ECB Review: Didn’t Rock the Boat, But Sailing Towards a Rate Cut

- As widely expected, the ECB left its three policy rates unchanged at today’s meeting, leaving its key policy rate (deposit rate) at 4%. Today’s meeting was expected to be a stocktaking meeting with no new policy signals and the ECB delivered just that. The ECB confirmed that the incoming information was broadly in line with the staff projections laid out at the December meeting. We view today’s assessment from the ECB as necessary but not sufficient for a rate cut.

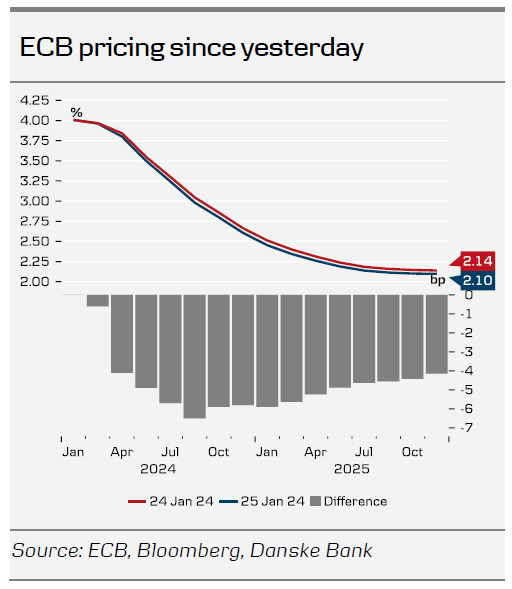

- While Lagarde said it was premature to discuss rate cuts, markets sent yields lower from the front end. Markets are pricing 20bp by the April meeting, which must be considered a live meeting. We stick to our call of a first rate cut coming in June, but highlight our long held risk bias of an April meeting cut. The question now is when/ how many there will come.

The road to rate cuts

The ECB gave no new policy signals today and Lagarde said that she stood by her comments made last week. Last week she said that the next rate change would likely be a cut and when asked whether this would be in the summer, she acknowledged that. Today’s meeting will be remembered as another step in the process of the ECB delivering a rate cut.

Incoming data as expected but wage pressure is easing

Lagarde acknowledged that the incoming data since the December meeting have been broadly as expected. Hence, the ECB has not changed its assessment of the economic situation and the inflation outlook since the last meeting. Aside from the energy-related upward base effect on headline inflation, the declining trend in underlying inflation continued as past interest rates were transmitted forcefully into financial conditions. Yet, Lagarde noted that wage pressure has started to ease and that firms are absorbing wage increases by reducing profit margins instead of increasing prices. This was a slight change of communication in the soft direction compared to the December meeting. Regarding the wage growth, Lagarde highlighted that Indeed’s wage growth tracker had stabilised at higher levels (and is primarily backward looking), and she also added that 40% of workers’ wages will be renegotiated in the near term.

On the growth side the ECB expects that the economy stagnated in Q4 23, and Lagarde said that incoming data continue to signal weakness. However, she also noted that forward looking indicators point to a pickup in growth later this year but that the risks to the growth outlook are tilted to the downside.

April meeting may be a live meeting

Based on today’s meeting, we stick to our call for the ECB to deliver its first 25bp rate cut at the June meeting, but we also repeat our long-held bias for risk of an earlier rate cut. We believe that if the ECB staff projections are revised lower, the ECB may deliver a cut already at the April meeting. The incoming data until then is plentiful with in particular inflation prints and wage growth being important, as well as the profit margin/ wage growth discussion (see above). If the January inflation next week surprises on the downside, markets will likely add to its already 20bp rate cut (cumulative). Today, Lagarde had the opportunity to push back on the market pricing and she choose not to, which led to a front-end driven rally. Markets are pricing 140bp of rate cuts until the end of this year. Lagarde said that the operational framework review will most likely be concluded by the end of spring.

EUR/USD moved lower to around the 1.0850 mark after the relatively dovish ECB meeting, which has made the April meeting live, combined with US macro data continuing to surprise to the upside, including strong Q4 flash GDP figures. We have recently discussed the possibility of a USD rally in Q1 due to stronger-than-expected US figures relative to the rest of the world. So far, this has played out well with strong US PMIs and Q4 GDP figures. We will have more clarity next week with releases such as ISM and nonfarm payrolls, in addition to the Fed meeting. Additionally, while we recognise that our Fed (first cut in March) and ECB (first cut in June) forecasts, all else equal, are positive for EUR/USD in H1, we believe that the broader pricing in the G10 could be more decisive for the cross, as we perceive current market expectations for rate cuts to be excessive. We still maintain our bias towards selling EUR/USD on rallies in the near term, and we forecast EUR/USD at 1.07/1.05 on a 6/12M horizon. We also remain short EUR/USD via a 6M put spread as part of our FX Top Trades 2024.

at 4%. Today's meeting was expected to be a stocktaking meeting with no new policy signals and the ECB delivered just that. The ECB confirmed that the incoming information was broadly in line with the staff projections laid out at the December meeting. We view today's assessment from the ECB as necessary but not sufficient for a rate cut.){kind=link}