Summary

- We expect that the Federal Open Market Committee (FOMC) will leave the target range for the federal funds rate unchanged at 5.25%-5.50% at the conclusion of its next meeting on November 1. Financial markets are essentially priced for no change as well.

- Although the rate of real GDP growth in the U.S. economy remains strong, inflation is moving back toward the FOMC’s target of 2%. That noted, we believe that the post-meeting statement will continue to characterize inflation as “elevated”, while also noting that recent geopolitical events add uncertainty to the outlook.

- Recent comments by Fed officials suggest that most Committee members are comfortable leaving the stance of monetary policy unchanged at the upcoming meeting. That said, most policymakers indicated at the September FOMC meeting that they thought another 25 bps rate hike would be appropriate by the end of this year.

- We believe the FOMC will want to keep its options open for further tightening. Therefore, we think the post-meeting statement will maintain the language that signals some additional policy tightening may be appropriate.

- We do not expect the FOMC will make any changes to the pace at which it is allowing Treasury securities and mortgage-backed securities (MBS) to run off the Fed’s balance sheet.

We Expect the FOMC Will Leave Rates Unchanged on November 1

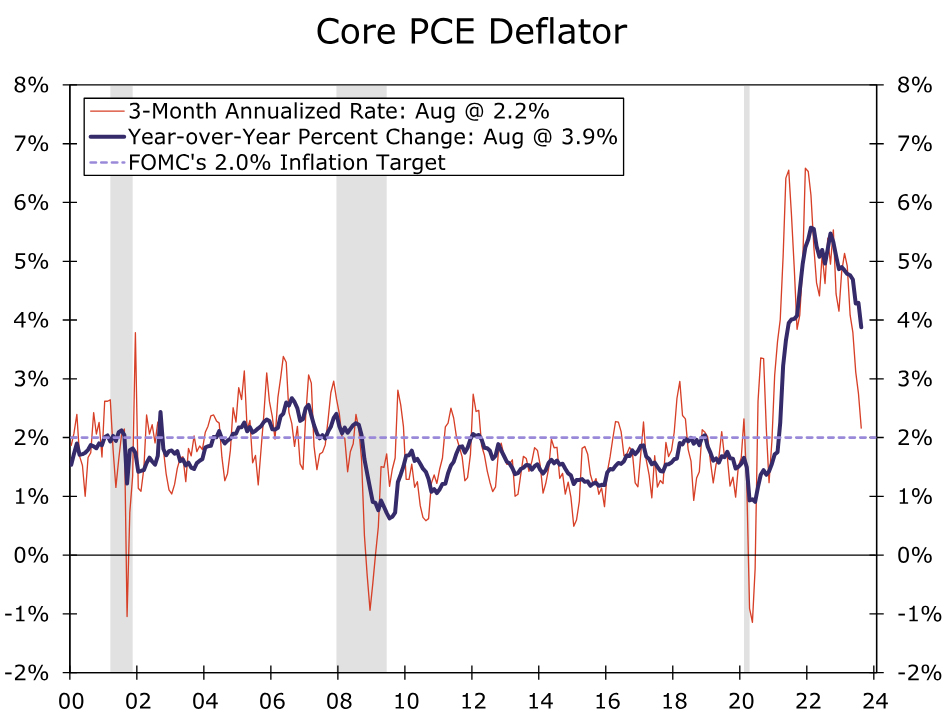

We share the widespread expectation that the Federal Open Market Committee (FOMC) will leave the target range for the federal funds rate unchanged at its upcoming meeting on October 31-November 1. Since the Committee last met, underlying inflation has shown continued signs of slowing. The core PCE deflator, which is the FOMC’s preferred measure of consumer price inflation, edged up just 0.1% in August relative to the previous month. Over the three-month period ending in August, core PCE inflation rose at a 2.2% annualized rate, not far from the Committee’s 2% target (Figure 1). Over the 12-month period ending in August, core PCE inflation was 3.9%, its first reading below 4% since June 2021.

These are welcome developments for a Committee that has been fighting to combat high inflation since early 2022. That said, it remains far from certain that inflationary pressures are fully in check. Data for PCE inflation in September are not yet available and will be released on October 27. Recently released data on the Consumer Price Index (CPI) and Producer Price Index (PPI) suggest that core PCE inflation strengthened a bit in September. As we wrote in our most recent CPI report, we think this monthly bounce is more noise than signal, and we believe the downward trend in inflation remains in place despite the periodic bumps in the road. However, we think the Committee will be sensitive to any upward surprises on the inflation front, and the September inflation data argue for the FOMC remaining cautious about how quickly inflation can return to target on a sustained basis.

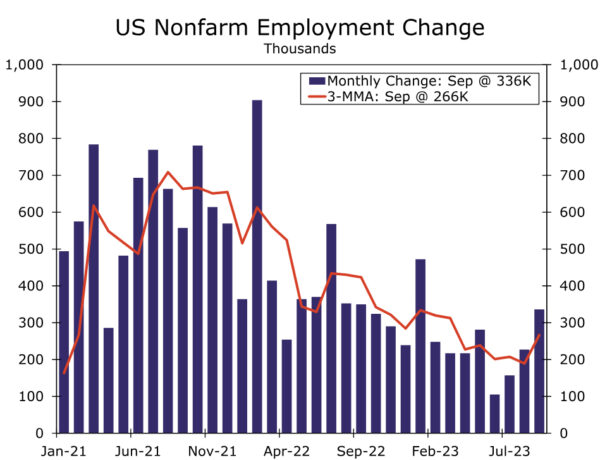

Data on economic output and employment have remained rock solid. Real GDP appears to have grown at roughly a 5% annualized rate in Q3-2023. A pickup in employment growth—nonfarm payrolls rose at an average monthly rate of 266K in Q3 relative to the average monthly rate of 201K in the second quarter—is consistent with this acceleration in real GDP (Figure 2). Moreover, the drivers of economic growth appear to have been broad-based in the third quarter.

Another Pause on November 1 Appears to be the Consensus View on the FOMC

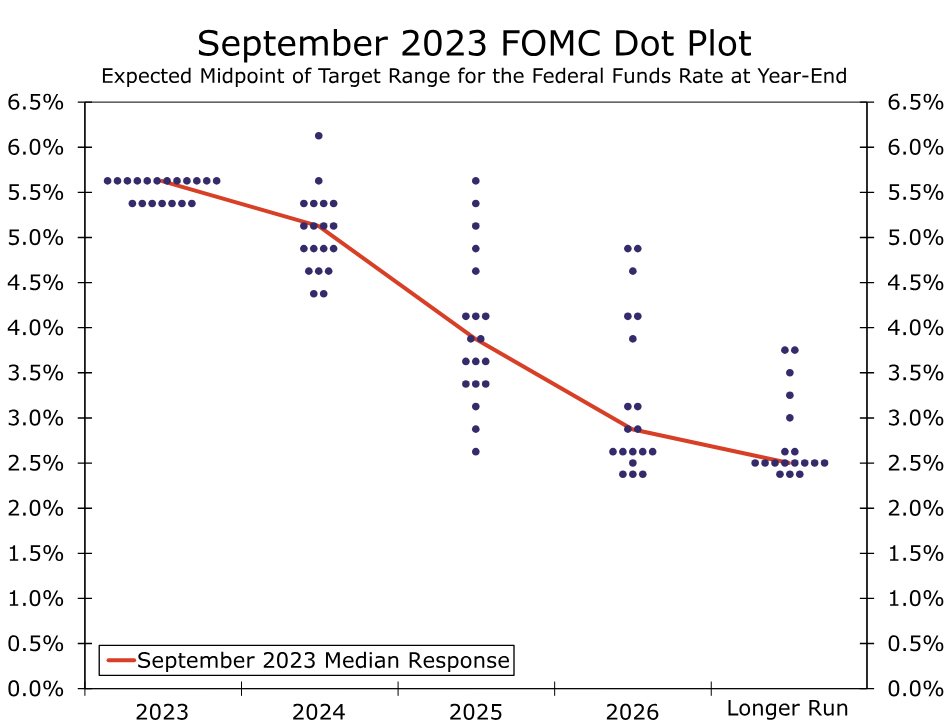

The dot plot from the September FOMC meeting indicated that the median participant supported one more 25 bps rate hike by the end of the year (Figure 3). However, recent comments from Federal Reserve officials suggest that another hold on November 1 is the consensus view. On October 18, Governor Waller stated the following: “I believe we can wait, watch and see how the economy evolves before making definitive moves on the path of the policy rate.” Patrick Harker, who is the president of the Federal Reserve Bank of Philadelphia and a voting member of the FOMC this year, sounded even more dovish on October 13 when stating that “I believe that we are at the point where we can hold rates where they are.” Financial markets appear to have gotten the memo. Fed funds futures heading into the blackout period were priced for essentially no chance of a 25 bps rate hike on November 1.

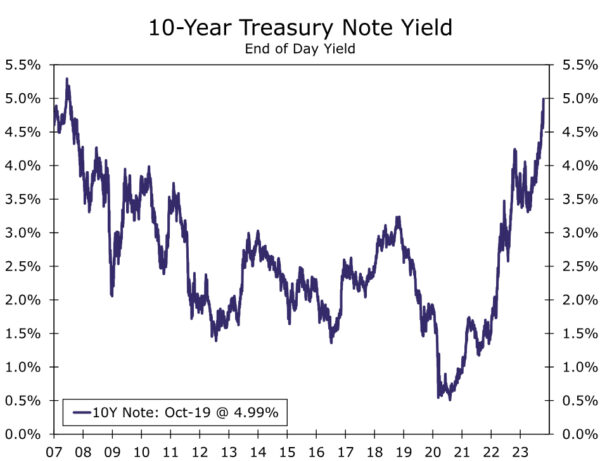

Other Committee members have pointed to the rise in long-term Treasury yields in recent months as another form of tightening that, if sustained, will likely restrain economic activity and inflation (Figure 4). The yield on the 10-year Treasury note has climbed from about 4% at the end of July to nearly 5% today. Vice Chair Philip Jefferson expressed this sentiment on October 9, saying that “I will remain cognizant of the tightening in financial conditions through higher bond yields and will keep that in mind as I assess the future path of policy.” In a speech shortly before the blackout period, Chair Powell similarly noted that “financial conditions have tightened significantly in recent months” and that “we remain attentive to these developments because persistent changes in financial conditions can have implications for the path of monetary policy.”

Current Rate of QT Should Remain in Place

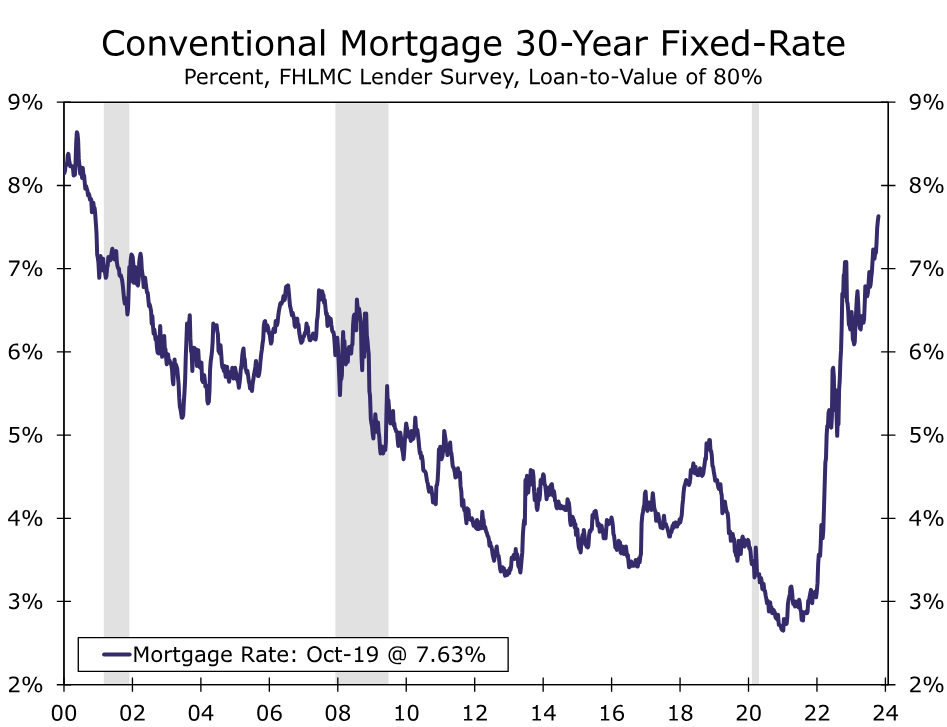

We also expect the FOMC will once again reaffirm the current pace of balance sheet runoff, commonly known as quantitative tightening (QT). As we wrote in a recent report, QT is serving its role as a secondary form of policy tightening. As the central bank reduces its holdings of Treasury bills, notes and bonds and mortgage-backed securities, the additional supply of these securities puts upward pressure on intermediate and longer-term bond yields, all else equal. This in turn leads to higher borrowing costs for households and businesses and restrains economic activity. As an example, the 30-year fixed rate mortgage is currently approaching 8% (Figure 5). QT is far from the only contributor to the recent run-up in longer-term yields, but it is important to remember that even if the Committee maintains the fed funds rate at current levels for the foreseeable future, policy tightening via QT is still running in the background.

Given that some members likely still favor a rate hike before year-end, we do not anticipate any material changes to the post-meeting statement. We think the Committee will continue to refer to inflation as “elevated” and will maintain the language that signals some additional policy tightening may be appropriate. The latter line affords the Committee maximum flexibility should it determine an additional rate hike may be needed at its next meeting on December 12-13. We also expect the statement to note that the recent geopolitical events in the Middle East add additional uncertainty to the outlook.

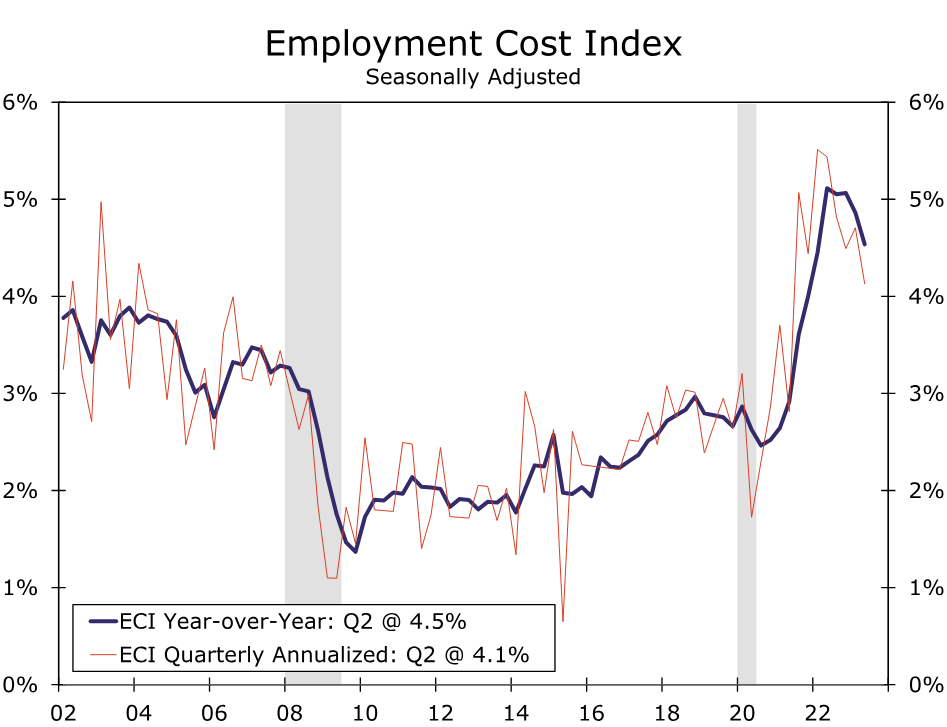

What will the Committee members be watching over the next week or so while in the blackout period? In our view, the biggest remaining data releases until the meeting are the advance release of Q3 GDP (October 26), the September personal income & spending report, which includes monthly PCE inflation (October 27) and the Q3 report on the Employment Cost Index (October 31). The Employment Cost Index (ECI) is the Fed’s preferred measure of labor cost growth. As Figure 6 illustrates, labor costs have been decelerating amid moderating labor demand growth and robust labor supply growth. The Committee will be watching closely for additional evidence that this slowdown in labor costs remains in place despite strong job growth in recent months.

will leave the target range for the federal funds rate unchanged at 5.25%-5.50% at the conclusion of its next meeting on November 1. Financial markets are essentially priced for no change as well.){kind=link}