while the deluge of new debt issuance by the Treasury Department is worsening the rout in the bond market. Unless there’s a sharp deterioration in the outlook, it is difficult to envisage bond yields retreating substantially in the near future.

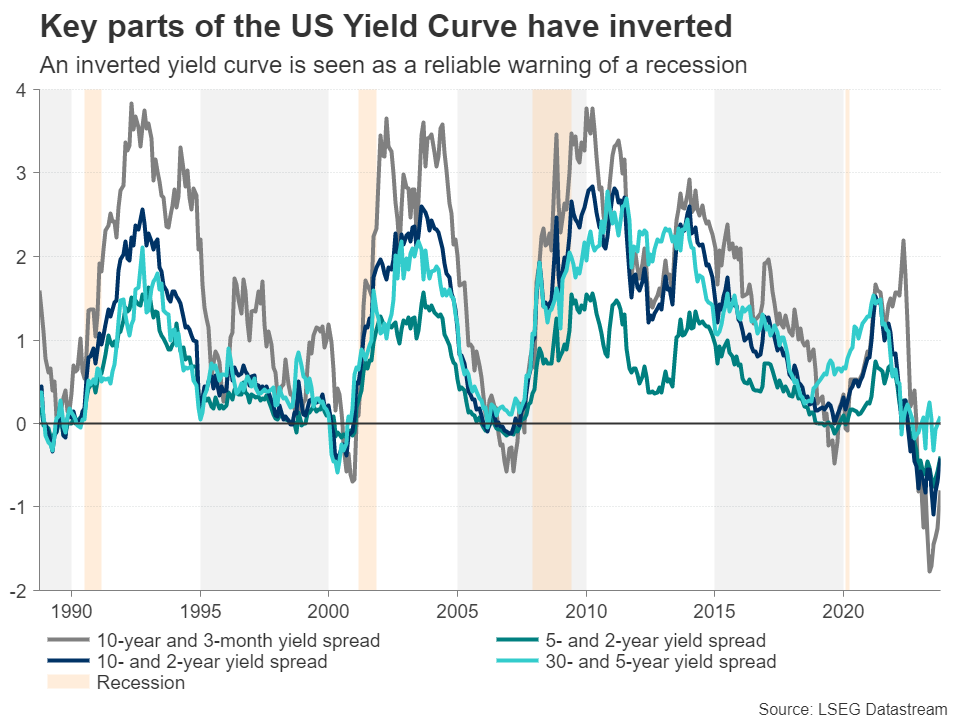

The danger is that the risk of a recession may not be as low as policymakers and investors would like to believe. The inverted yield curve continues to flash red even though the gap between long- and short-term yields has narrowed over the last few months. The other cause of concern is that in the past, calls for a soft landing have often tended to precede recessions and what may be happening now is simply the timing of one being pushed further and further back.

Yields vs stocks

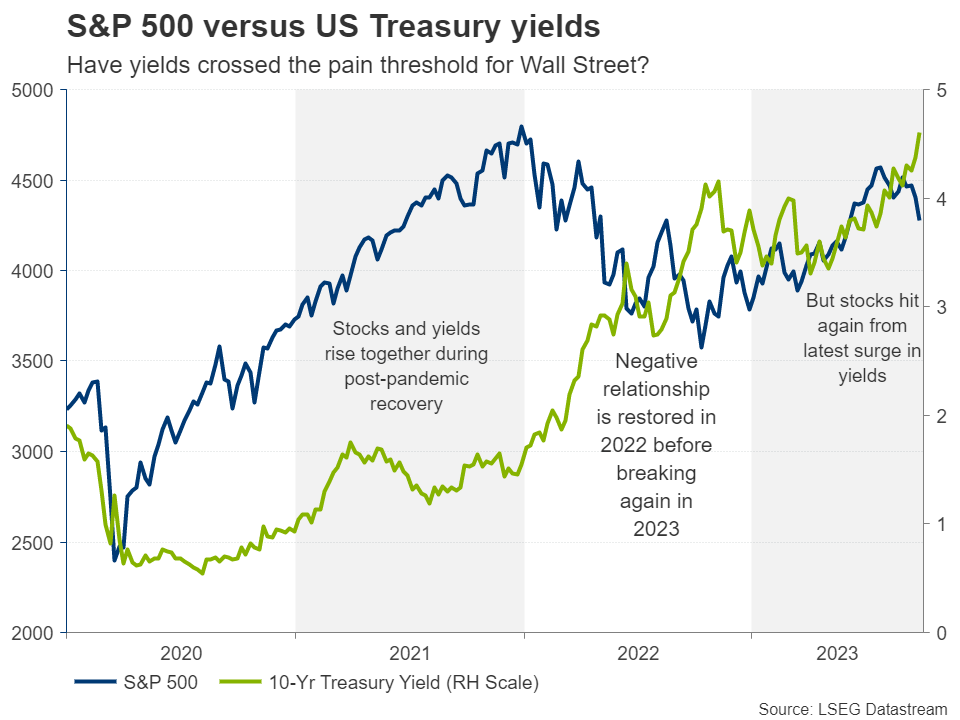

Adding to the confusion is the broken negative relationship between Treasury yields and the stock market. When yields reach a cycle peak, stocks traditionally enter a bear market. However, during the post-pandemic recovery, the S&P 500 and the 10-year yield rallied in tandem.

The negative relationship corrected itself last year when Wall Street declined and yields kept rising, but it broke again in the first half of 2023. Since September, however, yields and stocks have gone their opposite ways once more, in a possible sign that yields may have already reached the pain threshold for Wall Street. Does this hold true for the economy as well?

{kind=link}