Summary

October’s softer-than-expected CPI print is an encouraging development for the FOMC and reinforces our view that the FOMC has ended its hiking cycle. But, we do not see the latest data as a game-changer for inflation’s path ahead. With inflation in October held down by volatile components like gasoline, travel services and autos, we expect inflation’s return to 2% will continue to be a slow grind.

Inflation Reprieve

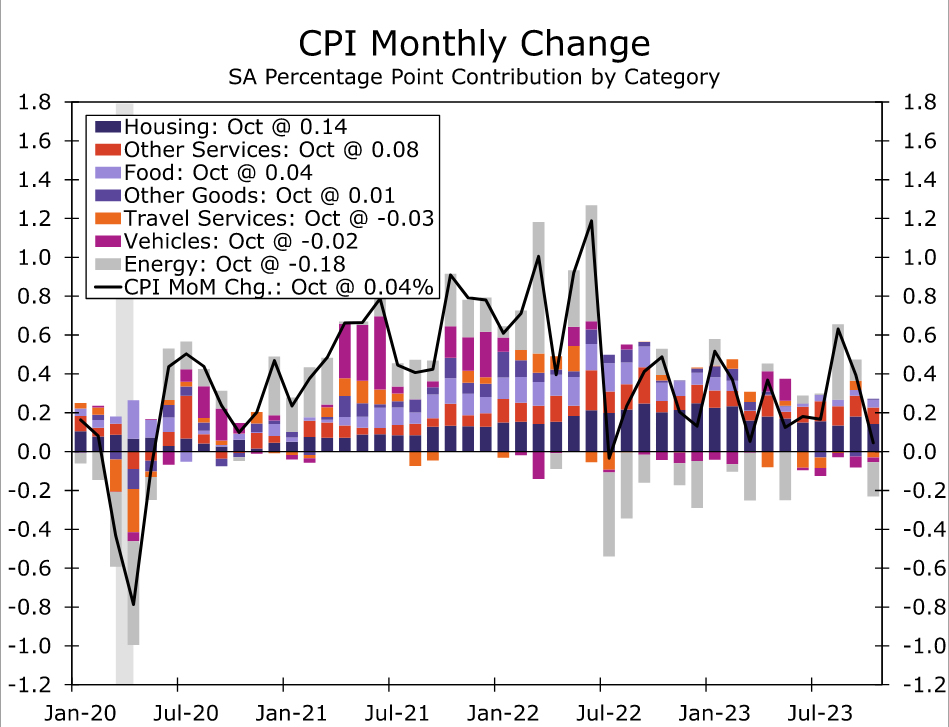

The consumer price index was unchanged in October, the first time monthly inflation was flat since July 2022. The Bloomberg consensus expected a 0.1% increase in the CPI, so this reading was a bit cooler than anticipated. As was the case in July 2022, a large drop in gasoline prices was the main contributor to the soft monthly reading. Gas prices fell 5.0% in October, more than reversing the 2.1% increase that occurred in September. Energy services prices, which includes electricity and utility gas, rose 0.5% in the month. Food prices increased 0.3% in October with food away from home inflation (+0.4%) outpacing the increase in prices at the grocery store (0.3%).

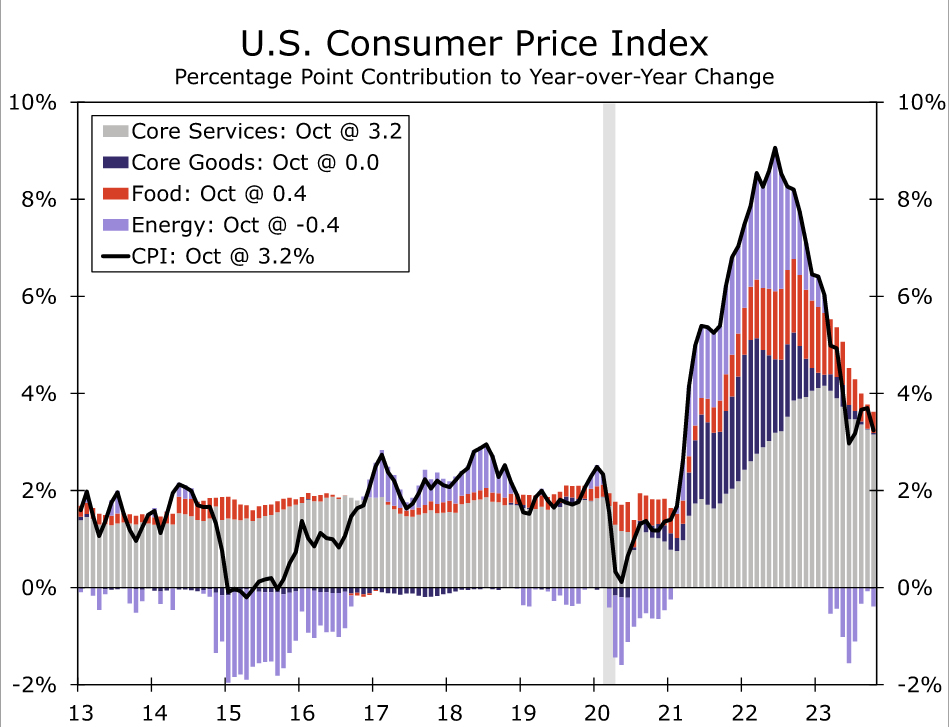

Compared to one year ago, the headline CPI has increased 3.2% (chart). Although this is still about a percentage above the pace that prevailed before the pandemic, it is well below the 9.1% peak that occurred in the summer of 2022. An outright decline in energy prices and much slower increases for food prices have put downward pressure on year-over-year inflation, although core price growth also has slowed to 4.0% from over 6% this time last year.

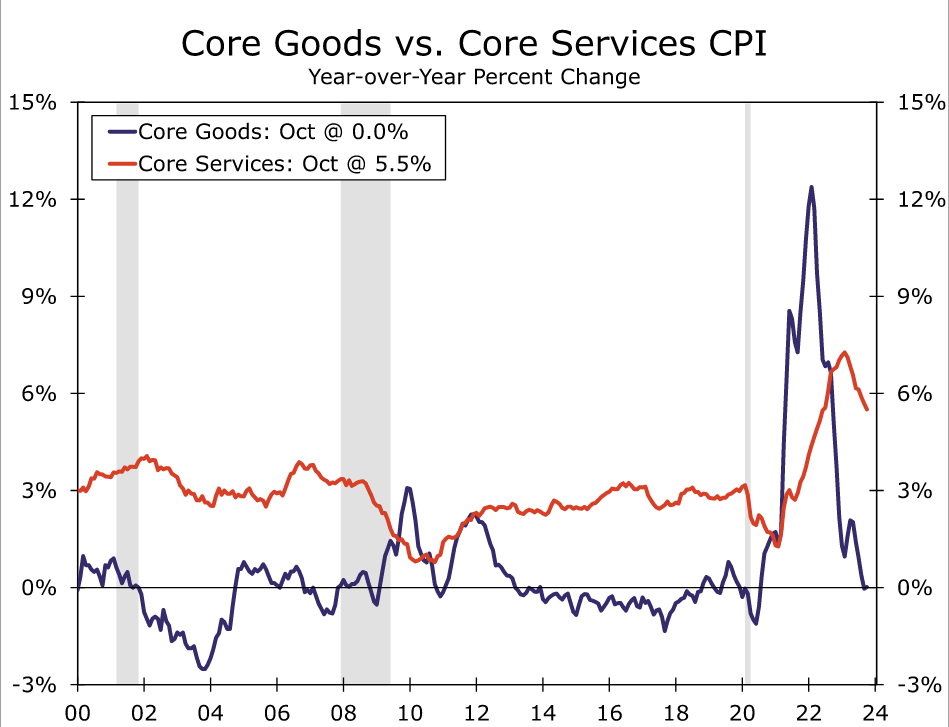

Excluding food and energy, consumer prices rose 0.2% in October, which was a touch softer than expected. The sharp run-up in goods prices since the pandemic continued to unwind in October. Core goods prices fell 0.1% in October, helped along by another drop in used vehicle prices (-0.8%) and a slight giveback in new vehicle prices (-0.1%). Elsewhere, goods prices were little changed over the month, as declines in education & communication equipment and motor vehicle parts offset small increases in apparel, medical and recreation goods. After peaking at a year-over-year rate of more than 12% last February, core goods price are unchanged from a year ago (chart).

Services inflation continues to ease as well, although progress remains slower than in the goods sector. Core services rose 0.3% in October, bringing the one-year change down to 5.5% from 6.7% this time last year. After a surprise 0.6% leap in September, owners’ equivalent rent growth slowed in October (+0.4%), while the monthly change in rent of primary residences was little changed at 0.5%. We expect to see shelter inflation to continue to moderate in the months ahead, although the steady rate of primary rent inflation cautions that the slowdown might not be as sharp as private sector measures have implied.

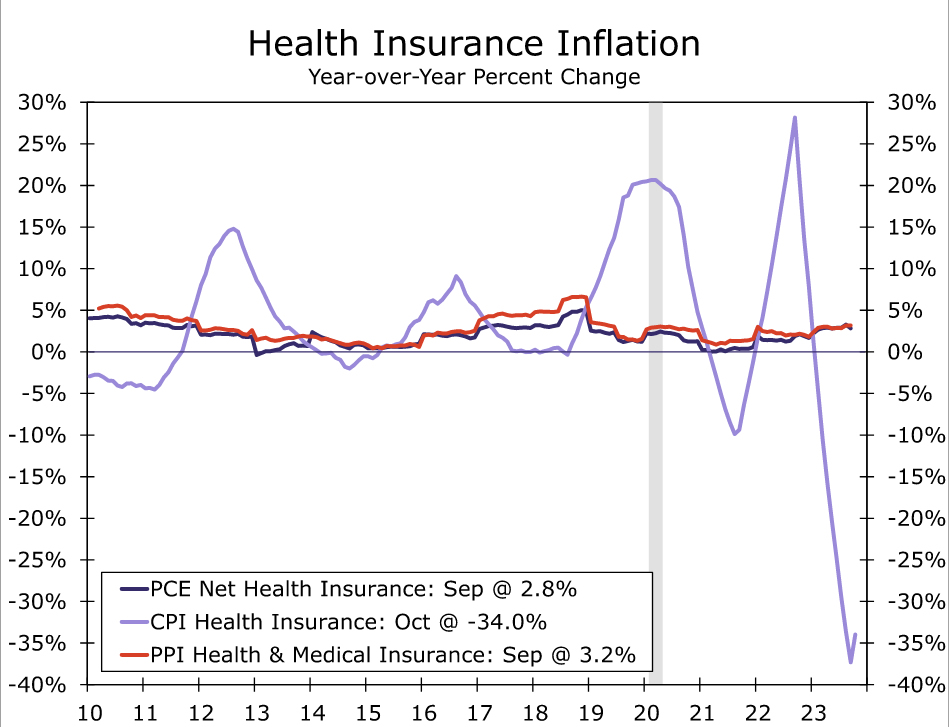

October’s softer print in core services came despite a renewed rise in health insurance prices. After falling an average of 3.8% per month over the past year, the health insurance index rose 1.1% in October. “Prices” in this category are measured indirectly by the industry’s retained earnings and are rather backward looking, with 2022 data incorporated with this release. Notably, the rise will not feed through to the PCE deflator, the Fed’s preferred gauge of inflation, where health insurance inflation is measured differently and is up a rather-unremarkable 2.8% over the past year (chart).

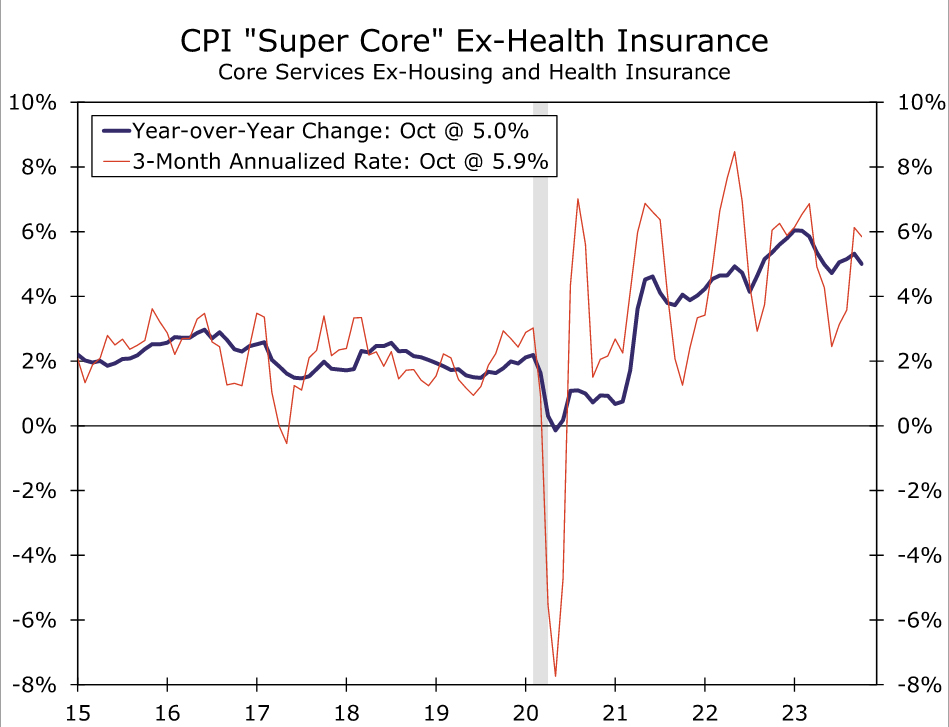

With the con of throwing yet another measure of “core” inflation into the mix, core services less primary shelter and health insurance, i.e., the CPI “super core” with the additional exclusion of health insurance, rose 0.2% in October after a 0.6% rise the prior month. Declines in both airfare (-0.9%) and hotel prices (-2.9%), two of the most volatile components of services, take some of the shine off the services slowdown, as they will be hard to repeat on a consistent basis. Through the large swings in travel-related services, the trend in CPI super core less health insurance is little improved over the past year, underscoring that despite the improvement for goods and housing, the fight against inflation is far from over (chart).

Focus To Turn from Future Rate Hikes to Future Rate Cuts

Today’s CPI report further reinforces our view that the last rate hike of this tightening cycle is behind us. We will not receive the October data for the Fed’s preferred measure of inflation, the PCE deflator, until November 30. That said, today’s CPI data signal that inflation took another step forward on its long road back to 2%. The FOMC’s job is not finished. Inflation is not yet back to 2%, and the Committee likely will need to feel confident that 2% inflation can be sustained before it begins to loosen its restrictive stance of monetary policy. Furthermore, the Committee will remain diligently on the lookout for any shocks that could disrupt the disinflationary trends that are currently in place. That said, as 2023 draws to a close and 2024 comes into view, we suspect the debate next year will focus squarely on when rate cuts and the end of quantitative tightening will occur.

{kind=link}