At next week’s policy meeting we expect the ECB to guide towards a more neutral policy outlook for the near term as we expect the ECB to virtually rule out the possibility of a further rate hike. That would mark the beginning of the end of the 4% policy rate level. This follows on the back of the inflation surprises on the downside in recent months. We expect the ECB to fall short of providing guidance on the timing of the first policy rate cut beyond the near future while repeating its call for a data-dependent approach. This will leave a Q2 24 rate cut as the most likely scenario for the next policy rate change.

During the Q&A part of the press conference, we expect Lagarde to acknowledge that ending the full PEPP reinvestments has been discussed. A formal decision with its technical details published is only expected at the January meeting for an immediate implementation.

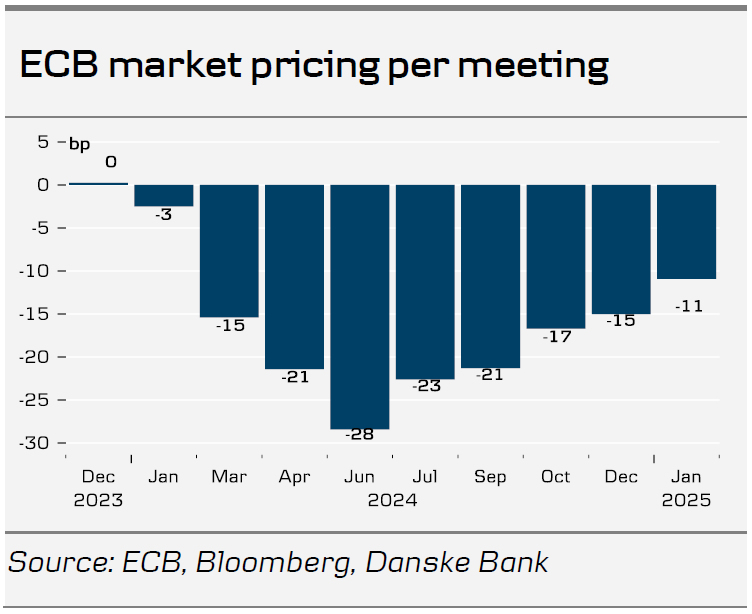

While markets are pricing in a very aggressive rate cut cycle through the end of next year of 140bp, and a 70% likelihood of a rate cut in Q1, we continue to expect the ECB to deliver its first cut in June, as we see the ECB respecting the ‘sequencing’ of first accelerating the liquidity normalisation and subsequently discussing rate cuts. We do not share the markets’ view on inflation and a growth outlook that would warrant more than five policy rate cuts next year as a main scenario.

Pushing back on the easing of financial conditions

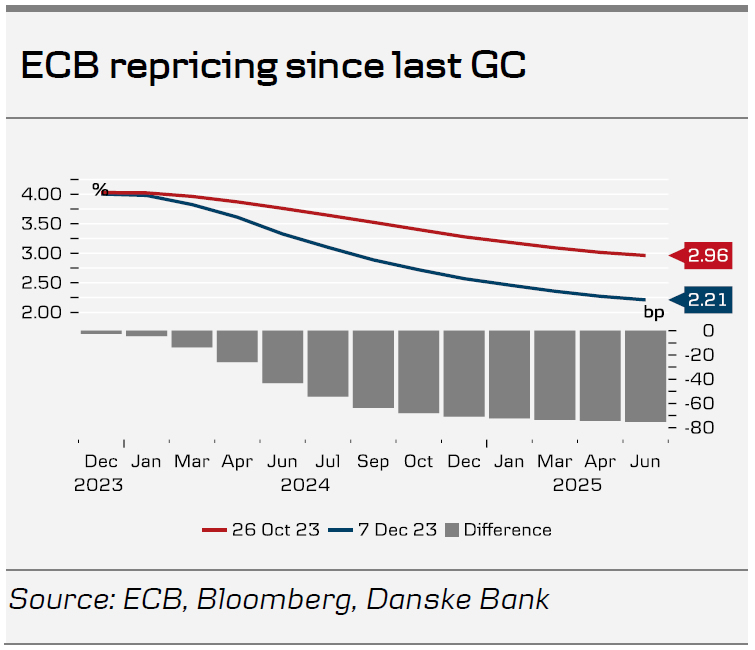

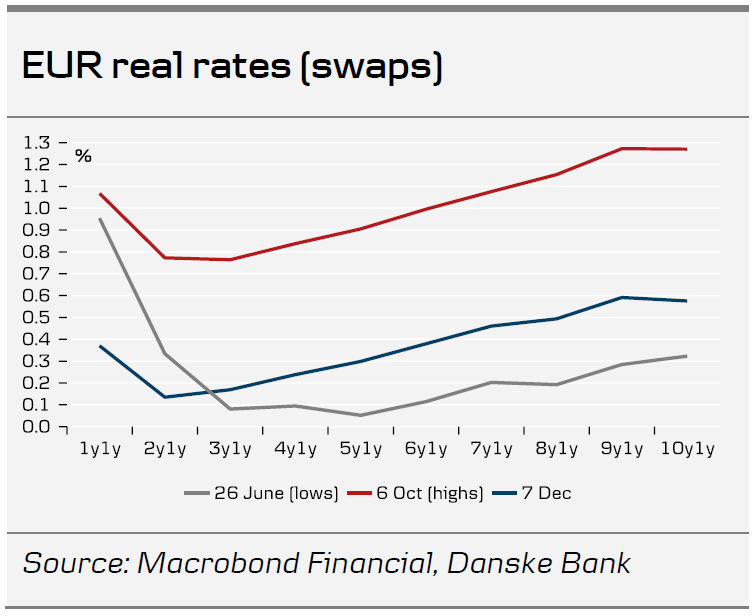

The downside surprise in recent months to inflation releases has provided ECB with an opportunity of shifting the narrative from how high the policy rates should go to how long will they stay at the current 4% level. We expect them to take advantage of this decline and say that in the absence of shocks, the final rate hike has already been delivered. Since the last governing council meeting on 26 October, markets have significantly eased financial conditions to multi-year lows on the back of a decline in rates markets with real rates in Europe approaching the year to date lows. While the inflation decline is an earlier than anticipated win to the ECB, we still view the repricing as unwanted relative to ECB’s sought-after calibration of the monetary policy stance.

While several governing council members have pushed back on the rate pricing saying it is ‘premature’ to discuss rate cuts, it has been with limited success on the market pricing. We expect ECB to push back on the easing of financial conditions that markets have been pricing during the past month. While President Lagarde has seldom commented directly on the policy rate pricing, we expect a moderate push back on the near-term financial conditions, which she has been referring to on previous occasions. We do not think that she will repeat the guidance for no rate cuts in the next ‘couple of quarters’ as she said two weeks ago – which will bring Q2 next year as the most likely scenario for the first rate cut. Markets are currently pricing 140bp of rate cuts through the end of next year.

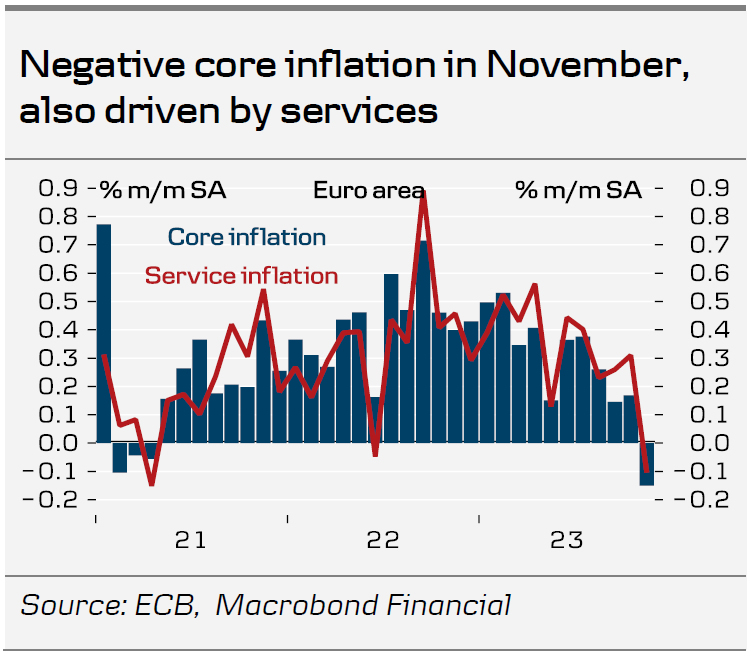

The November inflation print gave the ECB an early Christmas present

The November inflation print came in somewhat below expectations at 2.4% (compared to consensus of 2.7%) and is the third consecutive inflation surprise on the downside and thus it seems like Christmas came early for the ECB. Most recently, the decline in the inflation November report was broad-based where headline inflation even declined 0.5% m/m. Core inflation ticked down to 3.6% y/y from 4.2% y/y in October. Also remarkably, the monthly change in seasonally adjusted core inflation was negative at -0.2 driven by both negative goods and service price inflation. We expect Lagarde to sound more optimistic on the inflation outlook while at the same time remain cautious about making over hasty decisions.

Economic activity stagnating

Closely approaching year-end, economic activity in the euro area is stagnating after a strong recovery in 2021 and 2022 following the pandemic. Real GDP contracted marginally in Q3 on a quarterly basis, which left the yearly growth rate close to 0%, reflecting how the ECB’s restrictive monetary policy is working its way through the economy. That said, private consumption is the key growth sector of the euro area economy. Since the October ECB meeting, we have received the November PMIs that remained in contractionary territory but also sparked some hopes by improving more than expected to 48.7 and 44.2 in the service sector and manufacturing sector, respectively. Given the significant monetary tightening and uncertainty in the economy it is encouraging for the ECB that activity is not declining faster, which supports the ‘soft-landing’ case. Yet, the downside risk for the growth outlook is still that we suddenly see a more rapid transmission of monetary policy and tightening of financial conditions or a spike in energy prices and geopolitical uncertainty, see A year of transition ahead , 7 December.

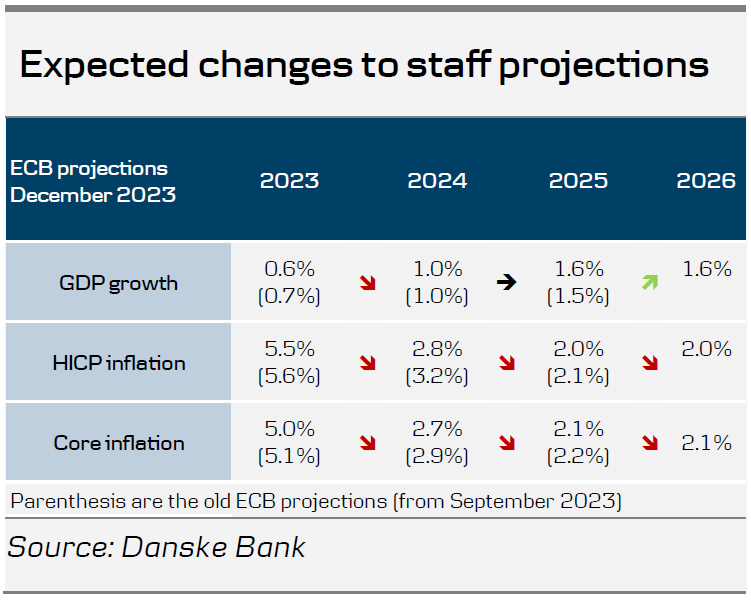

The new staff projection will likely lower the inflation outlook

We will closely watch the ECB staff projections on the back of the recent larger than expected declines in inflation. Both headline and core inflation have printed significantly lower in Q4 23 compared to the September ECB projections. We expect a rebound in HICP in December to 3.0% y/y, which will take the Q4 average to 2.8%. This will be 0.5 percentage points lower than the latest staff projections. This larger under hang as well as lower commodity futures will result in lower inflation projections next year.

Futures point to a downward revision of the technical assumptions on oil and gas prices in 2024 by 5% and 25%, respectively, and 7% and 20%, respectively, in 2025. These revisions will probably also imply that inflation projections get revised down to or below the 2% target in both 2025 and 2026, which will allow the ECB to start thinking about rate cuts.

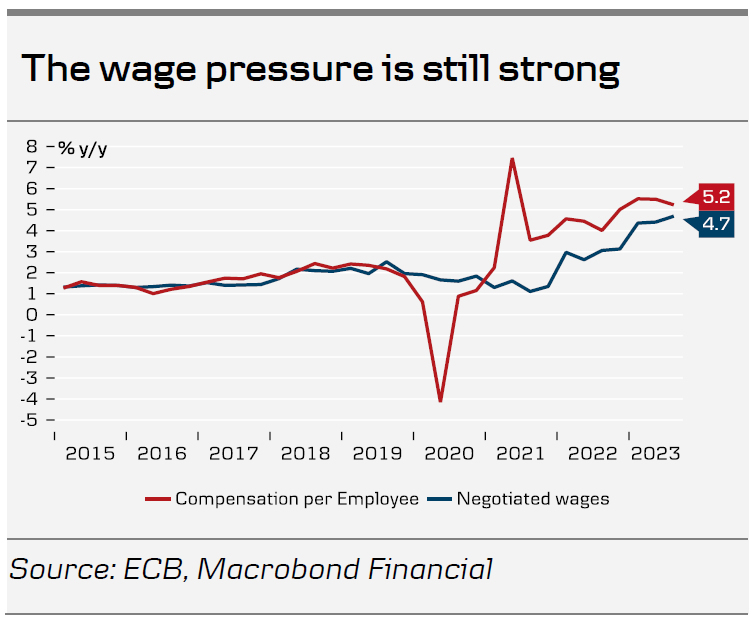

However, we expect the ECB to argue that it is premature to talk about rate cuts as upside risks persist for the inflation outlook, but the communication can be less aggressive than previously. The labour market is historically strong, and companies are reporting labour shortages amid strong wage growth with negotiated wages increases of 4.7% in Q3 and compensation per employee at 5.2%. The strong labour market and increasing real wages will support growth in the coming years. This fact combined with the weaker than projected Q3 GDP print will likely mean that the growth projections do not change significantly.

First step to end the full PEPP reinvestments

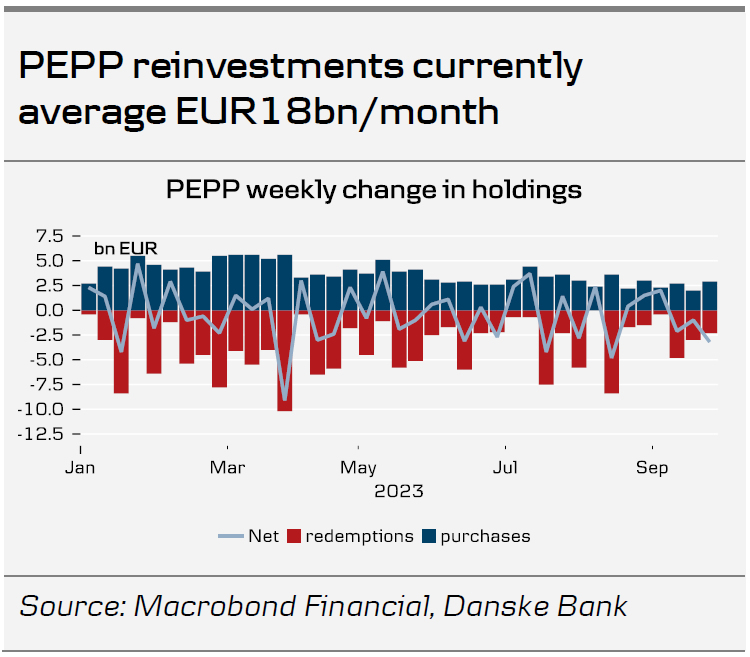

Last week, President Lagarde during a European Parliament hearing said with reference to the ongoing PEPP reinvestments currently guided to run at least until end of 2024, that ‘this is a matter which will come probably for discussion and consideration … in the not too distant future and we will re-examine possibly this proposal’. Given the benign market environment we firmly believe that this will be discussed next week – something that Lagarde will likely acknowledge during the Q&A session. A formal announcement will only follow in January. This will complement the already ongoing balance sheet normalisation from APP. Importantly, we do not expect the ECB to step back from reinvesting PEPP bonds in one take, but take a smoothening approach via a gradual phasing out of PEPP reinvestments. We see the PEPP reinvestments average EUR18bn per month through the past 12 month and we assume a similar redemption pattern is foreseen next year. Once the end to PEPP reinvestments is announced we assume it will be of immediate implementation, and hence no later than 1 April, with our baseline being for 1 March. We expect the first 12m of PEPP holding reduction will be to the tune of EUR150bn altogether. We expect that an announcement in January of the end to full PEPP reinvestments will be a compromise with the doves on the policy outlook.

Pushback on significant ECB repricing could support EUR/USD

We anticipate a relatively muted reaction in the FX markets, as both the ECB meeting and the FOMC meeting the day before are unlikely to bring any major surprises. If anything, there could be a slight pushback on the aggressive repricing of the ECB over the past couple of weeks, i.e., a relatively hawkish ECB underscoring that it is premature to talk about rate cuts. This, in turn, could support our near-term view of a higher EUR/USD. Regarding our strategic case, we maintain our belief that EUR/USD will move lower, based on relative terms of trade, real interest rates, and relative unit labour costs. Our projection for the cross is at 1.06/1.04 over the next 6-12 months. However, in the near-term, we still see potential for a higher EUR/USD. We expect weaker US data, positive risk appetite, and an unwinding of the aggressive ECB cuts that were priced for next year to support the cross in the short term.

{kind=link}