Summary

The November CPI report was relatively uneventful. Falling gasoline prices and modest food inflation restrained the headline CPI to just a 0.1% increase in the month. Excluding food and energy prices, core CPI was up 0.3%, in line with consensus expectations. Core goods prices continued to decline even as the drivers of the dip changed, while core services inflation was a bit stronger in November compared to October due to faster inflation for shelter, medical care and transportation.

The November CPI data probably do not move the needle much for the FOMC this week. Doves looking for a downside surprise did not see one materialize, but a nasty upside shock was also avoided. Looking through the month-to-month volatility, inflation continues to move back toward the Fed’s 2% inflation target. That said, price growth remains far enough away from 2% that the central bank likely will not declare victory just yet. We suspect the FOMC will keep monetary policy in a holding pattern and look toward the Q1 labor market and inflation data to determine its next move. Our base case for the first rate cut remains June 2024.

Falling Gas Prices Keep CPI In Check

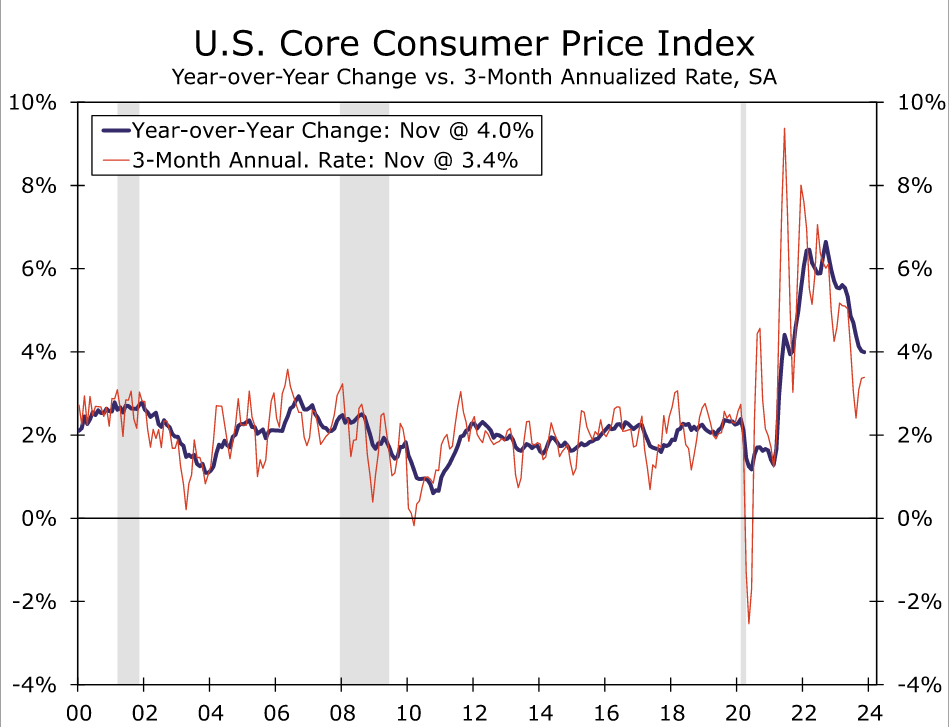

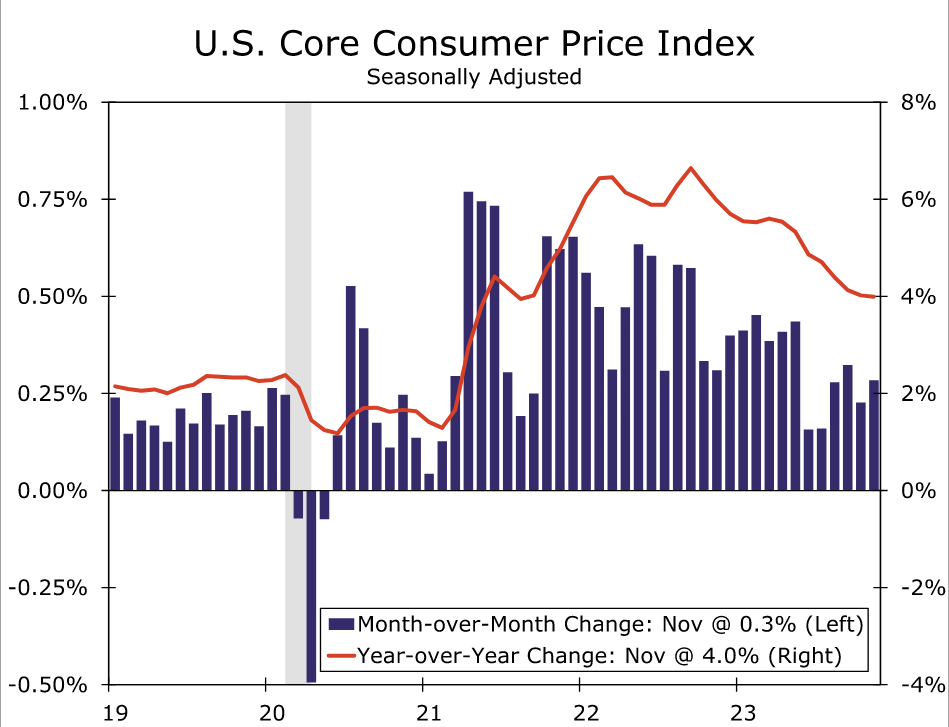

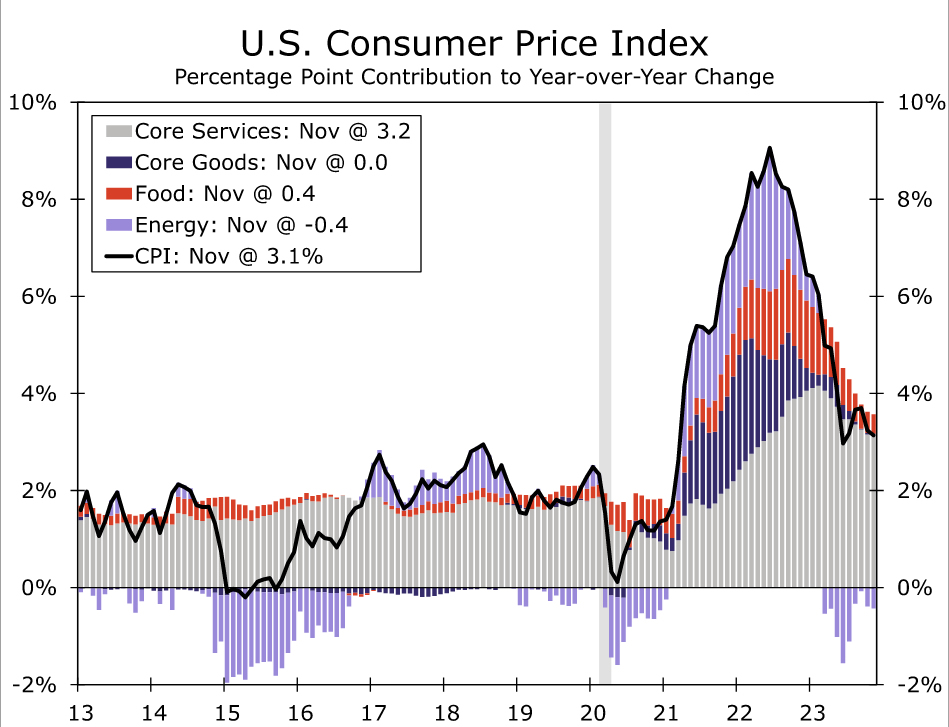

The Consumer Price Index rose 0.1% in November, a touch stronger than the Bloomberg consensus forecast. Excluding food and energy, core prices rose 0.3% during the month, in line with expectations. Compared to one year ago, headline CPI inflation was 3.1%, while the core CPI has increased by 4.0% over the same period. For context, both headline and core CPI inflation were 2.3% year-over-year in December 2019, shortly before the COVID-19 pandemic struck.

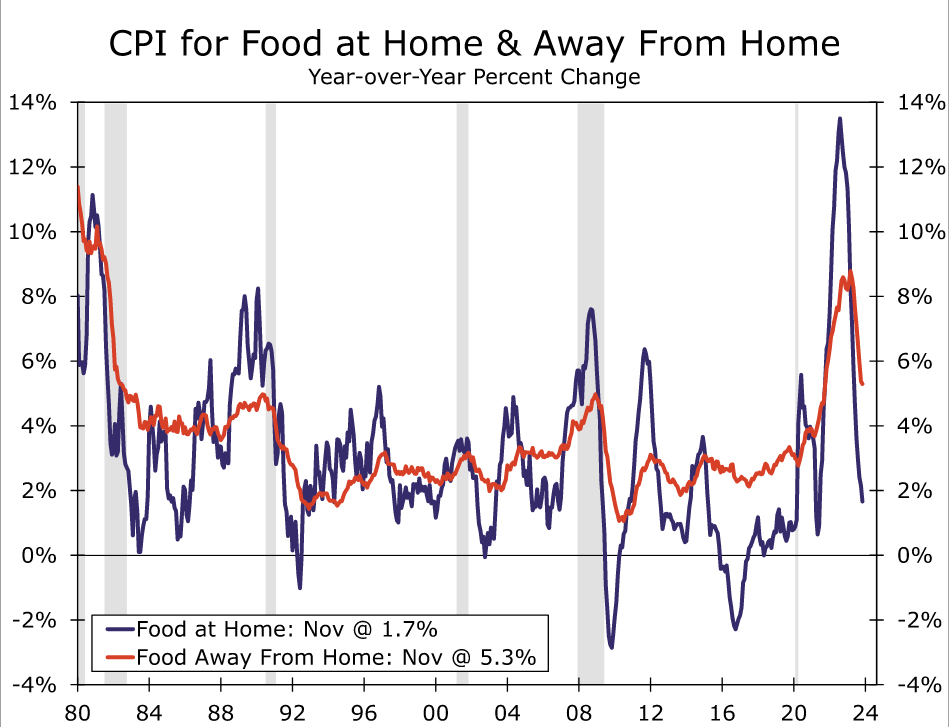

A major decline in energy prices in November kept monthly CPI inflation in check. Gasoline prices fell by 6.0% in November on the heels of a 5.0% dip in October. Energy services inflation was stronger at 1.7%, led higher by electricity prices (+1.4%) and utility gas (+2.8%). Food price inflation moderated a touch from September’s pace, registering 0.2% in November. Prices for meals at restaurants continue to rise faster than prices at the grocery store, a shift from the trend that prevailed earlier in the cycle (chart).

Excluding food and energy, price growth showed little change in the recent rate of underlying inflation. Core CPI rose 0.3% in November, which kept the 3-month annualized rate unchanged at 3.4%.

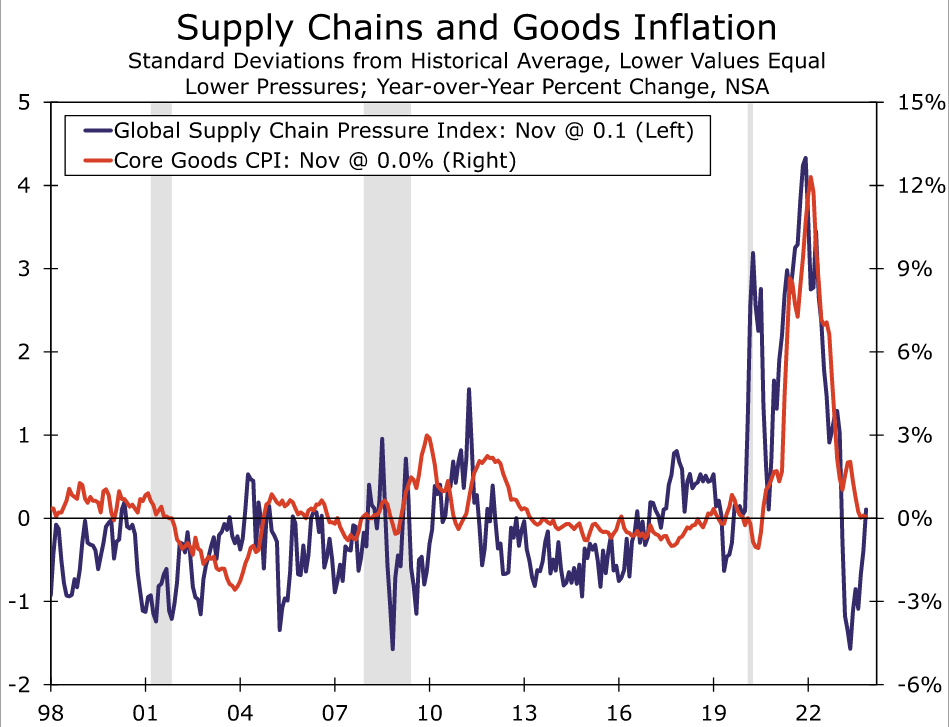

Underneath the hood, the split between core goods and services remains firmly in place. Core goods prices declined for a sixth-consecutive month. The 0.3% drop in November came despite a rise in used vehicles (+1.6%) as extended Black Friday deals helped to drive prices down for electronics (-2.7%), apparel (-1.3%), recreation goods (-0.6%) and household furnishings (-0.4%). Looking ahead, used vehicle prices look set to renew their downward trend, while prices for holiday shopping categories seem unlikely to repeat November’s pace of declines. Through the ups and downs of various sub-categories, the trend in core goods prices is likely to remain modestly deflationary over the coming months, led primarily—but not entirely—by lower vehicle prices.

Core services inflation, on the other hand, firmed a bit in November, increasing 0.5% after a 0.3% gain in October. Shelter inflation continues to moderate slowly rather than sharply, with primary shelter (rent of primary residences and owners’ equivalent rent) price growth edging up sequentially in November (0.5%) but continuing to move down on a year-over-year basis (6.7% after 6.9% in October). Among other services, medical care costs came in stronger, led by a rebound in physician services, while travel services (largely lodging away from home and airfares) declined less sharply. However, there were signs that the plateauing in vehicle prices is beginning to bring some relief to the rate of motor vehicle insurance price hikes (up 1.0% in November—the smallest increase since February), while motor vehicle maintenance, recreation services, tuition and other personal services also posted subdued gains relative to each category’s recent monthly trend.

Economics

Overall, progress continues in getting inflation back down to the Fed’s 2% target. On a year-over-year basis, CPI inflation has slowed 4.0 percentage points since November 2022. Outright declines in energy prices have put the biggest dent in inflation over the past year, but price growth has slowed for other major categories, including food, core goods, housing and other core services (chart). While the level of prices remains frustratingly higher for consumers, having grown 19% since the onset of COVID, the slowing rate of change is at least consistent with the Fed making headway toward a stable inflation environment.

Yet even with the significant slowdown in inflation over the past year, price growth continues to run above the Fed’s desired rate on both a headline and core basis. We expect inflation to slow further over the course of the coming year as demand growth weakens and improved supply dynamics limit input cost growth and feed through to consumer prices. However, progress is likely to be slower-going ahead, with the bulk of normalization to supply chains and the labor force behind us, leaving demand to take on greater importance in reducing inflation (chart).

In our view, today’s CPI report probably does not meaningfully impact this week’s FOMC meeting. Despite some noise underneath the headline figures, the broad takeaway is that the steady-but-bumpy downward trend in inflation remains in place. In light of this trend, we believe the FOMC will stand pat at its December meeting with an eye toward the Q1 inflation and labor market data to guide when rate cuts will be appropriate. So long as inflation continues to slow in 2024, rate cuts should materialize next year, with the pace of cuts determined by the resiliency (or lack thereof) in the U.S. labor market.

{kind=link}